Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

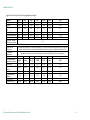

SBERBANK OF RUSSIA Russia: Budgetary Aces June 16, 2014 In the absence of external shocks, the stability of government finances can’t be doubted and will be provided even under the conditions of significant economic deceleration. The federal budget deficit will remain low and the public debt will increase insignificantly Even a significant increase of budget expenditures will not result in disastrous consequences, although, in this scenario, the federal budget deficit expansion reaches more risky levels of ~4.5-5% of GDP in a medium-term perspective. A slight acceleration in economic growth with increasing expenditures helps to slow down the growth of the budget deficit The fall of oil prices to $80 per barrel is critical for the budget stability. A serious expansion of the budget deficit, the accumulation of the public debt and the full use of sovereign wealth funds will cause the necessity of structural changes in budget policy Fiscal Sustainability: Risks Can’t be Ignored, but… Fiscal sustainability is an important achievement of the country… The stability of government finances is an important element of the economic stability and a subject of deserved pride of the government. Despite the significant deceleration in economic growth and the burst of geopolitical risks, the state of public finances is not a cause for concern. The federal budget deficit remains low (less than 1% of GDP). The size of the public debt (9.5% of GDP in total, including 2,9pp of the external public debt) allows us to talk about low risks of the rising cost of its maintenance. Even the hard consequences of falling oil prices can be smoothed for 1-2 years with the help of “safety cushion”, i.e. the sovereign wealth funds which reached $175 billion in total, or more than 9% of GDP. …but there are risks that should be evaluated under different scenarios of economic development and policy choices However, the general deterioration of the economic situation has affected a budgetary sphere as well: the income is not enough to finance all the ambitious projects and tasks at one time, which demands a careful and scrupulous management of priorities. New urgent expenses lead to slow growth of the budget expenditures. Now we more often hear talks about the abolition of socalled “budget rule”, according to which the size of the budget deficit should not exceed 1% of GDP in case of limiting the use of oil and gas revenues to finance Federal budget deficit, % GDP Source: Ministry of Finance of the Russian Federation © Centre of Macroeconomic Studies of Sberbank of Russia Public debt, % GDP Source: Ministry of Finance of the Russian Federation, Bloomberg 1 SBERBANK OF RUSSIA current budget expenditures. Although the government makes loud statements about the integrity of “budget rule”, in the past years the authorities demonstrated a flexible approach modifying the rule and treating it in accordance with circumstances. Thus, the shortfall of non-oil revenues in 2013 was offset by the use of oil revenues, exceeding the limits, set by the rule (i. e. exceeding revenues, received under the oil prices $91/bbl). We shall simulate the effects of economic slowdown, growth of government expenditures and possible fall of oil prices Now, the risks of further deterioration of the economic situation are high enough and it can undoubtly have a negative impact on the budgetary sphere. Our calculations include different economic scenarios and cover the most likely responses of the fiscal policy to the potential challenges. We shall consider three scenarios and will test the sustainability of the fiscal policy during their implementation: 1. A significant slowdown in economic growth in the next 5-7 years (a long period of low economic growth) at a very moderate increase in budget expenditures; 2. A rapid increase in budget expenditures, which can be necessary for stimulation of economy, building up the military forces and social welfare (the annexation of Crimea will also require an increase in government investments); 3. A sharp fall in oil prices to $80 per barrel, which in