Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

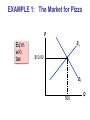

Unit IV Tax Incidence (Chapter7) In this chapter, look for the answers to these questions: How do taxes affect market outcomes? How does the outcome depend on whether the tax is imposed on buyers or sellers? What is the incidence of a tax? What determines the incidence? How does a tax affect consumer surplus, producer surplus, and total surplus? What is the deadweight loss of a tax? In this chapter, look for the answers to these questions: What factors determine the size of this deadweight loss? How does tax revenue depend on the size of the tax? What are the efficiency costs of taxes? How can we evaluate the equity of a tax system? Government Policies That Alter the Private Market Outcome • Price controls – Price ceiling: a legal maximum on the price of a good or service. Example: rent control. – Price floor: a legal minimum on the price of a good or service. Example: minimum wage. • Taxes – The govt can make buyers or sellers pay a specific amount on each unit bought/sold. We will use the supply/demand model to see how tax policy affects the market outcome (the price buyers pay, the price sellers receive, and eq’m quantity). Taxes • The govt levies taxes on many goods & services to raise revenue to pay for national defense, public schools, etc. • The govt can make buyers or sellers pay the tax. • The tax can be a percentage of the good’s price, or a specific amount for each unit sold. – For simplicity, we analyze per-unit taxes only. EXAMPLE 1: The Market for Pizza P Eq’m w/o tax S1 $10.00 D1 500 Q A Tax on Buyers A tax on buyers shifts the D curve down by the amount of the tax. The price buyers pay rises, the price sellers receive falls, eq’m Q falls. Effects of a $1.50 per unit tax on buyers P PB = $11.00 S1 Tax $10.00 PS = $9.50 D1 D2 430 500 Q The Incidence of a Tax: how the burden of a tax is shared among market participants P Because of the tax, buyers pay $1.00 more, sellers get $0.50 less. PB = $11.00 S1 Tax $10.00 PS = $9.50 D1 D2 430 500 Q A Tax on Sellers A tax on sellers shifts the S curve up by the amount of the tax. The price buyers pay rises, the price sellers receive falls, eq’m Q falls. Effects of a $1.50 per unit tax on sellers P PB = $11.00 S2 S1 Tax $10.00 PS = $9.50 D1 430 500 Q The Outcome Is the Same in Both Cases! The effects on P and Q, and the tax incidence are the same whether the tax is imposed on buyers or sellers! P What matters is this: A tax drives a wedge between the price buyers pay and the price sellers receive. PB = $11.00 S1 Tax $10.00 PS = $9.50 D1 430 500 Q A C T I V E L E A R N I N G 1: The market for Effects of a tax P 140 130 hotel rooms S 120 Suppose govt imposes a tax on buyers of $30 per room. Find new Q, PB, PS, and incidence of tax. 110 100 90 80 D 70 60 50 40 0 Q 50 60 70 80 90 100 110 120 130 A C T I V E L E A R N I N G 1: Answers P 140 The market for hotel rooms 130 PB = $110 Q = 80 PS = $80 Incidence buyers: $10 sellers: $20 S 120 PB = 110 100 90 PS = 80 Tax D 70 60 50 40 0 Q 50 60 70 80 90 100 110 120 130 Elasticity and Tax Incidence CASE 1: Supply is more elastic than demand In this case, buyers bear most of the burden of the tax. P Buyers’ share of tax burden PB S Tax Price if no tax Sellers’ share of tax burden PS D Q Elasticity and Tax Incidence CASE 2: Demand is more elastic than supply P Buyers’ share of tax burden S PB Price if no tax Sellers’ share of tax burden In this case, sellers bear most of the burden of the tax. Tax PS D Q Elasticity and Tax Incidence • If buyers’ price elasticity > sellers’ price elasticity, buyers can more easily leave the market when the tax is imposed, so buyers will bear a smaller share of the burden of the tax than sellers. • If sellers’ price elasticity > buyers’ price elasticity, the reverse is true. CASE STUDY: Who Pays the Luxury Tax? • 1990: Congress adopted a luxury tax on yachts, private airplanes, furs, expensive cars, etc. • Goal of the tax: to raise revenue from those who could most easily afford to pay – wealthy consumers. • But who really pays this tax? CASE STUDY: Who Pays the Luxury Tax? Demand is price-elastic. The market for yachts P Buyers’ share of tax burden S In the short run, supply is inelastic. PB Tax Sellers’ share of tax burden PS D Q Hence, companies that build yachts pay most of the tax. So, what do we know so far? • A tax is a wedge between the price buyers pay and the price sellers receive. • A tax raises the price buyers pay and lowers the price sellers receive. • A tax reduces the quantity bought & sold. The Effects of a Tax P With no tax, eq’m price is PE and quantity is QE . Govt imposes a tax of $T per unit. The price buyers pay is PB , Size of tax = $T S PB PE PS D the price sellers receive is PS , and quantity is QT . QT QE Q The Effects of a Tax P The tax generates revenue equal to $T x QT . Size of tax = $T S PB PE