The Evolution of the Financial Intermediary Controls and

... The scope of an auditor’s examination within a FICCA engagement is intended to be flexible for the intermediary completing the engagement. The specific details of the engagement are agreed upon by the auditor and the intermediary. For example, if an omnibus firm has previously engaged an auditor to ...

... The scope of an auditor’s examination within a FICCA engagement is intended to be flexible for the intermediary completing the engagement. The specific details of the engagement are agreed upon by the auditor and the intermediary. For example, if an omnibus firm has previously engaged an auditor to ...

Disclosure Timing and the Market Response to First

... disclosed following GCMs. Taken together, these studies suggest that going concern reporting provides important information to investors. As discussed above, however, there are several reasons why GCMs may not provide investors with incremental information. First, prior research finds that a conside ...

... disclosed following GCMs. Taken together, these studies suggest that going concern reporting provides important information to investors. As discussed above, however, there are several reasons why GCMs may not provide investors with incremental information. First, prior research finds that a conside ...

1. Which of the following statements best describes the IFRS

... costs. D. it makes it harder to measure transactions. ...

... costs. D. it makes it harder to measure transactions. ...

questions on non-gaap measures

... misunderstanding about the level of auditor involvement with non-GAAP measures. It was noted that in certain situations, at the direction of the audit committee or management, auditors may perform additional procedures over these measures. ...

... misunderstanding about the level of auditor involvement with non-GAAP measures. It was noted that in certain situations, at the direction of the audit committee or management, auditors may perform additional procedures over these measures. ...

GAAP

... accountants, auditors, boards of directors, stockholders, and potential business partners, can differ, especially when competing interests are involved. Financial statement items are considered material (large enough to matter) if they could influence the economic decisions of users. The materiality ...

... accountants, auditors, boards of directors, stockholders, and potential business partners, can differ, especially when competing interests are involved. Financial statement items are considered material (large enough to matter) if they could influence the economic decisions of users. The materiality ...

English - EDUCatt

... This book has evolved from the English courses held within a Master’s Course in Governance, Sistema di Controllo and Auditing at the Catholic University in Milan, organized in collaboration with ENI. It aims to enable non-native speakers of English to use English successfully in the auditing profess ...

... This book has evolved from the English courses held within a Master’s Course in Governance, Sistema di Controllo and Auditing at the Catholic University in Milan, organized in collaboration with ENI. It aims to enable non-native speakers of English to use English successfully in the auditing profess ...

Research exercise on charities SORP (FRS 102)

... charity. More guidance is needed to help preparers to tell their story, perhaps by providing them with guidance notes, prompts and best practice examples. Detail of reporting – given that there is plenty of detail which is required as part of the Trustees’ Annual Report, a key area of concern is ...

... charity. More guidance is needed to help preparers to tell their story, perhaps by providing them with guidance notes, prompts and best practice examples. Detail of reporting – given that there is plenty of detail which is required as part of the Trustees’ Annual Report, a key area of concern is ...

Does the Big-4 Effect Exist when Reputation and

... Big-4 firms have low and similar litigation and reputation risks. Our tests therefore aim to capture the potential quality effects of Big-4 firms being more competent and independent. In other words, we assume that Big-4 firms have the potential to deliver higher audit quality than non-Big-4 firms, ...

... Big-4 firms have low and similar litigation and reputation risks. Our tests therefore aim to capture the potential quality effects of Big-4 firms being more competent and independent. In other words, we assume that Big-4 firms have the potential to deliver higher audit quality than non-Big-4 firms, ...

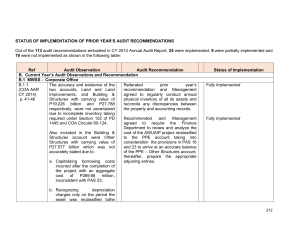

MWSS2015_Part3-Status_of_PY`s_Recomm

... in the amount of P464.434 million was not accurately reported due to (a) Income pertaining to CY 2013 with an aggregate total of P229.229 million was recognized as revenue during the year and (b) income received in CY 2014 totaling P235.205 million was not recognized as current year’s income. Also, ...

