united states securities and exchange commission - corporate

... The Notes were issued in a private offering exempt from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”), to qualified institutional buyers in accordance with Rule 144A and to persons outside of the United States pursuant to Regulation S under the Securi ...

... The Notes were issued in a private offering exempt from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”), to qualified institutional buyers in accordance with Rule 144A and to persons outside of the United States pursuant to Regulation S under the Securi ...

KRONOS ADVANCED TECHNOLOGIES INC (Form

... 60% of such controlling position and RS Properties converting such portion of the RS Note as is necessary to represent 40% of such controlling position, (3) to enter into the Lender Voting Agreement and (4) to make certain adjustments to the percentage of additional advances required to be made by A ...

... 60% of such controlling position and RS Properties converting such portion of the RS Note as is necessary to represent 40% of such controlling position, (3) to enter into the Lender Voting Agreement and (4) to make certain adjustments to the percentage of additional advances required to be made by A ...

American Italian Pasta Co.

... management information systems costs. The capitalization included inflated, arbitrary figures that were not based on actual measurement or appropriate calculation. Webster, Schmidgall, and others, were responsible for overstating AIPC's spare parts inventory by approximately $1.5 million, with a cor ...

... management information systems costs. The capitalization included inflated, arbitrary figures that were not based on actual measurement or appropriate calculation. Webster, Schmidgall, and others, were responsible for overstating AIPC's spare parts inventory by approximately $1.5 million, with a cor ...

words

... provisions as such expenses are incurred in advance of its final disposition, subject to repayment if it is ultimately determined that such party was not entitled to indemnity by the Registrant. The Registrant believes that these agreements are necessary to attract and retain qualified persons as di ...

... provisions as such expenses are incurred in advance of its final disposition, subject to repayment if it is ultimately determined that such party was not entitled to indemnity by the Registrant. The Registrant believes that these agreements are necessary to attract and retain qualified persons as di ...

66862 c07 296-365

... a finished product prior to sale. A good example of a manufacturing company is Winnebago Industries. It buys all of the various materials that are needed to build an RV, such as steel, glass, and tires, and then sells the finished product to its distributors, who sell the RVs to consumers. Whether a ...

... a finished product prior to sale. A good example of a manufacturing company is Winnebago Industries. It buys all of the various materials that are needed to build an RV, such as steel, glass, and tires, and then sells the finished product to its distributors, who sell the RVs to consumers. Whether a ...

- TestbankU

... Process Inventory. When a job is sold the entries are: (a) Debit Cash or Accounts Receivable and credit Sales Revenue for the selling price, and (b) Debit Cost of Goods Sold and credit Finished Goods Inventory for the cost of the goods. 5. Distinguish between under- or overapplied manufacturing over ...

... Process Inventory. When a job is sold the entries are: (a) Debit Cash or Accounts Receivable and credit Sales Revenue for the selling price, and (b) Debit Cost of Goods Sold and credit Finished Goods Inventory for the cost of the goods. 5. Distinguish between under- or overapplied manufacturing over ...

AMERCO /NV/ (Form: 8-K, Received: 09/13/2016 09:26:49)

... The series of N otes hereunder are not cross-defaulted or cross-collateralized to one another. Accordingly, a default by AMERCO under one series of N otes shall not trigger a default under any other series of N otes hereunder or under any other obligation of AMERCO or its affiliates. Additionally, ...

... The series of N otes hereunder are not cross-defaulted or cross-collateralized to one another. Accordingly, a default by AMERCO under one series of N otes shall not trigger a default under any other series of N otes hereunder or under any other obligation of AMERCO or its affiliates. Additionally, ...

Read the full report

... No part of this document may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as expressly permitted by law, without the prior written permission of the corresponding author. Limit ...

... No part of this document may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as expressly permitted by law, without the prior written permission of the corresponding author. Limit ...

15. mystery 6 dividend tier levels

... PIN means Personal Identification Number or other means of identification in the form required by the Company. Pool means the amount of money paid into a Totalizator, which after adjustment in accordance with the Rules, is available by way of Dividends to Investors who have made the appropriate Sele ...

... PIN means Personal Identification Number or other means of identification in the form required by the Company. Pool means the amount of money paid into a Totalizator, which after adjustment in accordance with the Rules, is available by way of Dividends to Investors who have made the appropriate Sele ...

NORTHWEST BIOTHERAPEUTICS INC (Form: 8-K

... Northwest Biotherapeutics, Inc. (the “Company”) announced today that, on September 7, 2005, it received a $500,000 loan from Toucan Capital Fund II, L.P. (“Toucan”). The loan accrues interest at 10% per year, matures on September 7, 2006, and the principal and interest is convertible into capital st ...

