Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

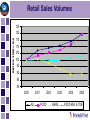

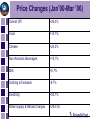

‘The Changing Retail Environment – An Economic Outlook’ FDII Annual Conference APRIL 27th 2006 Jim Power Chief Economist Friends First To Be Discussed • • • • • Key Themes for Irish Economy Irish Economic Background & Outlook The Big Economic Issues Consumer Dynamics Context for the Food & Drinks Industry • Official Policy Implications Key Themes • Solid external economic background • Rising interest rates • Exchange rates relatively stable, but modest euro appreciation likely • Buoyant housing market • Increased indebtedness • SSIAs • What are the risk factors? What to Watch • • • • • • Oil Prices Geo-Political turmoil US twin deficits & currency instability Chinese Imbalances Housing bubbles Too much aggression from paranoid ECB Financial Conditions • ECB rate tightening to continue • 1 ¼ % by end-2007 • Another 0.25% from Fed, BOE could cut • Exchange rate markets very stable, but • Euro should make some gains against sterling & dollar The Irish Economy • Strong momentum has carried over to 2006 • Consumer spending, Construction & Business Investment strong • Exports/Manufacturing finding life challenging • Strong public finances, another ‘budget bonanza’ in December • SSIAs will exert considerable influence over the next year • Growth prospects 2006 & 2007 good Forecasts 2005e 2006f 2007f GDP 4.5% 5.2% 4.7% GNP 4.8% 4.9% 4.4% Consumption 5.8% 7.0% 6.5% Investment 8.0% 7.0% 6.0% Exports 3.0% 4.8% 4.5% Inflation 2.5% 3.2% 2.9% Unemployment 4.4% 4.3% 4.4% Housing Completions 80,974 82,000 75,000 Where is Ireland Today? • Has come through a decade of strong growth • Growth momentum still strong, but nature of economy is changing • Rapid economic catch-up has highlighted deficiencies • Competitiveness has been undermined • Significant dependence on residential housing market • Manufacturing & Agriculture under pressure Significance of Housing Market • Construction activity & direct employment • Construction output valued at €30 bln, Housing 65% • Mortgage market has grown from €25 bln to €100 bln in 6 years • Major driver of financial sector employment • Important contributor to tax take directly & indirectly • VAT €2.6 bln, & Stamps €800 mln • Equity market effect • Housing stock valued at €530 bln, significant consumer ‘wealth effect’ A MM JJaupayrA SOueun--997 DNJeocgptl---9997 Feacv-9777 A MM abnr-999 7 p J a A SOJueuuyn---9988 DNJeocgptl---99988 Feacv-988 A MM abn-999 8 p J a AJuuuynr--99 S Neocgpl---999999 DO Jeactv- 999 FM eabn--99 MA p J A SOJueauuynr---0000900 DNJeocgptl---00000 Feacv 000 A MM abnr--000 0 p J a A SOJueuuyn---001 DNJeocgptl---000111 Feacv 011 A MM abnr--000 1 p J a A SOJueuuyn---0022 DNJeocgptl---0002 Feacv-0222 A MM abn-000 2 p J a A SOJueuuynr---0033 DNJeocgptl---00033 Feacv-033 A MM JJaupabynr--00034 A SOueun--004 DNJeocgptl---00044 Feacv-044 A MM abnr-0004 p J a A SOJueuuyn---005 DNJeocgptl---000555 Feacv 055 bn--00 5 06 140 120 100 80 60 40 20 0 35 30 25 20 15 10 5 0 CONSUMER CONFIDENCE HOUSE PRICE GROWTH % House Prices & Consumer Confidence The Housing Market in 2006 • Frenetic start to year • Demand forces to remain strong • Interest rates will have no more than a modest sobering effect • SSIAs will have an important influence • Completions of around 82,000 • Prices set to rise by 8% + • Residential housing will be an important driver of activity once again Near-Term Consumer Dynamics • • • • • • • Very expansionary fiscal background Strong labour market SSIAs Growing population Increased affluence Inflationary pressures picking up Interest rates rising Medium-Term Consumer Dynamics • Medium-Term growth of 5% p/a • Strong labour market, but quality of jobs more important than quantity • Rising population • Inward migration • Young age profile – higher spenders • Increased consumer power • Balance between taxation and public spending Changing Age Structure AGE 2001 2006 2021 2036 0-14 21.5% 20.8% 19.8% 16.0% 15-34 31.9% 31.2% 23.4% 23.6% 35-49 20.7% 21.1% 23.1% 16.9% 50-64 14.7% 15.7% 18.4% 21.6% 65+ 11.2% 11.2% 15.3% 21.9% Contributors to Pop. Change 80,000 60,000 40,000 20,000 0 -20,000 1971-79 1979-81 1981-86 1986-91 1991-96 -40,000 BIRTHS DEATHS NET MIGRATION 1996-02 Employment Changes SECTOR Q4 2003 to Q4 2005 Agriculture -8,100 Other Production -9,100 Construction +52,600 Hotels & Restaurants +100 Financial & Business Services +31,700 Wholesale & Retail Trade +28,500 Education +9,800 Health +15,700 TOTAL +151,700 Manufacturing Output 16 14 12 10 % 8 6 4 2 0 2000 2001 2002 2003 2004 2005 Manufacturing Growth Divergence 25 20 15 MODERN % 10 TRAD 5 0 -5 2000 2001 2002 2003 2004 2005 Manufacturing Output Prices (ex VAT) INDEX 2000=100 104 102 100 98 96 94 92 90 88 86 84 2000 2001 2002 2003 2004 2005 INDEX 2000=100 Retail Sales Volumes 125 120 115 110 105 100 95 90 85 80 2000 2001 ALL 2002 FOOD 2003 BARS 2004 2005 FOOD BEV & TOB Price Changes (Jan’00-Mar ’06) Overall CPI +26.0% Food +14.7% Cheese +24.3% Non-Alcoholic Beverages +15.1% Milk +5.7% Clothing & Footwear -9.7% Electricity +52.7% Water Supply & Refuse Charges +239.3% Consumer Issues • ‘Rip-Off Ireland’ – a major myth! • Consumer getting a more powerful, informed & demanding voice • Health Issues • Price v Quality • The Groceries Order • Planning Guidelines • Consumer demandinhg lower prices & different type of shopping experience • International competition will continue to grow to exploit one of the most vibrant consumer markets in Europe The Future • Growing population, strong inward migration • Changing demographics • Economic outlook positive, notwithstanding obvious challenges • Increased affluence, but changing spending patterns • Price awareness will continue to rise • Health issues will become more important • Globalisation & competition issues for every sector of economy, particularly retail sector THANK YOU