turn will cause a drastic drop in government revenues (a primary risk of the fiscal policy). Federal budget revenues, % of GDP Source: Ministry of Finance of the Russian Federation Size of sovereign wealth funds, billion USD Federal budget expenditures, % of GDP Source: Ministry of Finance of the Russian Federation (2011 requalification) Crediting oil-and-gas revenues of federal budget to the Reserve Fund, % of GDP 2,0% 1,5% 1,0% 0,5% 0,0% 2008 Source: Ministry of Finance of the Russian Federation, Haver Analytics © Centre of Macroeconomic Studies of Sberbank of Russia 2009 2010 2011 Source: Ministry of Finance of the Russian Federation 2 2012 2013 SBERBANK OF RUSSIA Basic Scenario: Fiscal Stability Базовый сценарий: Basic scenario: the продолжение continuation of текущей бюджетной current fiscal policy политики в условиях in the context of the замедления economic slowdown экономики In the basic scenario of the economy development we assume the stability of oil prices around $105 per barrel (Urals), a moderate inflation around 5-6%YoY, a very modest economy growth (around 1,5%YoY after overcoming more significant slowdown in 2014-15), caused by a low investment demand and by the deterioration of investment climate in general. According to this scenario, there is no way to avoid the weakening of the ruble, which still will be quite smooth. Share of oil-and-gas revenues will be reduced; the role of non-oil revenues will increase Our calculations show that the gap between non-oil and oil-and-gas revenues will increase, what in turn will lead to a reduction in the proportion of oil-and-gas revenues in the total revenues of the Federal budget - from 50% in 2013 to 45% in 2020. Unfortunately, this reduction will not be connected with the growth of non-oil revenues (they will remain stable in terms of GDP share), but with the relative decline of oil-and-gas revenues. Indeed, the dynamics of income’s ruble equivalent at marginally low production growth depends, first of all, on the speed of ruble’s weakening. If there is no serious weakening of the ruble in real terms (it is assumed in our basic scenario due to high oil prices), then the difference between the increase of production in oil and gas sector and the economic growth will provide the decrease of oil-and-gas revenues as GDP share. The stability of non-oil income level from GDP provides main taxes: VAT, income tax and excise tax. The growth of domestic VAT is expected at the level of growth of nominal GDP, and the ruble equivalent of the foreign VAT will be affected by the combination of the expected deceleration of import (the decline in revenues) and some weakening of the ruble (revenue growth). The growth of the return of profit tax is expected to be roughly proportional to GDP, and the increase of excise rates, especially on tobacco and alcohol, will continue according to the preliminary plans of the government. Stability of budget expenditures: 2021% from GDP We supposed that in the basic scenario the current expenditure policy will be continued: expenditures will increase approximately proportionally to the nominal GDP, along with this the expenditure on social policy, national security and defense will grow a little faster than others. The increase of expenditures connected with the annexation of Crimea is estimated in the amount of 130 billion rubles in 2014. From this perspective, the expenditures of the Federal budget will remain stable on the level 20-21% of GDP. It means that the nominal expenditures increase will not lead to their growth in real terms. Budget deficit can grow, but will still be quite moderate In this scenario it is impossible to avoid the growth of the budget deficit up to 3% of GDP by 2020. It is, according to our estimates, not critical. This deficit can be relatively financed by borrowings from domestic and foreign markets (in a 3:1 ratio). Therefore, the annual volume of external borrowings on an average will not exceed $15-20 billion. With this moderate amount of new borrowings the rates will not grow significantly, leaving the task of debt service feasible. Under these assumptions, the volume of public debt will not exceed 20% of GDP by