... Northwest Biotherapeutics, Inc. (the “Company”) announced today that, on September 7, 2005, it received a $500,000 loan from Toucan Capital Fund II, L.P. (“Toucan”). The loan accrues interest at 10% per year, matures on September 7, 2006, and the principal and interest is convertible into capital st ...

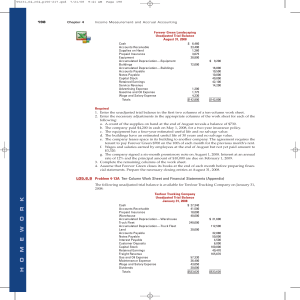

Lesson : 1

... predetermined basis, it is known as a Joint Venture. Joint venture is defined as a partnership confined to a particular adventure, speculation, course of trade or voyage, and in which partners, either latent or known use no firm or social name, and incur no responsibility beyond the limits of the ad ...

... predetermined basis, it is known as a Joint Venture. Joint venture is defined as a partnership confined to a particular adventure, speculation, course of trade or voyage, and in which partners, either latent or known use no firm or social name, and incur no responsibility beyond the limits of the ad ...

HOMEWORK

... illing itself as one of the world’s largest specialty retailers, Gap Inc. had its humble beginning when Doris and Don Fisher opened their first store in San Francisco in 1969. From that single store, the company has grown to operate more than 3,100 stores and to generate revenue that exceeded $15.9 ...

... illing itself as one of the world’s largest specialty retailers, Gap Inc. had its humble beginning when Doris and Don Fisher opened their first store in San Francisco in 1969. From that single store, the company has grown to operate more than 3,100 stores and to generate revenue that exceeded $15.9 ...

oncor electric delivery company llc - corporate

... WHEREAS, the Oncor Entities are “ring-fenced” from the Sellers and their Affiliates (as defined below), as a result of which, among other things, (i) the boards of directors of Oncor Holdings and Oncor are comprised of a majority of independent directors and (ii) certain arrangements are in place t ...

... WHEREAS, the Oncor Entities are “ring-fenced” from the Sellers and their Affiliates (as defined below), as a result of which, among other things, (i) the boards of directors of Oncor Holdings and Oncor are comprised of a majority of independent directors and (ii) certain arrangements are in place t ...

FSA001 – Balance sheet

... Report here those trade-related contingents which do not appear on the face of the balance sheet. Report short-term, self liquidating trade-related items such as documentary letters of credit issued by the firm which are, or are to be, collateralised by the underlying shipment, ie where the credit ...

... Report here those trade-related contingents which do not appear on the face of the balance sheet. Report short-term, self liquidating trade-related items such as documentary letters of credit issued by the firm which are, or are to be, collateralised by the underlying shipment, ie where the credit ...

CHAPTER 3

... *19. Wages paid during the year will include the payment of any wages attributable to the prior year but unpaid at the end of the prior year. This amount is an expense of the prior year and not of the current year, and thus should be subtracted in determining wages expense. Similarly, wages paid dur ...

... *19. Wages paid during the year will include the payment of any wages attributable to the prior year but unpaid at the end of the prior year. This amount is an expense of the prior year and not of the current year, and thus should be subtracted in determining wages expense. Similarly, wages paid dur ...

chapter 8 - Csulb.edu

... Which of the following statements is not valid as it applies to inventory costing methods? a. If inventory quantities are to be maintained, part of the earnings must be invested (plowed back) in inventories when FIFO is used during a period of rising prices. b. LIFO tends to smooth out the net incom ...

... Which of the following statements is not valid as it applies to inventory costing methods? a. If inventory quantities are to be maintained, part of the earnings must be invested (plowed back) in inventories when FIFO is used during a period of rising prices. b. LIFO tends to smooth out the net incom ...

united states securities and exchange commission - corporate

... name this Note (or one or more Predecessor Securities) is registered at the close of business on a Special Record Date for the payment of such Defaulted Interest to be fixed by the Company, notice whereof shall be given to Holders of Notes of this series not less than 10 days prior to such Special R ...

... name this Note (or one or more Predecessor Securities) is registered at the close of business on a Special Record Date for the payment of such Defaulted Interest to be fixed by the Company, notice whereof shall be given to Holders of Notes of this series not less than 10 days prior to such Special R ...