... in the amount of P464.434 million was not accurately reported due to (a) Income pertaining to CY 2013 with an aggregate total of P229.229 million was recognized as revenue during the year and (b) income received in CY 2014 totaling P235.205 million was not recognized as current year’s income. Also, ...

(revised) compilation engagements

... a reported item in the financial information, and the amount, classification, presentation, or disclosure that is required for the item to be in accordance with the applicable financial reporting framework. Misstatements can arise from error or fraud. Where the financial information is prepared in a ...

... a reported item in the financial information, and the amount, classification, presentation, or disclosure that is required for the item to be in accordance with the applicable financial reporting framework. Misstatements can arise from error or fraud. Where the financial information is prepared in a ...

accounting - WordPress.com

... ACCOUNTING... The most commonly used accounting method, which reports income when earned and expenses when incurred, as opposed to cash basis accounting which reports income when received and expenses when paid. ...

... ACCOUNTING... The most commonly used accounting method, which reports income when earned and expenses when incurred, as opposed to cash basis accounting which reports income when received and expenses when paid. ...

Defence Audit Guidelines_Final 25 March 2010

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

... Pakistan for use in Field Audit Offices (FAOs) for conducting Certification and Compliance with Authority audits. The Manual is based on the INTOSAI Auditing Standards and the international best practices. It covers the entire Audit Cycle and provides guidance with regard to the methods and approach ...

In Re: Gravity Co., Ltd. Securities Litigation 05-CV

... 29. The Prospectus contained Gravity's audited consolidated balance sheets as o f December 31, 2002 and 2003 and its audited consolidated statements of operations, changes in shareholders' equity and cash flows for the years ended December 31, 2001, 2002 and 2003 . In addition, the Prospectus includ ...

... 29. The Prospectus contained Gravity's audited consolidated balance sheets as o f December 31, 2002 and 2003 and its audited consolidated statements of operations, changes in shareholders' equity and cash flows for the years ended December 31, 2001, 2002 and 2003 . In addition, the Prospectus includ ...

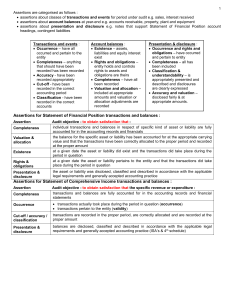

Aue2602 Summary

... recorded at correct amount (accuracy) and are allocated in proper accounting period (cut-off) have all been recorded (completeness) in the proper accounts (classification) Receipts (transactions) : payment from debtor actually occurred and pertains to entity (occurrence) receipts are recorde ...

... recorded at correct amount (accuracy) and are allocated in proper accounting period (cut-off) have all been recorded (completeness) in the proper accounts (classification) Receipts (transactions) : payment from debtor actually occurred and pertains to entity (occurrence) receipts are recorde ...

Advanced Oxygen Technologies 10K, June 30, 2012 - aoxy

... the statements are made. All statements, analyses and other information contained in this report relative to trends in sales, gross margin, anticipated expense levels and liquidity and capital resources, as well as other statements including, but not limited to, words such as "anticipate," "believe, ...

... the statements are made. All statements, analyses and other information contained in this report relative to trends in sales, gross margin, anticipated expense levels and liquidity and capital resources, as well as other statements including, but not limited to, words such as "anticipate," "believe, ...

The Auditor`s Responsibility to Detect Fraud

... inventory on the balance sheet to show more inventory on hand than is actually there, thus intentionally overstating assets and revenues. As a result of fraudulent activities occurring in Enron, WorldCom and other companies, the Sarbanes-Oxley Act of 2002 has required that internal controls be revie ...

... inventory on the balance sheet to show more inventory on hand than is actually there, thus intentionally overstating assets and revenues. As a result of fraudulent activities occurring in Enron, WorldCom and other companies, the Sarbanes-Oxley Act of 2002 has required that internal controls be revie ...

