Student lecture notes - Pearson Higher Education

... It may not always be feasible to split costs neatly into variable and fixed categories. Some costs show …………………. behaviour. ...

... It may not always be feasible to split costs neatly into variable and fixed categories. Some costs show …………………. behaviour. ...

III Local audit of project accounts

... The accounts must be audited annually or periodically by the auditor mandated with the consent of the SIB. The auditor shall verify in particular the existence and the quality of the ICS as well as the proper rendering of accounts, and confirm conformity with the project aims and the cost-effectiven ...

... The accounts must be audited annually or periodically by the auditor mandated with the consent of the SIB. The auditor shall verify in particular the existence and the quality of the ICS as well as the proper rendering of accounts, and confirm conformity with the project aims and the cost-effectiven ...

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Ordinary Level 7110/13

... standing order for payment of insurance premium ...

... standing order for payment of insurance premium ...

PART A - Chabot College

... Analyze each transaction. Use T accounts to record these transactions. Transactions are unrelated to each other!!!! Be sure to put the name of account on the top of each account. Label each T account with debit/credit and plus/minus signs (2 pts each transaction): ...

... Analyze each transaction. Use T accounts to record these transactions. Transactions are unrelated to each other!!!! Be sure to put the name of account on the top of each account. Label each T account with debit/credit and plus/minus signs (2 pts each transaction): ...

Appendix B - College of the Redwoods

... Book value. Value as shown in the “book” of accounts. In the case of assets subject to reduction by valuation allowances, “book value” refers to cost or stated value less any appropriate allowance. A distinction is sometimes made between “gross book value” and “net book value,” the former designatin ...

... Book value. Value as shown in the “book” of accounts. In the case of assets subject to reduction by valuation allowances, “book value” refers to cost or stated value less any appropriate allowance. A distinction is sometimes made between “gross book value” and “net book value,” the former designatin ...

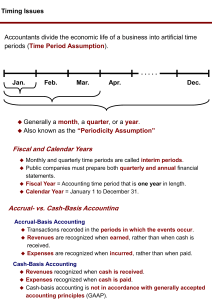

Fiscal and Calendar Years Accrual- vs. Cash

... Expenses are recognized when incurred, rather than when paid. Cash-Basis Accounting Revenues recognized when cash is received. Expenses recognized when cash is paid. Cash-basis accounting is not in accordance with generally accepted ...

... Expenses are recognized when incurred, rather than when paid. Cash-Basis Accounting Revenues recognized when cash is received. Expenses recognized when cash is paid. Cash-basis accounting is not in accordance with generally accepted ...

Chapter 6: Highlights

... Under the accrual basis of measuring income, firms recognize revenue when (a) all, or a substantial portion, of the services expected to be provided have been performed, and (b) cash, or another asset whose cash equivalent value a firm can measure objectively, has been received. Satisfying the first ...

... Under the accrual basis of measuring income, firms recognize revenue when (a) all, or a substantial portion, of the services expected to be provided have been performed, and (b) cash, or another asset whose cash equivalent value a firm can measure objectively, has been received. Satisfying the first ...

Is the accounting equation in balance?

... toward convergence of accounting standards. Objective of Financial Reporting: To provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in making decisions in their capacity as capital providers. ...

... toward convergence of accounting standards. Objective of Financial Reporting: To provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in making decisions in their capacity as capital providers. ...

PSA 510: Initial Engagements * Opening Balances

... asset and accumulated depreciation are restated proportionately to the revalued amount. After the revaluation entry, the excess of the asset balance over the balance of the accumulated depreciation is equal to the revalued amount. Under the elimination method, the balance of the accumulated deprecia ...

... asset and accumulated depreciation are restated proportionately to the revalued amount. After the revaluation entry, the excess of the asset balance over the balance of the accumulated depreciation is equal to the revalued amount. Under the elimination method, the balance of the accumulated deprecia ...

LO 5 - Test Banks Shop

... rely on the financial statements to make important decisions Accountants must make subjective judgments about what information to present and how to present it- this is why accounting is a profession. The Changing Face of the Accounting Profession Examples of some the companies involved in financi ...

... rely on the financial statements to make important decisions Accountants must make subjective judgments about what information to present and how to present it- this is why accounting is a profession. The Changing Face of the Accounting Profession Examples of some the companies involved in financi ...

Chapter 7 - Business Accounting

... Chapter 7 – Business Accounting Syllabus Unit – Business Finance and Accounting ...

... Chapter 7 – Business Accounting Syllabus Unit – Business Finance and Accounting ...

1. Explicit costs a. require an outlay of money by the firm. b. include

... a. increasing returns to scale. b. decreasing returns to scale. c. diminishing total product. d. diminishing marginal product. 15. Fixed costs can be defined as costs that a. vary inversely with production. b. vary in proportion with production. c. are incurred only when production is large enough. ...

... a. increasing returns to scale. b. decreasing returns to scale. c. diminishing total product. d. diminishing marginal product. 15. Fixed costs can be defined as costs that a. vary inversely with production. b. vary in proportion with production. c. are incurred only when production is large enough. ...

