Guide to Certifications

... Certified Government Auditing Professional (CGAP) – A specialty certification program issued by The Institute of Internal Auditors (The IIA), the CGAP is designed for audit practitioners in the public sector. The certification exam tests a candidate’s knowledge of public sector auditing, including c ...

... Certified Government Auditing Professional (CGAP) – A specialty certification program issued by The Institute of Internal Auditors (The IIA), the CGAP is designed for audit practitioners in the public sector. The certification exam tests a candidate’s knowledge of public sector auditing, including c ...

5 ACCOUNTING FOR

... these changes is the accounting profession that must provide reliable and relevant information to users. This chapter introduces accounting to the student as the means of providing the information to support such decisions. Two broad types of accounting information, financial and internal are introd ...

... these changes is the accounting profession that must provide reliable and relevant information to users. This chapter introduces accounting to the student as the means of providing the information to support such decisions. Two broad types of accounting information, financial and internal are introd ...

Assignment 1 is compulsory and due

... extract sample of trade receivables at year-end and also list of payments from masterfile after year-end and compare with the source documents to confirm is before year-end and that the trade receivables do exist at yearend extract a list of debtors who have a hold on their account or who have e ...

... extract sample of trade receivables at year-end and also list of payments from masterfile after year-end and compare with the source documents to confirm is before year-end and that the trade receivables do exist at yearend extract a list of debtors who have a hold on their account or who have e ...

ISA 520 Analytical procedures

... The auditor may consider testing the operating effectiveness of controls, if any, over the entity’s preparation of information used by the auditor in performing substantive analytical procedures in response to assessed risks. When such controls are effective, the auditor generally has greater confid ...

... The auditor may consider testing the operating effectiveness of controls, if any, over the entity’s preparation of information used by the auditor in performing substantive analytical procedures in response to assessed risks. When such controls are effective, the auditor generally has greater confid ...

The interaction of focus particles and information structure in

... of whether an adult-like performance was found or not, children were consistently found to perform better on FP-sentences when the focused constituent was in a sentence final position like (1) than in sentence initial position like (2). (2) Nur [der Elefant]focus hat einen Ballon. Only [the elephant ...

... of whether an adult-like performance was found or not, children were consistently found to perform better on FP-sentences when the focused constituent was in a sentence final position like (1) than in sentence initial position like (2). (2) Nur [der Elefant]focus hat einen Ballon. Only [the elephant ...

The Auditor - Whose Agent Is He Anyway

... the objectives of management and the owners. A mandatory provision was made in the Companies Act 1963: … every company shall at each annual general meeting appoint an auditor or auditors to hold office from the conclusion of that until the conclusion of the next annual general meeting (Companies Act ...

... the objectives of management and the owners. A mandatory provision was made in the Companies Act 1963: … every company shall at each annual general meeting appoint an auditor or auditors to hold office from the conclusion of that until the conclusion of the next annual general meeting (Companies Act ...

Leading Practice Examples of Audit Committee Reporting

... Internal Audit should also be prepared to attend the Executive Session, where outside Board members can question internal and external audit without the presence of Senior Management. ...

... Internal Audit should also be prepared to attend the Executive Session, where outside Board members can question internal and external audit without the presence of Senior Management. ...

working program - Almaty Management University

... The working curriculum was reviewed at the meeting of the Department of “Valuation, accounting and audit” Protocol №1 from “25” August 2014. Head of the department “Valuation, accounting and audit” c.ec.s., Docent_____________________ ...

... The working curriculum was reviewed at the meeting of the Department of “Valuation, accounting and audit” Protocol №1 from “25” August 2014. Head of the department “Valuation, accounting and audit” c.ec.s., Docent_____________________ ...

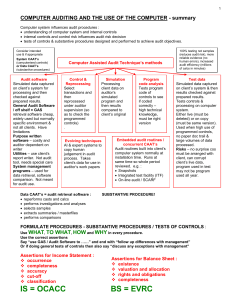

the relevance of auditing in a computerized accounting system

... perform other operations. Every company adopt the accounting system method of recording of transaction, because it is generally required that companies have to reveal certain financial and management information to the government and public users; and also because accounting is an indispensable tool ...

... perform other operations. Every company adopt the accounting system method of recording of transaction, because it is generally required that companies have to reveal certain financial and management information to the government and public users; and also because accounting is an indispensable tool ...

Scientific Visualization versus Information Visualization

... the original dataset. This requirement is not listed above, which makes VTK unsuitable for Information Visualization. However, many Scientific Visualization analysts study “Computational Steering,” with which feedback can be given to running simulations, based on visualizations of early results from ...

... the original dataset. This requirement is not listed above, which makes VTK unsuitable for Information Visualization. However, many Scientific Visualization analysts study “Computational Steering,” with which feedback can be given to running simulations, based on visualizations of early results from ...

internal-auditing-instructional-material

... Work is to be adequately planned Assistants are to be properly supervised A review is to be made of compliance with applicable laws & regulation During the audit, a study and evaluation shall be made of internal control systemadmin control ) applicable to the organization program, activity, or funct ...

... Work is to be adequately planned Assistants are to be properly supervised A review is to be made of compliance with applicable laws & regulation During the audit, a study and evaluation shall be made of internal control systemadmin control ) applicable to the organization program, activity, or funct ...

THE IMPORTANCE OF ACCOUNTING INFORMATION IN CRISIS TIMES

... other channels than the written form (Internet, database, green phone). Green phone free call can work permanently or temporarily, providing information to external users. The Internet is information medium providing information directly, in short time and inexpensive10. Free access to information l ...

... other channels than the written form (Internet, database, green phone). Green phone free call can work permanently or temporarily, providing information to external users. The Internet is information medium providing information directly, in short time and inexpensive10. Free access to information l ...