PS D QT QE Q The Effects of a Tax • Next, we use the tools of welfare economics to measure the gains and losses from a tax. • We will determine consumer surplus (CS), producer surplus (PS), tax revenue, and total surplus with and without the tax. • Tax revenue is included in total surplus, because tax revenue can be used to provide services such as roads, police, public education, etc. The Effects of a Tax P Without a tax, CS = A + B + C PS = D + E + F Tax revenue = 0 Total surplus = CS + PS =A+B+C +D+E+F A S B PE D C E D F QT QE Q The Effects of a Tax With the tax, CS = A PS = F Tax revenue =B+D Total surplus =A+B+D+F P A PB S B D C E PS D F The tax causes total surplus to fall by C + E QT QE Q The Effects of a Tax P C + E is called the deadweight loss (DWL) of the tax, the fall in total surplus that results from a market distortion, such as a tax. A PB S B D C E PS D F QT QE Q About the Deadweight Loss Because of the tax, the units between QT and QE are not sold. So, the tax has prevented some mutually beneficial trades. P PB S PS D QT QE Q A C T I V E L E A R N I N G 2: The market for Analysis of tax A. Compute CS, PS, and total surplus without a tax. B. If $100 tax per ticket, compute CS, PS, tax revenue, total surplus, and DWL. 400 airplane tickets P $ 350 300 S 250 200 150 D 100 50 0 Q 0 25 50 75 100 125 A C T I V E L E A R N I N G 2: Answers to A The market for P CS = ½ x $200 x 100 = $10,000 airplane tickets $ 400 350 300 S 250 PS = ½ x $200 x 100 P = 200 = $10,000 150 D 100 total surplus = $10,000 + $10,000 50 = $20,000 0 Q 0 25 50 75 100 125 A C T I V E L E A R N I N G 2: Answers to B A $100 tax on P CS = ½ x $150 x 75 = $5,625 $ 400 350 300 PS = $5,625 PB = 250 tax revenue = $100 x 75 = $7,500 200 PS = 150 total surplus = $18,750 50 DWL = $1,250 airplane tickets S D 100 0 Q 0 25 50 75 100 125 What Determines the Size of the DWL? • The govt needs tax revenue to finance roads, schools, police, etc., so it must tax some goods and services. • Which ones? One answer is that govt should tax the goods or services with the smallest DWL. • So when is the DWL small vs. large? Turns out it depends on the elasticities of supply and demand. • Recall: The price elasticity of demand (or supply) measures how much quantity demanded (or supplied) changes when the price changes. DWL and the Elasticity of Supply When supply is inelastic, the DWL of a tax is small. P S Size of tax D Q DWL and the Elasticity of Supply P The more elastic supply, the larger the DWL. S Size of tax D Q DWL and the Elasticity of Supply When demand is inelastic, the DWL of a tax is small. P S Size of tax D Q DWL and the Elasticity of Supply P S The more elastic the demand, the larger the DWL. Size of tax D Q Why Elasticity Affects the Size of DWL • A tax distorts the market outcome: consumers buy less and producers sell less, so eq’m Q is below the surplusmaximizing quantity. • Elasticity measures how much buyers and sellers respond to changes in price, and therefore determines how much the tax distorts the market outcome. A C T I V E L E A R N I N G 3: Elasticity and DWL of a tax Would the DWL of a tax be larger if the tax were on A. Rice Krispies or sunscreen? B. Gasoline in the Short Run vs. Gasoline in the Long Run C. Insulin vs. Caribbean Cruises A C T I V E L E A R N I N G 3: Answers A. Rice Krispies or sunscreen From Chapter 6: Rice Krispies has many more close substitutes than sunscreen, so demand for Rice Krispies is more price-elastic than demand for sunscreen. So, a tax on Rice Krispies would cause a larger DWL than a tax on sunscreen. A C T I V E L E A R N I N G 3: Answers B. Gasoline in the short run or long run From Chapter 6: The price elasticities of demand and supply for gasolline are larger in the long run than in the short run. So, a tax on gasoline would cause a larger DWL in the long run than in the short run. A C T I V E L E A R N I N G 3: Answers C. Insulin vs. Caribbean Cruises From Chapter 6: Insulin is a necessity and therefore less price-elastic than a Caribbean Cruise So, a tax on a Caribbean Cruise would cause a larger DWL than a tax on insulin. A C T I V E L E A R N I N G 3: Discussion question • The government must raise tax revenue to pay for schools, police, etc. To do this, it can either tax groceries or meals at fancy restaurants. • Which should it tax? The Effects of Changing the Size of the Tax • Policymakers often change taxes, raising some and lowering others. • What happens to DWL and tax revenue when taxes change? We explore this next…. DWL and the Size of the Tax Initially, the tax is T per unit. Doubling the tax causes the DWL to more than double. P new DWL S 2T T D initial DWL Q2 Q1 Q DWL and the Size of the Tax Initially, the tax is T per unit. Tripling the tax causes the DWL to more than triple. P new DWL S T 3T D initial DWL Q3 Q1 Q DWL and the Size of the Tax Implication When tax rates are low, raising them doesn’t cause much