Chapter 02 Job Order Costing and Analysis

... 76. The Work in Process Inventory account of a manufacturing company that uses an overhead rate based on direct labor cost has a $4,400 debit balance after all posting is completed. The cost sheet of the one job still in process shows direct material cost of $2,000 and direct labor cost of $800. The ...

... 76. The Work in Process Inventory account of a manufacturing company that uses an overhead rate based on direct labor cost has a $4,400 debit balance after all posting is completed. The cost sheet of the one job still in process shows direct material cost of $2,000 and direct labor cost of $800. The ...

FAP 20e Chapter 4 SM - Arab Academy Research Papers AAST

... Income Summary account by closing revenue and expense accounts directly to the owner’s capital account.) ...

... Income Summary account by closing revenue and expense accounts directly to the owner’s capital account.) ...

Table of Contents - Ontario Energy Board

... balance), and other specified reporting or filings, the distributor is required to report using the alternative accounting standard, including the accounting procedures or requirements that the Board has stipulated. The terms “regulated” and “rate-regulated” as used in this APH do not imply a specif ...

... balance), and other specified reporting or filings, the distributor is required to report using the alternative accounting standard, including the accounting procedures or requirements that the Board has stipulated. The terms “regulated” and “rate-regulated” as used in this APH do not imply a specif ...

Accounts Receivable

... Tasanee was the accounts receivable clerk for a large non-profit foundation that provided performance and exhibition space for the performing and visual arts. Her responsibilities included activities normally assigned to an accounts receivable clerk, such as recording revenues from various sources t ...

... Tasanee was the accounts receivable clerk for a large non-profit foundation that provided performance and exhibition space for the performing and visual arts. Her responsibilities included activities normally assigned to an accounts receivable clerk, such as recording revenues from various sources t ...

Environmental Account Framing Workbook

... The Environmental account framing workbook (the Workbook) describes how to frame an environmental account. The methodology considers answers to a basic set of questions that are needed to scope and then specify an account. Before an environmental account can be produced, it must be framed. The frami ...

... The Environmental account framing workbook (the Workbook) describes how to frame an environmental account. The methodology considers answers to a basic set of questions that are needed to scope and then specify an account. Before an environmental account can be produced, it must be framed. The frami ...

nextera energy, inc. - corporate

... immediately preceding such Interest Payment Date; provided , however , that if any of the Debentures of the Thirty-Second Series are not held by a securities depository in book-entry form, the Regular Record Date will be the close of business on the fifteenth (15th) calendar day next preceding such ...

... immediately preceding such Interest Payment Date; provided , however , that if any of the Debentures of the Thirty-Second Series are not held by a securities depository in book-entry form, the Regular Record Date will be the close of business on the fifteenth (15th) calendar day next preceding such ...

Commissioner`s Statement CS 17/01

... Section CE 6(2) provides that, for the purposes of sections CE 2 to CE 4 and CE 7: (a) shares are treated as having been acquired on the date on which the right or option to acquire them is exercised; and (b) if shares or rights are acquired or transferred under an agreement by a trustee for the ben ...

... Section CE 6(2) provides that, for the purposes of sections CE 2 to CE 4 and CE 7: (a) shares are treated as having been acquired on the date on which the right or option to acquire them is exercised; and (b) if shares or rights are acquired or transferred under an agreement by a trustee for the ben ...

Accounts Receivable - University of New Orleans

... UNO and personal email addresses. If the email is returned, a hard copy is mailed. Must receive payment within 30 days. If a payment is not received within 30 days, a Final Pre-Collection Letter will be sent to the student. This notice will be sent via email to both the UNO and personal email addr ...

... UNO and personal email addresses. If the email is returned, a hard copy is mailed. Must receive payment within 30 days. If a payment is not received within 30 days, a Final Pre-Collection Letter will be sent to the student. This notice will be sent via email to both the UNO and personal email addr ...

Time book

A time book is a mostly outdated accounting record, that registered the hours worked by employees in a certain organization in a certain period. These records usually contain names of employees, type of work, hours worked, and sometimes wages paid.In the 19th and early 20th century time books were separate held records. In those days time books were held by company clerks or foremen or specialized timekeepers. These time books were used by the bookkeeper to determine the wages to be paid. The data was used in financial accounting to determine the weekly, monthly and annual labour costs, and in cost accounting to determine the cost price. Late 19th century additional time cards came in use to register labour hours.Nowadays the time book can be a part of an integrated payroll system, or cost accounting system. Those systems can contain registers that describe the labour time spend to produced products, but those registers are not regularly called time books, but timesheets.