the end of the forecast period. This figure is way bellow, for example, than «sustainability level» in 60% of GDP, recommended by the IMF for its borrowers. © Centre of Macroeconomic Studies of Sberbank of Russia 3 SBERBANK OF RUSSIA Indicator GDP growth Inflation Dollar exchange rate, rub Price Urals,$ Rate on internal debt Rate on external debt Federal Budget Deficit,% from GDP Proportion –internal borrowing to external Macroeconomic background Governmental expenditures The level of the government debt by the end of 2020 2014 0.0% 6.5% 2015 0.5 6.0% 2016-2020 1.5% 5.1% 35.5 35.9 39.0 106 8.5% 5.0% 105 9.0% 5.0% 104 8.4% 5.3% 0.2% 1.2% 2.8% 3:1 Scenario description Growth rate of GDP up to 1.5% in mid-term; moderate inflation of ~5-6%, stable oil price of ~$104 Continuation of current tendencies. Increase of expenses due to the integration of the Crimea to Russia ~19.8% of GDP Probable Scenario: Increase in Expenditures Increase in expenditures is always tempting for the government Believing in the stability of the budgetary sector, we, however, think the government will not be able to avoid the temptation to increase expenditures. Expenses, connected with the annexation of Crimea can exceed 130 billion rubles, pledged by us for year 2014. More large-scale investment programs may result in an increase in total public expenditures at an average by 1-1.5% per year (0.010.02% of GDP) compared to the basic scenario. The necessity to fully implement the President’s May decrees will stimulate the growth of transfers to regional budgets, the financial states of which are even now worrying and should become the subject of separate consideration. From our point of view, the increase in transfers would be very difficult to avoid. Although in 2011 a significant part of articles, related to pension and social security, were reclassified from intergovernmental transfers in social policy (which we will discuss below), transfers are still a significant budget item, on which 670 billion rubles were spent in 2013. In our scenario, we are laying the increase in transfers to the regions around 20% compared to the basic scenario (for 0.1-0.2% of GDP), i.e. the increase for this budget item may reach 250 billion rubles in some years. The growth of social expenditure looks highly probable, too, especially taking into consideration the characteristics of the pension system and the demographic situation in the country. Indeed, according to the intermediate forecast of Rosstat, the number of pensioners will grow at a rate of 2%YoY in the medium term, and the number of people of working age, on the contrary, will decrease at a rate of 1%YoY. Thus, the maintenance of the current level of pensions will require the increase of social expenditures by 3% a year compared to the basic scenario (the growth for this budget items will reach 200 billion a year). The current political situation does not allow saving on defense and national security: we are predicting the 7-9% increase to the basic scenario for these © Centre of Macroeconomic Studies of Sberbank of Russia 4 SBERBANK OF RUSSIA budget items (by 0.45-0.6% of GDP, i.e. up to 600 billion rubles in different years). This corresponds well to the implementation of the modernization program of 2010-20, which includes the growth of the military department spendings by 20 trillion rubles. Therefore, we are predicting the following increase in government spending additionally to the growth in the basic scenario: 1. The growth of social expenditures (+0.1-0.2% of GDP during the 201520) and intergovernmental transfers (+0.1-0.2% of GDP); 2. The growth of spending on defense and national security (+0.45-0.6% of GDP during the period 2015-20); 3. The increase in public expenditure (+0.01-0.02% of GDP during the 201520). Indicator GDP growth Inflation Dollar exchange rate, rub Price Urals,$ Rate on internal debt Rate on external debt Federal Budget Deficit,% from GDP Proportion –internal borrowing to external Macroeconomic background Governmental expenditures 2014 0.0% 6.5% 2015 0.5% 6.0% 2016-2020 2.1% 5.1% 35.5 35.9 39.0 106 8.5% 5.0% 105 9.0% 5.0% 104 9.1% 6.0% 0.2% 1.8% 4.1$ 3:1 Scenario description