harm, and lowering them doesn’t bring much benefit. When tax rates are high, raising them is very harmful, and cutting them is very beneficial. Summary When a tax increases, DWL rises even more. DWL Tax size Revenue and the Size of the Tax When the tax is small, increasing it causes tax revenue to rise. P PB S PB 2T PS T D PS Q2 Q1 Q Revenue and the Size of the Tax P PB PB When the tax is larger, increasing it causes tax revenue to fall. S 3T 2T D PS PS Q3 Q2 Q Revenue and the Size of the Tax The Laffer curve Tax shows the revenue relationship between the size of the tax and tax revenue. The Laffer curve Tax size Taxes and Efficiency • One tax system is more efficient than another if it raises the same amount of revenue at a smaller cost to taxpayers. • The costs to taxpayers include: – the tax payment itself – deadweight losses – administrative burden Administrative Burden • includes the time and money people spend to comply with tax laws • encourages the expenditure of resources on legal tax avoidance – e.g., hiring accountants to exploit “loopholes” to reduce one’s tax burden • is a type of deadweight loss • could be reduced if the tax code were simplified but would require removing loopholes, politically difficult Marginal vs. Average Tax Rates • average tax rate – total taxes paid divided by total income – measures the sacrifice a taxpayer makes • marginal tax rate – the extra taxes paid on an additional dollar of income – measures the incentive effects of taxes on work effort, saving, etc. Lump-Sum Taxes • A lump-sum tax is the same for every person • Example: lump-sum tax = $4000/person income average tax rate marginal tax rate $20,000 20% 0% $40,000 10% 0% Taxes and Equity • Another goal of tax policy: equity – distributing the burden of taxes “fairly.” • Agreeing on what is “fair” is much harder than agreeing on what is “efficient.” • Yet, there are several principles people apply to evaluate the equity of a tax system. The Benefits Principle • Benefits principle: the idea that people should pay taxes based on the benefits they receive from govt services • Tries to make public goods similar to private goods – the more you use, the more you pay. • Example: Gasoline taxes – the more you drive on public roads, the more gas you buy, so the more gas tax you pay The Ability-To-Pay Principle • Ability-to-pay principle: the idea that taxes should be levied on a person according to how well that person can shoulder the burden • suggests that all taxpayers should make an “equal sacrifice” to support govt • recognizes that the magnitude of the sacrifice depends not just on the tax payment, but on the person’s income and other circumstances – a $10,000 tax bill is a bigger sacrifice for a poor person than a rich person Three Tax Systems • Proportional tax: taxpayers pay the same fraction of income, regardless of income • Regressive tax: high-income taxpayers pay a smaller fraction of their income than low-income taxpayers • Progressive tax: high-income taxpayers pay a larger fraction of their income than low-income taxpayers Examples of the Three Tax Systems regressive % of income proportional tax % of income progressive tax % of income income tax $50,000 $15,000 30% $12,500 25% $10,000 20% $100,000 $25,000 25% $25,000 25% $25,000 25% $200,000 $40,000 20% $50,000 25% $60,000 30% U.S. Federal Income Tax Rates: 2010 (Married Filing Jointly) The U.S. has a progressive income tax. On taxable income… the tax rate is… 0 – $16,750 10% $16,750 - $68,000 15% $68,000 - $137,300 25% $137,300 - $209,250 28% $209,250 - $373,650 33% Over $373,650 35% CHAPTER SUMMARY A tax on a good places a wedge between the price buyers pay and the price sellers receive, and causes the eq’m quantity to fall, whether the tax is imposed on buyers or sellers. The incidence of a tax is the division of the burden of the tax between buyers and sellers, and does not depend on whether the tax is imposed on buyers or sellers. The incidence of the tax depends on the price elasticities of supply and demand. Policymakers often face a tradeoff between the goals of efficiency and equity in the tax system. Much of the debate over tax policy arises because people give different weights to these two goals. CHAPTER SUMMARY The efficiency of a tax system refers to the costs it imposes on taxpayers beyond their tax payments. One cost is the deadweight loss caused by the distortion of incentives from taxes. Another is the administrative burden of complying with tax laws. The equity of a tax system refers to its fairness. The benefits principle suggests that it is fair for people to be taxed based on the amount of government benefits they receive. The ability-to-pay principle suggests that it is fair for people to pay taxes based on their ability to handle the burden. The U.S. has a progressive tax system, in which high income taxpayers face a higher average tax rate than low income taxpayers.