10414-378 IFRS IT White Paper WEB FINAL

... In the AICPA IFRS Preparedness Survey conducted in September 2009, a 54% majority of CPAs believed that the SEC should ultimately require adoption of IFRS for U.S. public companies. Furthermore, more than 50% of respondents expressed a need to know some level of IFRS over the next three years. Howev ...

... In the AICPA IFRS Preparedness Survey conducted in September 2009, a 54% majority of CPAs believed that the SEC should ultimately require adoption of IFRS for U.S. public companies. Furthermore, more than 50% of respondents expressed a need to know some level of IFRS over the next three years. Howev ...

Appendix

... made for a stated period of time during which the funds may be spent; (c) The grant instrument names the Principal Investigator or Project Director under whose direction the project will be carried out; and (d) The grant carries a minimum number of limiting conditions that are stated in the award do ...

... made for a stated period of time during which the funds may be spent; (c) The grant instrument names the Principal Investigator or Project Director under whose direction the project will be carried out; and (d) The grant carries a minimum number of limiting conditions that are stated in the award do ...

Comprehensive Case A.1 – Enron

... reliability of various kinds of evidence are subject to important exceptions.” So, the competence of audit evidence refers to the quality of the evidence gathered for a financial statement assertion about a financial statement account balance and/or an economic transaction(s). And, as indicated in ...

... reliability of various kinds of evidence are subject to important exceptions.” So, the competence of audit evidence refers to the quality of the evidence gathered for a financial statement assertion about a financial statement account balance and/or an economic transaction(s). And, as indicated in ...

Management control systems. Literature

... in the right way to design or use management accounting systems (PUXTY, 1993). Within this paradigm the radical critiques emerged. The radical critique suggests that the discipline of MCS can also be regarded as a discursive practice following Foucault (1980). As a discursive formation, it views the ...

... in the right way to design or use management accounting systems (PUXTY, 1993). Within this paradigm the radical critiques emerged. The radical critique suggests that the discipline of MCS can also be regarded as a discursive practice following Foucault (1980). As a discursive formation, it views the ...

Implementation Tool for Auditors

... To the extent not already done so, obtain an understanding of the entity’s related controls, including control activities, relevant to the identified risk. Once the auditor has concluded that ROMM due to fraud in revenue recognition exists for all or only certain types of revenue and revenue transac ...

... To the extent not already done so, obtain an understanding of the entity’s related controls, including control activities, relevant to the identified risk. Once the auditor has concluded that ROMM due to fraud in revenue recognition exists for all or only certain types of revenue and revenue transac ...

Other cultures, other accountings

... -3whether there is a cohesive notion of, for example, Islamic warfare that is substantially distinctive from Western warfare. This scepticism needs to be addressed in any discussion of Islamic accounting – is the term actually helpful in the sense that it describes, or potentially could describe, a ...

... -3whether there is a cohesive notion of, for example, Islamic warfare that is substantially distinctive from Western warfare. This scepticism needs to be addressed in any discussion of Islamic accounting – is the term actually helpful in the sense that it describes, or potentially could describe, a ...

internal-auditing-instructional-material

... g. A description of noteworthy accomplishment, particularly when management improvement in one area may be applicable elsewhere h. A listing of any issues and questions needing further study and considerations i. A statement as to whether any pertinent information has been omitted because it is deem ...

... g. A description of noteworthy accomplishment, particularly when management improvement in one area may be applicable elsewhere h. A listing of any issues and questions needing further study and considerations i. A statement as to whether any pertinent information has been omitted because it is deem ...

Approved form - Australian Prudential Regulation Authority

... (collectively known as the ‘relevant forms’) of …………………………….. [insert name of the superannuation entity], which comprise part of the APRA Annual Return, for the [year / period] ended .../.../.... I have conducted an independent reasonable assurance engagement on the relevant forms in order to expres ...

... (collectively known as the ‘relevant forms’) of …………………………….. [insert name of the superannuation entity], which comprise part of the APRA Annual Return, for the [year / period] ended .../.../.... I have conducted an independent reasonable assurance engagement on the relevant forms in order to expres ...

Competency area - Chartered Institute of Internal Auditors

... Chartered Institute of Internal Auditors 2013 ...

... Chartered Institute of Internal Auditors 2013 ...

Principles of Accounting I

... Dr. Johnson passed the Certified Public Accountant’s Exam in 1986 and become a member of the Colorado Society of Accountants, Colorado State Board of Accountancy and the American Institute of Certified Public Accountants. He became a member of The Bahamas Institute of Chartered Accountants in 1989, ...

... Dr. Johnson passed the Certified Public Accountant’s Exam in 1986 and become a member of the Colorado Society of Accountants, Colorado State Board of Accountancy and the American Institute of Certified Public Accountants. He became a member of The Bahamas Institute of Chartered Accountants in 1989, ...

Quality of Earnings Case Study Collection

... “Earnings Quality” has been a subject of SEC investigations, articles in most, if not all, business publications, and significant debate in recent years. It is a matter of importance in the financial reporting and regulatory communities, and it impacts the confidence of investors in our financial ma ...

... “Earnings Quality” has been a subject of SEC investigations, articles in most, if not all, business publications, and significant debate in recent years. It is a matter of importance in the financial reporting and regulatory communities, and it impacts the confidence of investors in our financial ma ...

CJAR Fundamentalist Perspective on Accounting Jiang

... The residual earnings model has had a long history. In the early part of the twentieth century, the idea that a firm’s value was based on “excess profits” was firmly established in the United Kingdom. The model is in the German literature of the 1920s and 1930s, particularly in the writings of Schma ...