Slowdown of GDP growth rate to 1.5% in mid-term; moderate inflation of ~5-6%; stable oil price of ~$104 Increase of expenses on defense, security, social services and regional support. Increase of expenses due to the integration of the Crimea to Russia The level of the government debt by the end of 2020 © Centre of Macroeconomic Studies of Sberbank of Russia ~26% of GDP 5 SBERBANK OF RUSSIA Higher expenditures will lead to budget deficit expansion, but will help accelerate the economic growth Fall in oil prices to $80 per barrel is the biggest shock to the budget Higher budget expenditure, as described above, will help to accelerate economic growth, but the acceleration is unlikely to be serious: from 1.5% to 2-2.3% in 2015-2020. However, this will help to slow down the budget deficit expansion a little and to limit the growth of the public debt. However, the federal budget deficit at the end of the reporting period will approach 5% of GDP, which will increase the cost of its financing. We suggested that the absence of strongly pronounced shocks in the public sector will help to maintain a balance between internal and external financing at the level of 3:1. The national debt grows more significantly than in the basic scenario - to 26% of GDP in 2020. This is also quite a low level that does not pose a risk to the sustainability of public finances. Stress Scenario: Fall in Oil Prices is Extremely Harmful The fall in oil prices is the most obvious risk for the Russian public finances. The direct effect from the fall in oil prices is a sharp reduction of oil-and-gas revenues, and the secondary effect hits all revenues and is connected with the deterioration of the economic situation. The third wave of deterioration is also probable within a year after the fall of prices and is invoked by the necessity to increase budget expenditures for social protection of the population from the crisis. Economic recession will be fairly profound In this scenario, we simulate the decline in oil prices to $80 per barrel in the second half of 2015 and the stabilization of prices at this level until the end of 2020. It is obvious that the decline in oil prices would be a shock for the Russian economy. The economy will decrease in the second half of 2015 and the first half of 2016 by 3%YoY, and its recovery in subsequent years will be extremely weak. The inflation will accelerate on the back of the ruble weakening in 2015-16. Oil and gas revenues will decline sharply; sovereign wealth funds will be spent in a year and a half The fall in oil prices will cause an immediate reduction in oil-and-gas revenues by $32 billion in 2015 relative to the basic scenario, which will extend the budget deficit by 2.5% of GDP in the same year (total deficit of 3.7% of GDP against 1.2% in the baseline scenario). This is the first direct effect of the deterioration of oil prices. Furthermore, our model shows that the interest costs due to the increase in financing costs and the deficit extension will increase from 0.7% of GDP in 2013-14 to 3.5% of GDP in 2020. It is obvious that the increase in debt service costs will lead to a higher budget deficit of following periods. Moreover, we assume that the recession and the slow recovery of the economy will force the government to change the structure of loans. The possibilities of borrowing on the domestic market can’t meet the increased demand for financing that, in turn, will force to borrow more on the international market. Accordingly, the proportion of loans between the internal and external markets will change from 3:1 as described in our basic scenario to 2:1. The financing of additional growth of social expenditures in 2015 and 2016 (by 2.8 and 4.7% to the basic scenario, or 110 and 200 billion, respectively) by new borrowings will also be necessary. As a result, the expansion of the budget deficit will reach a very alarming level of 7-8% of GDP and the public debt will increase to 39% of GDP by 2020. The level of debt would be even higher, but we think that the half of the budget deficit in 2015-16 will be financed by sovereign funds. Thereafter, there will be no savings therein. © Centre of Macroeconomic Studies