Survey

* Your assessment is very important for improving the work of artificial intelligence, which forms the content of this project

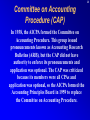

Chapter 1 The Environment of Financial Reporting Intermediate Accounting 10th edition Nikolai Bazley Jones An electronic presentation by Norman Sunderman Angelo State University COPYRIGHT © 2007 Thomson South-Western, a part of The Thomson Corporation. Thomson, the Star logo, and South-Western are trademarks used herein under license. 2 Printing PowerPoint The options for printing are Color, Grayscale, and Pure Black and White. For best results select PURE BLACK and WHITE on the print page. 3 More Accountants Needed New accounting rules pose challenges for financial accounting and projections point to increased hiring of accounting graduates. 4 Estimated Hiring Increase Accounting firms of all sizes plan to increase future hiring. 5 Companies need large amounts of capital for operations 6 Companies may obtain capital by issuing capital stock... Stock Exchange 7 …or by borrowing from lenders Bank 8 Capital Markets Corporations Sell stocks and bonds Primary Market (e.g., individuals,Investors banks) Borrow money Financial Institutions Buy and sell stocks and bonds Secondary Market (e.g., New York Stock Investors Exchange) Buy and sell stocks and bonds Buy and sell stocks and bonds Investors Accounting Information Economic Activities and Decision Making 9 Impact External User Company’s Economic Activities Accumulate Accounting Information Communicate Internal User Impact Externa l Decisio n Making Internal Decisio n Making 10 External and Internal Users 1. Buy. A potential investor decides to purchase a particular security on the basis of communicated accounting information. 2. Hold. An actual investor decides to retain a particular security on the basis of communicated accounting information. 3. Sell. An actual investor decides to dispose of a particular security on the basis of communicated accounting information. 11 Comparison of Financial and Managerial Accounting Sources of Authority Financial Accounting Managerial Accounting Internal needs GAAP 12 Comparison of Financial and Managerial Accounting Time Frame of Reported Information Financial Accounting Primarily historical Managerial Accounting Present and future 13 Comparison of Financial and Managerial Accounting Scope Financial Accounting Total company & Segment reporting Managerial Accounting Individual departments, divisions, and total company 14 Comparison of Financial and Managerial Accounting Type of Information Financial Accounting Managerial Accounting Primarily quantitative Qualitative as well as quantitative 15 Comparison of Financial and Managerial Accounting Statement Format Financial Accounting Prescribed by GAAP; oriented toward investment and credit decisions Managerial Accounting Determined by company; focused upon specific decisions being made 16 Comparison of Financial and Managerial Accounting Decision Focus Financial Accounting External Managerial Accounting Internal 17 The company’s accountants prepare both the financial and the managerial accounting reports… …and the information comes from the same information system. 18 Financial Reporting Financial reporting is the process of communicating financial accounting information about a company to external users. 19 Financial Reporting A statement of changes in stockholders’ equity also is included by many companies. 20 Financial Reporting This statement summarizes the changes in each item of stockholders’ equity for a period. 21 Generally Accepted Accounting Principles (GAAP) GAAP are the guidelines, procedures, and practices that a company is required to use in recording and reporting the accounting information in its audited financial statements. 22 Hierarchy of Sources of GAAP Categories Authoritative Sources A. FASB Statements of Financial Accounting Standards and Interpretations, FASB Staff Positions, FASB Statement 133 Implementation Issues, APB Opinions, and CAP (AICPA) Accounting Research Bulletins, (as well as SEC releases such as regulation SX, Financial Reporting releases, and Staff Accounting Bulletins for companies that file with the SEC) Continued 23 Hierarchy of Sources of GAAP Categories Authoritative Sources B. FASB Technical Bulletins, and, if cleared by the FASB, AICPA Industry Audit and Accounting Guides, and AICPA Statements of Position C. FASB Emerging Issues Task Force Consensus Positions and if cleared by the FASB, AICPA Practice Bulletins Continued 24 Hierarchy of Sources of GAAP Categories Authoritative Sources D. FASB Q’s and A’s (Implementation Guides), AICPA Accounting Interpretations, and practices that are widely recognized and prevalent either generally or in the industry (e.g., AICPA Accounting Trends and Techniques) There are electronic databases such as the FASB Financial Accounting Research System (FARS) that include most accounting standards 25 History of GAAP in Private Sector 1938 1959 1973 CAP formed APB formed FASB formed CAP issued 51 ARBs APB issued 31 Opinions Present FASB issued 154 Statements of Standards as of 10/05 26 Committee on Accounting Procedure (CAP) In 1938, the AICPA formed the Committee on Accounting Procedure. This group issued pronouncements known as Accounting Research Bulletins (ARB), but the CAP did not have authority to enforce its pronouncements and application was optional. The CAP was criticized because its members were all CPAs and application was optional, so the AICPA formed the Accounting Principles Board in 1959 to replace the Committee on Accounting Procedure. 27 Reasons for Forming APB 1. To alleviate criticism about the process of formulating accounting principles, which included wider representation. 2. To create a policy-making body whose rules would be binding on companies rather than optional. The APB was comprised 17 to 21 members, selected primarily from the accounting profession. 28 Structure of FASB Financial Accounting Foundation (16-member board of trustees) Appoint, fund, and oversee Financial Accounting Standards Advisory Council (approximately 30 members) Advise Financial Accounting Standards Board (7 members) Continued 29 Structure of the FASB Financial Accounting Standards Board (7 members) Appoint Consult Task Forces of the Standards Board (including Emerging Issues Task Force) Support Administrative Staff Research and Technical Staff Consult 30 Types of Pronouncements Issued by the FASB Statements of Financial Accounting Standards Interpretations Technical Bulletins Statements of Financial Accounting Concepts Other Pronouncements 31 FASB Operating Procedures Identify Topic Appoint Task Force Conduct Research Issue Discussion Memorandum or Invitation to Comment Hold Public Hearings Deliberate on Findings Issue Exposure Draft Continued 32 FASB Operating Procedures Hold Public Hearings Modify Exposure Drafts From previous page Issue Exposure Draft Vote (simple majority) Issue Statement 33 Principles of the AICPA Code of Professional Conduct Responsibilities In carrying out their responsibilities as professionals, members should exercise sensitive professional judgment in all their activities. 34 Principles of the AICPA Code of Professional Conduct The Public Interest Members should accept the obligation to act in a way that will serve the public interest, honor the public trust, and demonstrate commitment to professionalism. 35 Principles of the AICPA Code of Professional Conduct Integrity To maintain and broaden public confidence, members should perform all professional responsibilities with the highest sense of integrity. 36 Principles of the AICPA Code of Professional Conduct Objectivity and Independence A member should maintain objectivity and be free from conflicts of interest in discharging professional responsibilities. A member in public practice should be independent in fact and appearance. 37 Principles of the AICPA Code of Professional Conduct Due Care A member should observe the profession’s technical and ethical standards, strive continually to improve competence and the quality of services, and discharge the professional responsibility to the best of the member’s ability. 38 Principles of the AICPA Code of Professional Conduct Scope and Nature of Service A member in public practice should observe the Principles of the CPC in determining the scope and nature of services to be provided. 39 Chapter 1 Task Force Image Gallery clip art included in this electronic presentation is used with the permission of NVTech Inc.