Budget Justification Form

... Policies for more details. Local Telephone Costs Local telephone costs (defined as all expenses other than long distance calls) are not allowable as direct costs on federal/federal flow-through projects. This includes the monthly use charges on equipment, installation, line charges, maintenance, pag ...

... Policies for more details. Local Telephone Costs Local telephone costs (defined as all expenses other than long distance calls) are not allowable as direct costs on federal/federal flow-through projects. This includes the monthly use charges on equipment, installation, line charges, maintenance, pag ...

Review of key topics

... significant amounts of indirect costs are now allocated using only one or two cost pools. all or most costs are identified as output unitlevel costs. products make diverse demands on resources because of differences in volume, process steps, batch size, or complexity. ...

... significant amounts of indirect costs are now allocated using only one or two cost pools. all or most costs are identified as output unitlevel costs. products make diverse demands on resources because of differences in volume, process steps, batch size, or complexity. ...

UWA Full Costing on External Research Grants

... Full costing can also be calculated on the basis of base salary only, as is often the case when negotiating collaborative arrangements for Cooperative Research Centres where a 3 times multiplier is suggested. At UWA: Full costs ...

... Full costing can also be calculated on the basis of base salary only, as is often the case when negotiating collaborative arrangements for Cooperative Research Centres where a 3 times multiplier is suggested. At UWA: Full costs ...

Steps in cost analysis

... capacity of facility), and economies of scope (cost savings from the use of one facility for a greater diversity of services). What would happen to costs if the activities or programmes were scaled up or down, or piggy-backed with other services? Some care must be taken in this analysis, as changes ...

... capacity of facility), and economies of scope (cost savings from the use of one facility for a greater diversity of services). What would happen to costs if the activities or programmes were scaled up or down, or piggy-backed with other services? Some care must be taken in this analysis, as changes ...

Chapter 3.44 - Charges Reasonably Necessary

... and his or her custodians or records and/or designees to charge parties requesting public records a sum reasonably necessary to recover such additional costs of furnishing copies as permitted by law. Such additional costs shall not exceed the weighted hourly salary of the custodian or his designee ...

... and his or her custodians or records and/or designees to charge parties requesting public records a sum reasonably necessary to recover such additional costs of furnishing copies as permitted by law. Such additional costs shall not exceed the weighted hourly salary of the custodian or his designee ...

Logistics Network Configuration

... Data for Network Design 1. A listing of all products 2. Location of customers, stocking points and sources 3. Demand for each product by customer location 4. Transportation rates 5. Warehousing costs 6. Shipment sizes by product 7. Order patterns by frequency, size, season, content 8. Order process ...

... Data for Network Design 1. A listing of all products 2. Location of customers, stocking points and sources 3. Demand for each product by customer location 4. Transportation rates 5. Warehousing costs 6. Shipment sizes by product 7. Order patterns by frequency, size, season, content 8. Order process ...

Service Center Policy

... central administrative costs. (The Federal government has designated certain services as Service Centers, even though they may fall below the University expenditure threshold, e.g., animal care facilities.) Separate organization(s) must be established for each service center to account for its opera ...

... central administrative costs. (The Federal government has designated certain services as Service Centers, even though they may fall below the University expenditure threshold, e.g., animal care facilities.) Separate organization(s) must be established for each service center to account for its opera ...

Revision Notes

... There are a number of costs; sunk costs; committed costs; notional costs, that are termed irrelevant to decision-making because they are either not future cash flows or costs which will be incurred anyway, regardless of the decision that is taken. A sunk cost is a cost which has already been incurre ...

... There are a number of costs; sunk costs; committed costs; notional costs, that are termed irrelevant to decision-making because they are either not future cash flows or costs which will be incurred anyway, regardless of the decision that is taken. A sunk cost is a cost which has already been incurre ...

class group cases – acct 2302

... Sales are 20% cash and 80% on credit. All credit sales are collected in the month following the sale. The June 30 balance sheet includes balances of $12,900 in cash; $47,000 in accounts receivable; $5,100 in accounts payable; and a $2,600 balance in loans payable. A minimum cash balance of $12,600 i ...

... Sales are 20% cash and 80% on credit. All credit sales are collected in the month following the sale. The June 30 balance sheet includes balances of $12,900 in cash; $47,000 in accounts receivable; $5,100 in accounts payable; and a $2,600 balance in loans payable. A minimum cash balance of $12,600 i ...

Financial Liabilities Measured at Fair Value through Profit or Loss

... Paragraph 18 of IAS 23 Borrowing Costs requires capitalization of borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset. Borrowing costs are defined, in part, as interest expense calculated using the effective interest rate method as desc ...

... Paragraph 18 of IAS 23 Borrowing Costs requires capitalization of borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset. Borrowing costs are defined, in part, as interest expense calculated using the effective interest rate method as desc ...