of Sberbank of Russia 6 SBERBANK OF RUSSIA Indicator GDP growth Inflation Dollar exchange rate, rub Price Urals,$ Rate on internal debt Rate on external debt Federal Budget Deficit,% from GDP Proportion –internal borrowing to external Macroeconomic background Governmental expenditures The level of the government debt by the end of 2020 Destabilization of the public finances will require a radical revision of approaches to the budget and tax policy 2014 0.0% 6.5% 2015 -2.0% 8.5% 2016-2020 -0.3% 4.9% 35.5 37.4 39.3 106 8.5% 5.0% 90 11.8% 5.3% 80 10.4% 7.5% 0.2% 3.7% 7.1% 2:1 Scenario description GPD growth rate decreased to 0.5% in mid-term; inflation is ~5-8%; oil price is declining in the second half of 2015 to $80 and remains at this level. Reserve Fund and National Wealth Fund resources are spent on budget financing in 2015-2016 Adjustment of expenses in accordance with the change of nominal GDP growth; growth of social expenses ~39% of GDP As a result, the high budget deficit, the lack of "safety cushion" and a rapid growth of the national debt will lead to an exponential increase in risks. In addition to that, under this scenario Russia is likely to leave the countries club of investment group of ratings in 2016, which would make the financing of deficit much more expensive. In any case, this is a situation of chronic budgetary crisis, which may lead to a complete revision of the budget and tax policy basic principles. © Centre of Macroeconomic Studies of Sberbank of Russia 7 SBERBANK OF RUSSIA Application 1: Basic Scenario Description Indicator GDP growth Inflation Dollar exchange rate, rub Price Urals,$ Rate on internal debt Rate on external debt Proportion –internal borrowing to external 2014 0.0% 6.5% 2015 0.5% 6.0% 2016 1.5% 5.5% 2017 1.5% 5.0% 2018 1.5% 5.0% 2019 1.5% 5.0% 2020 1.5% 5.0% 35.5 35.9 36.5 38.0 39.5 40.0 41.2 106 8.5% 5.0% 105 9.0% 5.0% 104 8.5% 5.0% 104 8.2% 5.2% 104 8.3% 5.3% 104 8.4% 5.4% 104 8.5% 5.5% 3:1 Scenario description Macroeconomic background Governmental expenditures Indicator, % from GDP Total governmental expenditures, of them Social policy Defense and national security National economy Intergovernmental transfers Budget deficit National debt level GDP growth rate changes to 1.5% in mid-term; moderate inflation of ~5-6%; stable oil price of ~$104 Continuation of current tendencies. Increase of expenses due to the integration of the Crimea to Russia 2014 2015 2016 2017 2018 2019 2020 20.0% 20.2% 20.4% 20.6% 20.9% 20.6% 20.4% 5.1% 5.2% 5.3% 5.4% 5.4% 5.4% 5.4% 6.4% 6.5% 6.5% 6.6% 6.6% 6.2% 5.9% 3.2% 3.2% 3.2% 3.2% 3.1% 3.1% 3.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 0.2% 9.6% 1.2% 10.2% 1.9% 11.4% 2.4% 13.1% 3.0% 15.3% 3.2% 17.6% 3.3% 19.8% © Center of Macroeconomic Studies of Sberbank of Russia 8 SBERBANK OF RUSSIA Application 2: Description of the Growing Expenses Scenario Indicator GDP growth Inflation Dollar exchange rate, rub Price Urals,$ Rate on internal debt Rate on external debt Proportion –internal borrowing to external 2014 0.0% 6.5% 2015 0.5% 6.0% 2016 1.8% 5.5% 2017 2.0% 5.0% 2018 2.1% 5.0% 2019 2.1% 5.0% 2020 2.3% 5.0% 35.5 35.9 36.5 38.0 39.5 40.0 41.2 106 8.5% 5.0% 105 9.0% 5.0% 104 9.0% 5.0% 104 8.9% 5.2% 104 9.0% 5.3% 104 9.2% 5.4% 104 9.3% 5.5% 3:1 Scenario description Macroeconomic background Governmental expenditures Indicator, % from GDP Total governmental expenditures, of them Social policy Defense and national security National economy Intergovernmental transfers Budget deficit National debt level GDP growth rate slowdown to 1.5% in mid-term; moderate inflation of ~5-6%; stable oil price of ~$104 Growth of expenses on defense, security, social services and regional support. Increase of expenses due to the integration of the Crimea to Russia 2014 2015 2016 2017 2018 2019 2020 20.0% 20.9% 21.4% 21.7% 22.0% 21.7% 21.4% 5.1% 5.3% 5.4% 5.5% 5.5% 5.5% 5.5% 6.4% 6.9% 7.1% 7.1% 7.1% 6.7% 6.2% 3.2% 3.2% 3.2% 3.1% 3.1% 3.1% 3.0% 1.1% 1.2% 1.3% 1.3% 1.3% 1.3% 1.3% 0.2% 9.6% 1.8% 10.8% 3.0% 13.1% 3.7% 15.9% 4.3% 19.2% 4.7% 22.6% 4.8% 25.8% © Center of Macroeconomic Studies of Sberbank of Russia 9 SBERBANK OF RUSSIA Application 3: Description of the Growing