Best management practices for nitrogen in intensive pasture

... Formulas, algorithms, models Data required Accounting protocols » Consistent with NGGI methods » Based on peer reviewed science » Top down and bottom up align ...

... Formulas, algorithms, models Data required Accounting protocols » Consistent with NGGI methods » Based on peer reviewed science » Top down and bottom up align ...

Answers

... Obtain a listing of trade payables from the purchase ledger and agree to the general ledger and the financial statements. Reconcile the total of purchase ledger accounts with the purchase ledger control account, and cast the list of balances and the purchase ledger control account. Review the list o ...

... Obtain a listing of trade payables from the purchase ledger and agree to the general ledger and the financial statements. Reconcile the total of purchase ledger accounts with the purchase ledger control account, and cast the list of balances and the purchase ledger control account. Review the list o ...

Competency area - Chartered Institute of Internal Auditors

... Can demonstrate that the IIA’s code of ethics is applied in every audit assignment so that information is kept confidential, audit work is only undertaken where the auditor is competent to do so, conflicts of interest are disclosed, and the auditor acts objectively in all situations, ensuring that w ...

... Can demonstrate that the IIA’s code of ethics is applied in every audit assignment so that information is kept confidential, audit work is only undertaken where the auditor is competent to do so, conflicts of interest are disclosed, and the auditor acts objectively in all situations, ensuring that w ...

Part II. Essay Questions (60%)

... 13. Which of the following is not one of the principal CPA firm’s alternatives when issuing a report if a different CPA firm performed part of the audit? a. Issue a joint report signed by both CPA firms. b. Make no reference to the other CPA in the audit report, and issue the standard unqualified op ...

... 13. Which of the following is not one of the principal CPA firm’s alternatives when issuing a report if a different CPA firm performed part of the audit? a. Issue a joint report signed by both CPA firms. b. Make no reference to the other CPA in the audit report, and issue the standard unqualified op ...

Sample September / December 2015 answers

... Payment in advance and revenue recognition under contract with customers For items where significant design work is needed, Dali Co receives a payment in advance. This gives rise to risk in terms of when that part of the revenue generated from a sale of goods is recognised. There is a risk that reve ...

... Payment in advance and revenue recognition under contract with customers For items where significant design work is needed, Dali Co receives a payment in advance. This gives rise to risk in terms of when that part of the revenue generated from a sale of goods is recognised. There is a risk that reve ...

III Local audit of project accounts

... the separation of conflicting or important functions and processes such as commitment to obligations, signing and recording of expenses, matching of cash and bank account balances, clarification of long-term unsettled receivables and obligations, physical existence of material goods, etc. Existenc ...

... the separation of conflicting or important functions and processes such as commitment to obligations, signing and recording of expenses, matching of cash and bank account balances, clarification of long-term unsettled receivables and obligations, physical existence of material goods, etc. Existenc ...

information technology problems in the context of logic of science

... primarily the financial one, because "the developing technology cannot be interested in a stable financial position, it is actively involved in the area of finance in order to undermine their stability"; "a technician is likely to have a technical approach to finance issues" [18, p.146]. In this ca ...

... primarily the financial one, because "the developing technology cannot be interested in a stable financial position, it is actively involved in the area of finance in order to undermine their stability"; "a technician is likely to have a technical approach to finance issues" [18, p.146]. In this ca ...

2015-230 Presentation of Financial Statements of Not-for

... b. Composition of net assets with donor restrictions at the end of the period and how the restrictions affect the use of resources. Disagree in part – narrative about how the composition affects the use of resources is subjective, may be duplicative of information already in the financials and adds ...

... b. Composition of net assets with donor restrictions at the end of the period and how the restrictions affect the use of resources. Disagree in part – narrative about how the composition affects the use of resources is subjective, may be duplicative of information already in the financials and adds ...

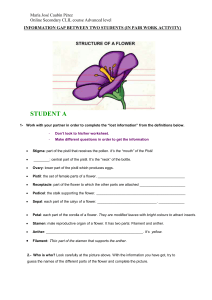

information gap between two students (in pair

... gaps are completed, they have to guess “who is who” in the picture of a flower. DEVELOPMENT OF THE ACTIVITY First step: The teacher should explain the activity, and read aloud the common part of the worksheets. Second step: Students are grouped in pairs, working together in order to gather all the i ...

... gaps are completed, they have to guess “who is who” in the picture of a flower. DEVELOPMENT OF THE ACTIVITY First step: The teacher should explain the activity, and read aloud the common part of the worksheets. Second step: Students are grouped in pairs, working together in order to gather all the i ...

Auditor`s Responsibility

... Financial Statement Certifications • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all kno ...

... Financial Statement Certifications • Management responsible for preventing and detecting fraud • Management can override internal controls and create deceptive accounting • Management representation letters from CEO, CFO, and other appropriate officers (SOX requirements) – Provided access to all kno ...

November 12, 2014 International Ethics Standards Board for

... the proposal, IESBA evaluates whether the current time-on/time-off period of 7/2 remains appropriate to address the treat of long association for key audit partners (KAPs) of a public interest entity (PIE). We agree with the IESBA of the need to propose changes to increase the cooling-off period for ...

... the proposal, IESBA evaluates whether the current time-on/time-off period of 7/2 remains appropriate to address the treat of long association for key audit partners (KAPs) of a public interest entity (PIE). We agree with the IESBA of the need to propose changes to increase the cooling-off period for ...

Audit Committee 18 September 2012

... compared to the previous year in terms of reporting requirements, changes are detailed within section 3 of the explanatory foreword. ...

... compared to the previous year in terms of reporting requirements, changes are detailed within section 3 of the explanatory foreword. ...