CHAPTER 1 – Principles of Accounting

... Accounting and Reporting Capabilities A governmental accounting system must make it possible both (a) to present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental unit in conformity with generally accepted a ...

... Accounting and Reporting Capabilities A governmental accounting system must make it possible both (a) to present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental unit in conformity with generally accepted a ...

old dominion freight line, inc.

... agreement dated August 10, 2006 (the “Credit Agreement”), with Wachovia Bank, National Association (“Wachovia”) serving as administrative agent for the lenders. Of the $225.0 million line of credit commitments, $150.0 million may be used for letters of credit and $15.0 million may be used for borrow ...

... agreement dated August 10, 2006 (the “Credit Agreement”), with Wachovia Bank, National Association (“Wachovia”) serving as administrative agent for the lenders. Of the $225.0 million line of credit commitments, $150.0 million may be used for letters of credit and $15.0 million may be used for borrow ...

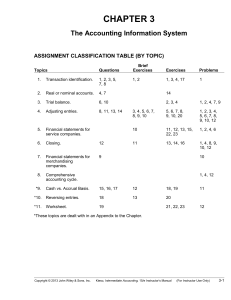

chap.3 - HCC Learning Web

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

... Depending on time constraints and students’ accounting course background, Chapter 3 can be approached in several different ways: (1) Spend 2-3 class sessions reviewing the chapter and Appendices 3-A through 3-C. (2) Spend 1-2 class sessions reviewing selected portions of the chapter and Appendix 3-A ...

Guide to New Canadian Independence Standard

... assurance engagement. Circumstances that may create a self-review threat include there being a person on the engagement team being, or having recently been, an employee of the assurance client in a position to exert direct and significant influence over the subject matter of the engagement. An Advoc ...

... assurance engagement. Circumstances that may create a self-review threat include there being a person on the engagement team being, or having recently been, an employee of the assurance client in a position to exert direct and significant influence over the subject matter of the engagement. An Advoc ...

- Charities SORP

... We seek to combine amateur community events, including our annual event BF Borough Scouts and Guides Christmas Concert and the BF Borough Amateur Dramatics Society Comedy Summer Season alongside professional events including classic plays such as Twelfth Night and dramatic modern performances such a ...

... We seek to combine amateur community events, including our annual event BF Borough Scouts and Guides Christmas Concert and the BF Borough Amateur Dramatics Society Comedy Summer Season alongside professional events including classic plays such as Twelfth Night and dramatic modern performances such a ...

PDF - The Actuarial Standards Board

... the American Academy of Actuaries (Academy) Committee on Life Insurance Financial Reporting for the Life Committee of the ASB. In 1992, ASOP No. 10 was expanded. The purpose of the expansion was to incorporate portions of the Academy’s Financial Reporting Recommendation (FRR) 1, Actuarial Methods an ...

... the American Academy of Actuaries (Academy) Committee on Life Insurance Financial Reporting for the Life Committee of the ASB. In 1992, ASOP No. 10 was expanded. The purpose of the expansion was to incorporate portions of the Academy’s Financial Reporting Recommendation (FRR) 1, Actuarial Methods an ...

Document

... transparent. The emphasis of the V in red re-emphasize those values as it stands out among others in the industry. The italic nature of the “VOTY” gives out a brand message of “leaning forward”, encompassing the very value of the branding qualities of the event and publication recognisable among its ...

... transparent. The emphasis of the V in red re-emphasize those values as it stands out among others in the industry. The italic nature of the “VOTY” gives out a brand message of “leaning forward”, encompassing the very value of the branding qualities of the event and publication recognisable among its ...

JD Group covers 27606

... in which we trade forced this upon us. What held good for the past is most certainly not so for the future. Those companies who fail to acknowledge this reality will hit a brick wall; some already have. We are obviously disappointed that we deliberately had to interrupt our strong growth track recor ...

... in which we trade forced this upon us. What held good for the past is most certainly not so for the future. Those companies who fail to acknowledge this reality will hit a brick wall; some already have. We are obviously disappointed that we deliberately had to interrupt our strong growth track recor ...