Expenses Scenario Indicator GDP growth Inflation Dollar exchange rate, rub Price Urals,$ Rate on internal debt Rate on external debt Proportion –internal borrowing to external Macroeconomic background Governmental expenditures Indicator, % from GDP Total governmental expenditures, of them Social policy Defense and national security National economy Intergovernmental transfers Budget deficit National debt level 2014 0.0% 6.5% 2015 -2.0% 8.5% 2016 -3.0% 6.5% 2017 0.0% 4.0% 2018 0.5% 4.0% 2019 0.5% 5.0% 2020 0.5% 5.0% 35.5 37.4 38.0 38.0 39.5 40.0 41.2 106 8.5% 5.0% 90 11.8% 5.3% 80 10.9% 6.4% 80 9.5% 7.5% 80 9.6% 7.6% 80 10.8% 7.8% 80 11.1% 8.1% 2:1 Scenario description GDP growth rate changes to 0.5% in mid-term; inflation is ~5-8%; oil price declines in the second half of 2015 to $80 and remains at this level. Reserve Fund and National Wealth Fund resources are spent on budget financing in 2015-16 Adjustment of expenses in accordance with change of the nominal GDP growth; increase of social expenses 2014 2015 2016 2017 2018 2019 2020 20.0% 20.6% 21.3% 21.8% 22.5% 23.0% 23.3% 5.1% 5.4% 5.7% 5.9% 6.1% 6.1% 6.1% 6.4% 6.5% 6.5% 6.6% 6.7% 6.3% 6.0% 3.2% 3.2% 3.2% 3.2% 3.1% 3.1% 3.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 1.1% 0.2% 9.6% 3.7% 10.9% 5.9% 13.9% 6.3% 19.7% 7.0% 25.8% 7.8% 32.3% 8.4% 39.0% © Center of Macroeconomic Studies of Sberbank of Russia 10 SBERBANK OF RUSSIA Overview prepared by Yulia Tseplyaeva Director of Center of Macroeconomic Studies [email protected] Aleksey Kiselev Leading analyst [email protected] You can direct your questions to the CMS via phone number (495) 747–38–79 or the aforementioned Email. Standard disclaimer that is attached compulsorily to all analytical products Disclaimer The data presented herein should not be considered a recommendation of investment. The information is provided solely for educational purposes. Any information contained herein is exploratory in its nature and is not an offer, request, requirement or recommendation to buy, sell, or provide (directly or indirectly) the securities, or their derivatives. The sale or purchase of securities cannot be carried out on the basis of the information and prices contained herein. The information contained in this document may not be used as the basis for any legally binding commitments or agreements, including, but not limited to an obligation to update this information. It may not be reproduced, distributed or published by any person for the purpose of any proposals, motivations, requirements or recommendations to subscribe, purchase or sale any securities or derivatives thereof. It is assumed that everyone who received this information, has conducted their own investigation and made their own assessment of the prospects of investments in the instruments mentioned in this document. Sberbank of Russia does not assume any liability for any direct or consequential loss, damage or costs incurred in connection with the use of the information contained in this document, including the submitted data. Information may not be considered recommendatory for specific investment policy or as a recommendation of any other sort. The information cannot be regarded as liability, warranty claim, commitment, offer, advice, counseling, etc. The Bank is not liable for the consequences incurred by third parties using the information contained in this document. The Bank has the right to change the information contained in this document at any time and without notice. Third parties (investors, shareholders, etc.) must independently assess the economic risks and benefits of the transaction (services), tax, legal, accounting consequences and opportunities to take such risks. The Bank does not guarantee the accuracy, completeness or adequacy of reproducing information by third parties and disclaims responsibility for errors or omissions committed by them while reproducing the information. The information contained herein cannot be interpreted as a bid/offer or as a recommendation/advice on investment, legal, tax, banking and other issues. Please contact a specialist for professional advice. © Center of Macroeconomic Studies of Sberbank of Russia 11