Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

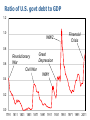

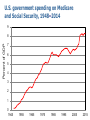

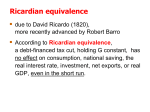

Government Debt – Chapter 19, 8th and 9th THIS CHAPTER COVERS about the size of the U.S. government’s debt and how it compares to that of other countries problems measuring the budget deficit [SKIP] the traditional and Ricardian views of the government debt other perspectives on the debt [SKIP] 1 Indebtedness of the world’s governments Country Gov Debt (% of GDP) Country Gov Debt (% of GDP) Japan 142.9 France 70.9 Greece 125.3 U.K. 64.2 Italy 120.4 Germany 42.4 Portugal 99.8 Netherlands 42.3 Belgium 91.6 Canada 40.9 United States 85.5 Switzerland 6.5 Spain 73.3 Australia 3.5 US debt is large in absolute terms. Moderate compared to other countries. https://www.treasurydirect.gov/govt/reports/pd/mspd/2017/opdm042017.p df Ratio of U.S. govt debt to GDP 1.2 1.0 WW2 Financial Crisis 0.8 0.6 Great Revolutionary Depression War Civil War WW1 0.4 0.2 0.0 1791 1811 1831 1851 1871 1891 1911 1931 1951 1971 1991 2011 U.S. government spending on Medicare and Social Security, 1948–2014 9 Percent of GDP 8 7 6 5 4 3 2 1 0 1945 1955 1965 1975 1985 1995 2005 2015 Is the govt debt really a problem? Consider a tax cut with corresponding increase in the government debt. Two viewpoints: 1. Traditional view 2. Ricardian view The traditional view of Debt Cut T and hold G constant: In the Short run: Y, u Long run (AD-AS model): Y and u back at their natural rates C , r, I Very long run: slower growth. Yp is lower than otherwise because I => K is lower than otherwise. Ricardian equivalence due to David Ricardo (1820), more recently advanced by Robert Barro According to Ricardian equivalence, a debt-financed tax cut, holding G constant, has no effect on consumption, national saving, the real interest rate, investment, or real GDP, even in the short run. This is in section 19.3 and 19.4. The logic of Ricardian Equivalence Consumers are forward-looking, base spending on current and expected future income - permanent Income/ Life Cycle Hypothesis Implication - Consumers know that a debt-financed tax cut today (holding G constant) implies an increase in future taxes that is equal in present value terms to the tax cut. The tax cut today (coupled with a tax hike in the future) is merely transitory income. Consumption does not change, Y does not change. The logic of Ricardian Equivalence Consumers save the full tax cut in order to repay the future tax liability. Result: Private saving rises by the amount public saving falls, leaving national saving unchanged, r unchanged, I unchanged, Y unchanged. A tax cut financed by government debt does not reduce the tax burden, it just reschedules the tax. Deficit financed by debt is equivalent to deficit financed by taxes. Question: Suppose consumers understand that the tax cut today is to be followed by a decrease in government spending in the future. Would consumption increase? Arguments against Ricardian Equivalence Myopia: Not all consumers think so far ahead, some see the tax cut as a windfall or an increase in life time income. Borrowing constraints: Some consumers cannot borrow enough to achieve their optimal consumption, so they spend a tax cut. Future generations: If consumers expect that the burden of repaying a tax cut will fall on future generations, then a tax cut now makes them feel better off, so they increase spending. Bush 1992 withholding Lower withholding, but pay up in the following April. RE predicts no change in consumption because life time resource(permanent income) was not changed – lower withholding was transitory income. Survey – 57% said would save and 43% spend. Most studies show MPC out of temporary tax change < MPC out of permanent tax change. Other examples Johnson 1968 tax surcharge. Temporary, people just reduced savings Ford 1974 tax rebate. People just increased saving