Manufacturing Accounting Intro

... Direct materials + direct labour + manufacturing overhead are considered to be product costs because they are all associated with the manufacture of a product. Direct labour + manufacturing overhead is commonly called the conversion cost because these are the costs associated with converting the dir ...

... Direct materials + direct labour + manufacturing overhead are considered to be product costs because they are all associated with the manufacture of a product. Direct labour + manufacturing overhead is commonly called the conversion cost because these are the costs associated with converting the dir ...

Activity Based Costing

... ABC is a management tool that provides better allocation of resources. The ABC or unit cost goal is a benchmark that represents an expectation of the cost incurred for the production of an output. ABC aligns costs to outputs thereby increasing cost visibility, and is useful in forecasting financial ...

... ABC is a management tool that provides better allocation of resources. The ABC or unit cost goal is a benchmark that represents an expectation of the cost incurred for the production of an output. ABC aligns costs to outputs thereby increasing cost visibility, and is useful in forecasting financial ...

Download File

... UPS/USPS-T30-5. Refer to your response to interrogatory DFC/USPS-T30-1. Confirm that in GFY 2000, 21.7% of all flat rate Priority Mail envelopes weighed more than 1 pound. If not confirmed, provide the correct percentage. UPS/USPS-T30-6. How many pieces in the flat rate envelope category does the Po ...

... UPS/USPS-T30-5. Refer to your response to interrogatory DFC/USPS-T30-1. Confirm that in GFY 2000, 21.7% of all flat rate Priority Mail envelopes weighed more than 1 pound. If not confirmed, provide the correct percentage. UPS/USPS-T30-6. How many pieces in the flat rate envelope category does the Po ...

Flexible Budgets ACC/543 Budgeting is a key concept in business

... costs. Closely related to fixed and variable costs is the concept of cost structure. For most businesses, the application of the appropriate cost structure depends on the expected or generated revenue. Businesses can either apply a fixed or variable cost structure. A fixed cost structure focuses on ...

... costs. Closely related to fixed and variable costs is the concept of cost structure. For most businesses, the application of the appropriate cost structure depends on the expected or generated revenue. Businesses can either apply a fixed or variable cost structure. A fixed cost structure focuses on ...

What is a Cost? - University of North Florida

... • Dedicated cost accountant labor • Factory and equipment depreciation • Factory insurance • Factory rent and utilities • Other factory costs ...

... • Dedicated cost accountant labor • Factory and equipment depreciation • Factory insurance • Factory rent and utilities • Other factory costs ...

Costs of Production Practice

... (A) Average total costs are increasing when marginal costs are increasing. (B) Marginal costs are increasing when average variable costs are higher than marginal costs. (C) Average variable costs are increasing when marginal costs are increasing. (D) Average variable costs are increasing when margin ...

... (A) Average total costs are increasing when marginal costs are increasing. (B) Marginal costs are increasing when average variable costs are higher than marginal costs. (C) Average variable costs are increasing when marginal costs are increasing. (D) Average variable costs are increasing when margin ...

Managing Risks in the Project Pipeline Minimizing the Impacts Larry Redd, P.E.

... – Using (accurate) forward projections of available revenue, or reducing design times in the pipeline (especially for 3R4R projects) – Reducing the values of the factors of Hurry Up and Holding Costs – The “Critical Project Method” of stabilizing the flow of major projects has proven effective. Don’ ...

... – Using (accurate) forward projections of available revenue, or reducing design times in the pipeline (especially for 3R4R projects) – Reducing the values of the factors of Hurry Up and Holding Costs – The “Critical Project Method” of stabilizing the flow of major projects has proven effective. Don’ ...

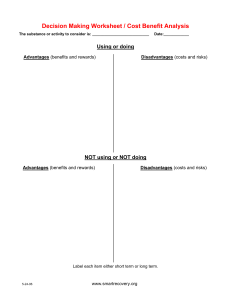

Decision Making

... marginal costing may be used to assist in shutdown or continuation decisions a shut-down decision that is based on absorption costing may not be a good decision if a contribution is being made towards covering fixed costs ...

... marginal costing may be used to assist in shutdown or continuation decisions a shut-down decision that is based on absorption costing may not be a good decision if a contribution is being made towards covering fixed costs ...

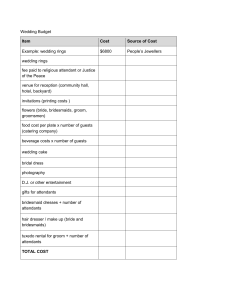

Wedding Budget Item Cost Source of Cost Example: wedding rings

... Instructions: In a paragraph of 200 words, describe your reaction to the costs of the items. Were you surprised, for example, by the costs? Did the costs of the items cause you to reconsider the number of guests you would invite? Did the costs cause you to change the inclusion of some budget items? ...

... Instructions: In a paragraph of 200 words, describe your reaction to the costs of the items. Were you surprised, for example, by the costs? Did the costs of the items cause you to reconsider the number of guests you would invite? Did the costs cause you to change the inclusion of some budget items? ...