BASIC CONCEPTS OF FINANCIAL ACCOUNTING

... • Liabilities are present obligations of the firm. – They are probable future sacrifices of economic benefits which arise as the result of past transactions or events. ...

... • Liabilities are present obligations of the firm. – They are probable future sacrifices of economic benefits which arise as the result of past transactions or events. ...

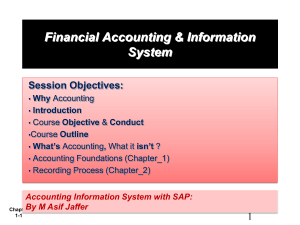

What is Accounting? - masif-emba-fais-s12

... Cost Principle (Historical) – dictates that companies record assets at their cost. Issues: Reported at cost when purchased and also over the time the asset is held. Cost easily verified, whereas market value is often subjective. ...

... Cost Principle (Historical) – dictates that companies record assets at their cost. Issues: Reported at cost when purchased and also over the time the asset is held. Cost easily verified, whereas market value is often subjective. ...

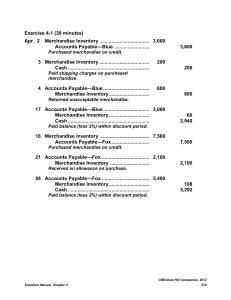

Exercise 4-1 (30 minutes) Apr. 2 Merchandise Inventory 3,600

... future. For example, the returns might arise from product defects, shipping damage, misleading information provided at the time of sale, or fickle customers. An important early step in controlling returns is to have information about their dollar amount. In addition, managers can set goals for reduc ...

... future. For example, the returns might arise from product defects, shipping damage, misleading information provided at the time of sale, or fickle customers. An important early step in controlling returns is to have information about their dollar amount. In addition, managers can set goals for reduc ...

2012 Audited Financial Statements

... Accounts receivable --- Accounts receivable are stated at the amounts management expects to collect from outstanding balances. Management provides for probable uncollectible amounts through a charge to expense and a credit to a valuation allowable based on its assessment of the current status of ind ...

... Accounts receivable --- Accounts receivable are stated at the amounts management expects to collect from outstanding balances. Management provides for probable uncollectible amounts through a charge to expense and a credit to a valuation allowable based on its assessment of the current status of ind ...

Understanding Our Environment

... Von Liebig proposed the single factor in shortest supply relative to demand is the critical determinant in species distribution. Shelford later expanded by stating each environmental factor has both minimum and maximum levels, tolerance limits, beyond which a particular species cannot survive. ...

... Von Liebig proposed the single factor in shortest supply relative to demand is the critical determinant in species distribution. Shelford later expanded by stating each environmental factor has both minimum and maximum levels, tolerance limits, beyond which a particular species cannot survive. ...

PDF

... flowing (chrematistic) in societies it is actually a poor “economic” measure. The word “economic” comes from the Greek oikonomia, meaning the stewardship or management of the household; the word “wealth” comes from the Old English meaning the condition (th) of well-being (weal).” If we are to measur ...

... flowing (chrematistic) in societies it is actually a poor “economic” measure. The word “economic” comes from the Greek oikonomia, meaning the stewardship or management of the household; the word “wealth” comes from the Old English meaning the condition (th) of well-being (weal).” If we are to measur ...

Principles of Accounting I

... Regulation Business Environment and Concepts Since many people rely on accounting information it is important that accountants maintain the highest ethical standards. As we discuss various topics we will consider the ethical aspect of the actions we take. ...

... Regulation Business Environment and Concepts Since many people rely on accounting information it is important that accountants maintain the highest ethical standards. As we discuss various topics we will consider the ethical aspect of the actions we take. ...

Academic Advisors Environmental and Sustainability Sciences (ESS

... HADM 4415: Sustainable Business and Economics with ...

... HADM 4415: Sustainable Business and Economics with ...

Nature-based Solutions: New Influence for

... biodiversity within these areas while exporting biomass into fishing grounds (Grorud-Colvert et al. 2014). This type of NBS is connected to, e. g., the concept of biosphere reserves incorporating core protected areas for nature conservation and buffer and transition areas where people live and work ...

... biodiversity within these areas while exporting biomass into fishing grounds (Grorud-Colvert et al. 2014). This type of NBS is connected to, e. g., the concept of biosphere reserves incorporating core protected areas for nature conservation and buffer and transition areas where people live and work ...

رقم الطالب في كشف الحضور:....... دراسات محاسبية باللغة الإنجليزية عدد

... 5. Goods out on consignment should be included in the inventory of the consignor. 6. The specific identification method of costing inventories tracks the actual physical flow of the goods available for sale. 7. Management may choose any inventory costing method it desires as long as the cost flow as ...

... 5. Goods out on consignment should be included in the inventory of the consignor. 6. The specific identification method of costing inventories tracks the actual physical flow of the goods available for sale. 7. Management may choose any inventory costing method it desires as long as the cost flow as ...

1. Paid rent for the next three months. 2. Paid property taxes that

... A. Accounts receivable to retained earnings when an account is fully paid. B. Balances in temporary accounts to a permanent account. C. Inventory to cost of goods sold when merchandise is sold. D. Assets and liabilities when operations are discontinued. 62. Temporary accounts would not include: ...

... A. Accounts receivable to retained earnings when an account is fully paid. B. Balances in temporary accounts to a permanent account. C. Inventory to cost of goods sold when merchandise is sold. D. Assets and liabilities when operations are discontinued. 62. Temporary accounts would not include: ...

chap.3 - HCC Learning Web

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

BRIEF EXERCISE 8-1 (a) Other receivables. (b) Notes receivable. (c

... Frequently the allowance is estimated as a percentage of the outstanding receivables. Management establishes a percentage relationship between the amount of receivables and expected losses from uncollectible accounts. Companies often prepare a schedule in which customer balances are classified ...