Chap009

... – Potential obsolescence – Goods have not been sold, so marketability may be uncertain. ...

... – Potential obsolescence – Goods have not been sold, so marketability may be uncertain. ...

Tutorial - Cengage

... 17. The downward-sloping segment of the longrun average cost curve corresponds to a. diseconomies of scale. b. both economies and diseconomies of scale. c. the decrease in average variable cost. d. economies of scale. D. Economies of scale takes place when a firm increases its efficiency by produci ...

... 17. The downward-sloping segment of the longrun average cost curve corresponds to a. diseconomies of scale. b. both economies and diseconomies of scale. c. the decrease in average variable cost. d. economies of scale. D. Economies of scale takes place when a firm increases its efficiency by produci ...

Chapter 11

... concern that any new equipment acquired to replace the old equipment may become obsolete within the next two to five years. A number of popular-press articles have recently discussed the increasing number of asset impairments occurring in their industry. Conner and Martin therefore want to know how ...

... concern that any new equipment acquired to replace the old equipment may become obsolete within the next two to five years. A number of popular-press articles have recently discussed the increasing number of asset impairments occurring in their industry. Conner and Martin therefore want to know how ...

Internal Controls - Trans

... Utilization Reports (such as payroll and related employee benefit cost reports or similar usage reports) ...

... Utilization Reports (such as payroll and related employee benefit cost reports or similar usage reports) ...

PowerPoint

... • Grants should be closed before a final invoice and/or financial report (ROE, FFR) can be prepared – Charges must be posted to grant including: ...

... • Grants should be closed before a final invoice and/or financial report (ROE, FFR) can be prepared – Charges must be posted to grant including: ...

question bank - SIETK ECE Dept

... 37. Which of the following do not involve payment of cash as they are not actually incurred? (A) Explicit costs ...

... 37. Which of the following do not involve payment of cash as they are not actually incurred? (A) Explicit costs ...

Villegas y Villegas Mexico Joins Alliott Group Press Release

... Villegas y Villegas is an accounting firm founded by Guillermo Villegas in 1982. The firm is located in one of Mexico's main industrial cities, and their clients have been expanding rapidly reflecting the scope of services offered by Villegas y Villegas Currently the focus of Villegas y Villegas mai ...

... Villegas y Villegas is an accounting firm founded by Guillermo Villegas in 1982. The firm is located in one of Mexico's main industrial cities, and their clients have been expanding rapidly reflecting the scope of services offered by Villegas y Villegas Currently the focus of Villegas y Villegas mai ...

Chapter 5 The Time Value of Money

... of millions of dollars in taxes by its use of stock options. Corporate executives received large quantities of stock options. When they exercised these options, the company claimed compensation expense on their tax returns. Accounting rules let them omit that same expense from the earnings statement ...

... of millions of dollars in taxes by its use of stock options. Corporate executives received large quantities of stock options. When they exercised these options, the company claimed compensation expense on their tax returns. Accounting rules let them omit that same expense from the earnings statement ...

Weygandt_FinMan_PowerPoint_Review_Ch15

... Determining the Cost of Goods Manufactured Total Work in Process – (1) cost of beginning work in process and (2) total manufacturing costs for the current period. Total Manufacturing Costs – sum of direct material costs, direct labor costs, and manufacturing overhead in the current year. Illustratio ...

... Determining the Cost of Goods Manufactured Total Work in Process – (1) cost of beginning work in process and (2) total manufacturing costs for the current period. Total Manufacturing Costs – sum of direct material costs, direct labor costs, and manufacturing overhead in the current year. Illustratio ...

Case Development (Action) Slides

... Chart of Accounts • Assign appropriate account numbers to each identified account – Assets (100), Liabilities (200), Owners Equity ...

... Chart of Accounts • Assign appropriate account numbers to each identified account – Assets (100), Liabilities (200), Owners Equity ...

Understanding Financ.. - Loughborough University

... The Reducing Balance Method: takes the original cost of the asset and reduces it by a fixed % each year This method is used where the asset is expected to depreciate more heavily in the earlier years of its use. Activity: (complete the table below) A new vehicle costs £12,000 It is decided that it w ...

... The Reducing Balance Method: takes the original cost of the asset and reduces it by a fixed % each year This method is used where the asset is expected to depreciate more heavily in the earlier years of its use. Activity: (complete the table below) A new vehicle costs £12,000 It is decided that it w ...

REVIEW OF ILLUSTRATIVE FINANCIAL STATEMENTS IN

... straight line basis over the respective lease term Dividend income from investments, including associates is recognized in the period in which the right to receive payment has been established. ...

... straight line basis over the respective lease term Dividend income from investments, including associates is recognized in the period in which the right to receive payment has been established. ...

Edward P. Moxey

Edward Preston Moxey, Jr. (Oct. 2, 1881 - April 6, 1943 ) was an American accountant, and the first Professor of Accounting at the Wharton School of Finance and Commerce at the University of Pennsylvania. He is known for his early works on cost keeping in factories, which describe the elementary principles of cost accounting.