How Do We Know That We Know? The Accessibility Model

... memory. Evidence from 3 experiments is presented. The results challenge the view that FOK is based on a direct, privileged access to an internal monitor. ...

... memory. Evidence from 3 experiments is presented. The results challenge the view that FOK is based on a direct, privileged access to an internal monitor. ...

APPTICATION OF THE AUDIT PROCESS TO OTHER CYCTES

... is commonly used to pay for the acquisition when payment is due. Most companies use computer-prepared checks based on information included in the acquisition transactions file at the time goods and services are received. Checks are typically prepared in a multi-copy format, with the original going t ...

... is commonly used to pay for the acquisition when payment is due. Most companies use computer-prepared checks based on information included in the acquisition transactions file at the time goods and services are received. Checks are typically prepared in a multi-copy format, with the original going t ...

Revised Guidance Statement GS 009: Auditing SMSFs

... useful in planning, conducting and reporting their audits, but it does not relate specifically to APRA funds. See Division 1, Section 6 of the SISA. Regulated funds, under section 19 of the SISA, are funds which have a trustee, either a corporate trustee or governing rules which contain a pension fu ...

... useful in planning, conducting and reporting their audits, but it does not relate specifically to APRA funds. See Division 1, Section 6 of the SISA. Regulated funds, under section 19 of the SISA, are funds which have a trustee, either a corporate trustee or governing rules which contain a pension fu ...

Auditing for Fraud Detection - Professional Education Services

... Chapter 1 has been designed to heighten your familiarity with the nature, signs, prevention, detection and reaction to fraud that can enable you to perform financial statement audits with awareness of fraud possibilities. Chapter 2 defines and explains internal controls as they affect financial reco ...

... Chapter 1 has been designed to heighten your familiarity with the nature, signs, prevention, detection and reaction to fraud that can enable you to perform financial statement audits with awareness of fraud possibilities. Chapter 2 defines and explains internal controls as they affect financial reco ...

Substantive Tests of Transactions and Balances

... effective means of auditing the financial report of a small business. It is especially efficient if the auditor designs effective analytical tests for those specific audit objectives, such as statement of financial performance, account classification and those related to the completeness assertion, ...

... effective means of auditing the financial report of a small business. It is especially efficient if the auditor designs effective analytical tests for those specific audit objectives, such as statement of financial performance, account classification and those related to the completeness assertion, ...

User guide to Standing Direction 1

... Certification takes place annually from July to September each year. An overview of the annual certification process can be found within this section. ...

... Certification takes place annually from July to September each year. An overview of the annual certification process can be found within this section. ...

Data mining journal entries for fraud detection: A Pilot Study

... Perhaps the most interesting aspect of the WorldCom case from the perspective of this paper is the statement that “WorldCom personnel also repeatedly rejected Andersen’ s requests for access to the computerized General Ledger through which Internal Audit and others discovered the cap ...

... Perhaps the most interesting aspect of the WorldCom case from the perspective of this paper is the statement that “WorldCom personnel also repeatedly rejected Andersen’ s requests for access to the computerized General Ledger through which Internal Audit and others discovered the cap ...

Does the Big-4 Effect Exist when Reputation and

... We find evidence consistent with a Big-4 effect. For partners switching to Big-4 firms, we find higher going-concern reporting accuracy, less earnings management, and higher audit fees after they switch. We observe an immediate increase in the accuracy of the going-concern reports (i.e., in the swi ...

... We find evidence consistent with a Big-4 effect. For partners switching to Big-4 firms, we find higher going-concern reporting accuracy, less earnings management, and higher audit fees after they switch. We observe an immediate increase in the accuracy of the going-concern reports (i.e., in the swi ...

Defence Audit Guidelines_Final 25 March 2010

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

Dimensions of integration in embedded and extended cognitive

... analyse agent-artifact relations, it should be equally useful to analyse agent-agent systems. Conceptual and empirical research on socially embedded or distributed cognitive systems (e.g. Tollefson et al. 2013; Theiner 2013) would thus also benefit from this framework. Second, conceiving of situated ...

... analyse agent-artifact relations, it should be equally useful to analyse agent-agent systems. Conceptual and empirical research on socially embedded or distributed cognitive systems (e.g. Tollefson et al. 2013; Theiner 2013) would thus also benefit from this framework. Second, conceiving of situated ...

(revised) compilation engagements

... form of agreement (such as financial information provided to a funding body to support provision or continuation of a grant). For transactional purposes, for example to support a transaction involving changes to the entity’s ownership or financing structure (such as for a merger or acquisition). ...

... form of agreement (such as financial information provided to a funding body to support provision or continuation of a grant). For transactional purposes, for example to support a transaction involving changes to the entity’s ownership or financing structure (such as for a merger or acquisition). ...

The Effect of Audit Firm Specialization on Earnings Management

... The demand for auditing in capital markets can be analyzed from three perspectives (i.e., a monitoring role, an information role and an insurance role) (Wallace, 1981). How the auditor fulfils these roles determines the level of audit quality (Fernando et al., 2010). Audit quality is an important m ...

... The demand for auditing in capital markets can be analyzed from three perspectives (i.e., a monitoring role, an information role and an insurance role) (Wallace, 1981). How the auditor fulfils these roles determines the level of audit quality (Fernando et al., 2010). Audit quality is an important m ...

report (text only) - RTF 202Kb - Opens in a new

... decision-making and scrutiny are still bedding in and councils need to keep them under review to make sure they are effective. The report shows that councillors are receiving training and councils need to build on this to support them in their new and developing roles, especially in strategic leader ...