... The residual earnings model has had a long history. In the early part of the twentieth century, the idea that a firm’s value was based on “excess profits” was firmly established in the United Kingdom. The model is in the German literature of the 1920s and 1930s, particularly in the writings of Schma ...

extract

... understand that which we cannot directly observe or measure rather than only “what is” (Bastiat, 1848; Hayek, 1989; Smith, 2003). Second, historical data provide unique opportunities to study issues of enduring importance. Finance and economics scholars increasingly use historical data to study impo ...

... understand that which we cannot directly observe or measure rather than only “what is” (Bastiat, 1848; Hayek, 1989; Smith, 2003). Second, historical data provide unique opportunities to study issues of enduring importance. Finance and economics scholars increasingly use historical data to study impo ...

Empirical evidence on liability caps and earnings management in

... affect audit quality. The study greatly contributed to the European Commission’s recommendation on the matter (European Commission 2008b). It identifies three main reasons why auditors’ liability in Europe should be limited: (1) the poor availability of auditor insurance especially for higher levels ...

... affect audit quality. The study greatly contributed to the European Commission’s recommendation on the matter (European Commission 2008b). It identifies three main reasons why auditors’ liability in Europe should be limited: (1) the poor availability of auditor insurance especially for higher levels ...

Chapter 1 - Accounting Information and Decision Making

... 9. Tax authorities decide on taxation policies. 10. Local communities decide on environmental issues. ...

... 9. Tax authorities decide on taxation policies. 10. Local communities decide on environmental issues. ...

FASB: Status of Statement 5

... 10. If no accrual is made for a loss contingency because one or both of the conditions in paragraph 8 are not met, or if an exposure to loss exists in excess of the amount accrued pursuant to the provisions of paragraph 8, disclosure of the contingency shall be made when there is at least a reasonab ...

... 10. If no accrual is made for a loss contingency because one or both of the conditions in paragraph 8 are not met, or if an exposure to loss exists in excess of the amount accrued pursuant to the provisions of paragraph 8, disclosure of the contingency shall be made when there is at least a reasonab ...

FASB: Status of Statement 5

... 10. If no accrual is made for a loss contingency because one or both of the conditions in paragraph 8 are not met, or if an exposure to loss exists in excess of the amount accrued pursuant to the provisions of paragraph 8, disclosure of the contingency shall be made when there is at least a reasonab ...

... 10. If no accrual is made for a loss contingency because one or both of the conditions in paragraph 8 are not met, or if an exposure to loss exists in excess of the amount accrued pursuant to the provisions of paragraph 8, disclosure of the contingency shall be made when there is at least a reasonab ...

The Role of Accounting in a Society

... approaches to the accounting research are all characterized by a more critical, often reformist thinking about its role, significance, and functioning in society (see, for example, critical accounting or radical accounting).1 They are based on the critical theory tradition,2 which serves as the foun ...

... approaches to the accounting research are all characterized by a more critical, often reformist thinking about its role, significance, and functioning in society (see, for example, critical accounting or radical accounting).1 They are based on the critical theory tradition,2 which serves as the foun ...

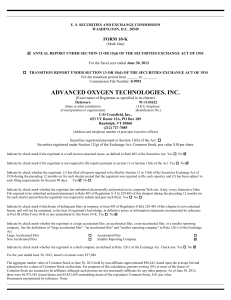

Advanced Oxygen Technologies 10K, June 30, 2012 - aoxy

... Non Accelerated Filer Smaller Reporting Company ...

... Non Accelerated Filer Smaller Reporting Company ...

Preview Sample File

... Feedback: Learning objective 1.3 - Understand the Conceptual Framework and the purpose of financial reporting. The objective of general purpose reporting forms the foundation of the Conceptual Framework. If we know why we need to report then who needs to report can be determined and then what and ho ...

... Feedback: Learning objective 1.3 - Understand the Conceptual Framework and the purpose of financial reporting. The objective of general purpose reporting forms the foundation of the Conceptual Framework. If we know why we need to report then who needs to report can be determined and then what and ho ...

ch02_sm_rankin

... Based on principles & objectives of financial reporting: To be consistent with the conceptual framework all items that meet the definition and recognition criteria of assets and liabilities should be included on the balance sheet. Also to be complete and so representationally faithful would argue ...

... Based on principles & objectives of financial reporting: To be consistent with the conceptual framework all items that meet the definition and recognition criteria of assets and liabilities should be included on the balance sheet. Also to be complete and so representationally faithful would argue ...

CHAPTER 1 – Principles of Accounting

... Accounting and Reporting Capabilities A governmental accounting system must make it possible both (a) to present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental unit in conformity with generally accepted a ...

... Accounting and Reporting Capabilities A governmental accounting system must make it possible both (a) to present fairly and with full disclosure the financial position and results of financial operations of the funds and account groups of the governmental unit in conformity with generally accepted a ...

Accounting for Government and Society

... likely to be a focus of attention and be actively and thoughtfully managed. Conversely, if we choose not to provide accounts of corporate behaviour in relation to employee conditions or environmental performance, then we are choosing one of at least four possibilities. First, we choose to trust the ...

... likely to be a focus of attention and be actively and thoughtfully managed. Conversely, if we choose not to provide accounts of corporate behaviour in relation to employee conditions or environmental performance, then we are choosing one of at least four possibilities. First, we choose to trust the ...

Examining the Accounting for Defined Benefit Pension Costs

... Calculating such obligations is a complex process, often requiring actuarial help. First, service costs represent “the actuarial present value of benefits attributed by the pension benefit formula to services rendered by employees during that period” (FASB 715-3020). Companies should match recognize ...

... Calculating such obligations is a complex process, often requiring actuarial help. First, service costs represent “the actuarial present value of benefits attributed by the pension benefit formula to services rendered by employees during that period” (FASB 715-3020). Companies should match recognize ...