... Frequently the allowance is estimated as a percentage of the outstanding receivables. Management establishes a percentage relationship between the amount of receivables and expected losses from uncollectible accounts. Companies often prepare a schedule in which customer balances are classified ...

Asset section of the balance sheet

... during the period of time. Expenses reports in one accounting period may actually be paid for in another accounting period. o Net income (or net earnings): the excess of total revenues over total expenses. If total expenses exceed total revenues, a net loss is reported. Net income normally does not ...

... during the period of time. Expenses reports in one accounting period may actually be paid for in another accounting period. o Net income (or net earnings): the excess of total revenues over total expenses. If total expenses exceed total revenues, a net loss is reported. Net income normally does not ...

Taylor Shellfish ECOP - Case Inlet Shoreline Association

... Introduction. Clam and oyster culture on Taylor Resources’ tidelands requires seed of larger sizes than is generally economical to grow in an upland nursery. In upland nurseries algae must be cultured to feed young shellfish and large amounts of water need to be pumped upland for optimal flows. In o ...

... Introduction. Clam and oyster culture on Taylor Resources’ tidelands requires seed of larger sizes than is generally economical to grow in an upland nursery. In upland nurseries algae must be cultured to feed young shellfish and large amounts of water need to be pumped upland for optimal flows. In o ...

download

... For each of the following errors, considered individually, indicate whether the error would cause the adjusted trial balance totals to be unequal. If the error would cause the adjusted trial balance total to be unequal, indicate whether the debit or credit total is higher and by how much. a. The adj ...

... For each of the following errors, considered individually, indicate whether the error would cause the adjusted trial balance totals to be unequal. If the error would cause the adjusted trial balance total to be unequal, indicate whether the debit or credit total is higher and by how much. a. The adj ...

Sample Study Guide - McGraw Hill Higher Education

... Analyze business transactions using the accounting equation. Summary A transaction is an exchange of economic consideration between two parties. Examples include products, services, money and rights to collect money. Transactions always have at least two effects on one or more components of the acco ...

... Analyze business transactions using the accounting equation. Summary A transaction is an exchange of economic consideration between two parties. Examples include products, services, money and rights to collect money. Transactions always have at least two effects on one or more components of the acco ...

LO 5 - Test Banks Shop

... rely on the financial statements to make important decisions Accountants must make subjective judgments about what information to present and how to present it- this is why accounting is a profession. The Changing Face of the Accounting Profession Examples of some the companies involved in financi ...

... rely on the financial statements to make important decisions Accountants must make subjective judgments about what information to present and how to present it- this is why accounting is a profession. The Changing Face of the Accounting Profession Examples of some the companies involved in financi ...

Certified Hospitality Accountant Executive (CHAE) Review

... What Funds Were Raised by the Sale of Capital Stock What Amount of Dividends Were Paid How Much Was Invested in Long Term Investments The Statement of Cash Flows Required Statement Since 1988 by the FASB Replaces the Statement of Changes in Financial Position ...

... What Funds Were Raised by the Sale of Capital Stock What Amount of Dividends Were Paid How Much Was Invested in Long Term Investments The Statement of Cash Flows Required Statement Since 1988 by the FASB Replaces the Statement of Changes in Financial Position ...

THE UTAH GENUINE PROGRESS INDICATOR (GPI) 1990-2007

... the earth to be concerned about the environment, sustainability, and population. Furthermore, we place special value on the unique heritage and landscape of the state of Utah. ...

... the earth to be concerned about the environment, sustainability, and population. Furthermore, we place special value on the unique heritage and landscape of the state of Utah. ...

preference shares - LPS Business Department

... The main disadvantages of being a sole trader are: • That liability is not limited to the amount of money invested by the owner. This means that if the business fails and creditors cannot be paid from the proceeds raised from the sale of business assets then the proprietor must provide further finan ...

... The main disadvantages of being a sole trader are: • That liability is not limited to the amount of money invested by the owner. This means that if the business fails and creditors cannot be paid from the proceeds raised from the sale of business assets then the proprietor must provide further finan ...

Review of a Company`s Accounting System

... the financial statements, to (a) reduce the balances in all temporary accounts (revenue, expense, and dividend accounts) to zero, and (b) update the retained earnings and inventory accounts. Each temporary income statement account is closed, that is, debited or credited for the amount that will resu ...

... the financial statements, to (a) reduce the balances in all temporary accounts (revenue, expense, and dividend accounts) to zero, and (b) update the retained earnings and inventory accounts. Each temporary income statement account is closed, that is, debited or credited for the amount that will resu ...

Debits and Credits: Analyzing and Recording Business Transactions

... of accounts will give us the same answers as in Chapter 1, but with greater ease. Mia’s accountant developed what is called a chart of accounts. The chart of accounts is a numbered list of all of the business’s accounts. It allows accounts to be located quickly. In Mia’s business, for example, 100s ...

... of accounts will give us the same answers as in Chapter 1, but with greater ease. Mia’s accountant developed what is called a chart of accounts. The chart of accounts is a numbered list of all of the business’s accounts. It allows accounts to be located quickly. In Mia’s business, for example, 100s ...

practiceqs_chapter3

... a. adjust the accounts to their proper amounts on December 31. b. understate total assets on the balance sheet as of December 31. c. overstate the net book value of the capital assets at December 31. d. understate the net book value of the capital assets as of December 31. ...

... a. adjust the accounts to their proper amounts on December 31. b. understate total assets on the balance sheet as of December 31. c. overstate the net book value of the capital assets at December 31. d. understate the net book value of the capital assets as of December 31. ...