... decision-making and scrutiny are still bedding in and councils need to keep them under review to make sure they are effective. The report shows that councillors are receiving training and councils need to build on this to support them in their new and developing roles, especially in strategic leader ...

Yes, there is a big Difference between Audit on Profit Organizations

... material misstatements - a concept influenced by both quantitative (numerical) and qualitative factors. Auditing is a vital part of accounting. Traditionally, audits were mainly associated with gaining information about financial systems and the financial records of a company or a business. However, ...

... material misstatements - a concept influenced by both quantitative (numerical) and qualitative factors. Auditing is a vital part of accounting. Traditionally, audits were mainly associated with gaining information about financial systems and the financial records of a company or a business. However, ...

English - EDUCatt

... pronunciation and include a considerable amount of authentic texts provided by ENI. This means that the book should prepare would-be auditors for the texts that they will meet once they are within the corporate context. Auditing is a profession which requires good interpersonal skills, and this is r ...

... pronunciation and include a considerable amount of authentic texts provided by ENI. This means that the book should prepare would-be auditors for the texts that they will meet once they are within the corporate context. Auditing is a profession which requires good interpersonal skills, and this is r ...

Notification 297/2015 dated 28th December, 2015 - Regarding the Internal Audit Manual (672 KB)

... Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk man ...

... Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps the organization to accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk man ...

ch02_sm_rankin

... representationally faithful (i.e. how would you audit this information, particularly in relation to completeness). The incorporeal nature of items such as (for items such as human capital, innovations) necessarily means that in many instances identifying these and deciding on what impact or signi ...

... representationally faithful (i.e. how would you audit this information, particularly in relation to completeness). The incorporeal nature of items such as (for items such as human capital, innovations) necessarily means that in many instances identifying these and deciding on what impact or signi ...

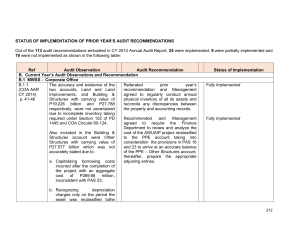

MWSS2015_Part3-Status_of_PY`s_Recomm

... Structures with carrying value of physical inventory of all its assets and P19.226 billion and P27.788 reconcile any discrepancies between respectively, were not ascertained the property and accounting records. due to incomplete inventory taking required under Section 102 of PD Recommended and Manag ...

... Structures with carrying value of physical inventory of all its assets and P19.226 billion and P27.788 reconcile any discrepancies between respectively, were not ascertained the property and accounting records. due to incomplete inventory taking required under Section 102 of PD Recommended and Manag ...

MANDATORY EMPHASIS PARAGRAPHS, CLARIFYING

... uncertainty, etc.). The PCAOB’s proposal, therefore, reflects the notion that disclosure of the most significant matters that the auditor encounters during the audit within the actual body of audit report will increase the relevance of the audit report. While the Big 4 audit firms agree that the ide ...

... uncertainty, etc.). The PCAOB’s proposal, therefore, reflects the notion that disclosure of the most significant matters that the auditor encounters during the audit within the actual body of audit report will increase the relevance of the audit report. While the Big 4 audit firms agree that the ide ...

Comprehensive Case A.1 – Enron

... reliability. The relevance of audit evidence specifically relates to whether the evidence gathered actually relates to the financial statement assertion being tested. That is, will the evidence allow the auditor to reach conclusions related to that financial statement assertion? The reliability of t ...

... reliability. The relevance of audit evidence specifically relates to whether the evidence gathered actually relates to the financial statement assertion being tested. That is, will the evidence allow the auditor to reach conclusions related to that financial statement assertion? The reliability of t ...

hall, accounting information systems

... ©2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. ...

... ©2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. ...

Dialogue Games for Inconsistent and Biased Information

... with u, t, f and i respectively. Truth-value t (1∼0) represents full evidence for believing and no evidence for disbelieving; this is considered the orthodox ‘true’ from classical logic. Opposite to true is truth-value f (0∼1) that represents no evidence for believing but maximal evidence for disbel ...

... with u, t, f and i respectively. Truth-value t (1∼0) represents full evidence for believing and no evidence for disbelieving; this is considered the orthodox ‘true’ from classical logic. Opposite to true is truth-value f (0∼1) that represents no evidence for believing but maximal evidence for disbel ...

Conceptual Framework for General Purpose Financial

... Conceptual Framework) will establish and make explicit the concepts that are to be applied in developing International Public Sector Accounting Standards (IPSASs) and other documents that provide guidance on information included in general purpose financial reports (GPFRs). IPSASs are developed to a ...

... Conceptual Framework) will establish and make explicit the concepts that are to be applied in developing International Public Sector Accounting Standards (IPSASs) and other documents that provide guidance on information included in general purpose financial reports (GPFRs). IPSASs are developed to a ...

Auditor Liability and Professional Skepticism: A Look at Lehman

... The key to effective auditing: maintaining professional skepticism The role assigned to auditors in our society is as examiners of the financial statements prepared by company management, followed by the expression of opinions as to whether those financial statements have been fairly presented in ac ...

... The key to effective auditing: maintaining professional skepticism The role assigned to auditors in our society is as examiners of the financial statements prepared by company management, followed by the expression of opinions as to whether those financial statements have been fairly presented in ac ...