Financial Accounting and Accounting Standards

... However, in the wake of the credit crisis of 2008, some countries, their central banks, and bank regulators wanted to suspend fair value accounting based on concerns that use of fair value accounting, which calls for recording significant losses on poorly performing loans and investments, would scar ...

... However, in the wake of the credit crisis of 2008, some countries, their central banks, and bank regulators wanted to suspend fair value accounting based on concerns that use of fair value accounting, which calls for recording significant losses on poorly performing loans and investments, would scar ...

Syngene International Limited Dividend Distribution Policy Version. No

... thereunder, may declare interim dividend or recommend final dividend, payable to the existing shareholders of the Company subject to shareholders’ approval. The Board may consider the free cash flow position, profit earned during that year, capex requirements, applicable taxes, overall market situat ...

... thereunder, may declare interim dividend or recommend final dividend, payable to the existing shareholders of the Company subject to shareholders’ approval. The Board may consider the free cash flow position, profit earned during that year, capex requirements, applicable taxes, overall market situat ...

Invitation to join the Refinancing Agreement and

... letter all holders of Financial Liability other than the Original Creditors (the Offerees) are offered the possibility to join such Refinancing Agreement and/or to choose between capitalization or write off from 35% of the amount in each one of the Financial Liability Section where Offerees have any ...

... letter all holders of Financial Liability other than the Original Creditors (the Offerees) are offered the possibility to join such Refinancing Agreement and/or to choose between capitalization or write off from 35% of the amount in each one of the Financial Liability Section where Offerees have any ...

LO 2 - Wiley

... Tasanee was the accounts receivable clerk for a large non-profit foundation that provided performance and exhibition space for the performing and visual arts. Her responsibilities included activities normally assigned to an accounts receivable clerk, such as recording revenues from various sources t ...

... Tasanee was the accounts receivable clerk for a large non-profit foundation that provided performance and exhibition space for the performing and visual arts. Her responsibilities included activities normally assigned to an accounts receivable clerk, such as recording revenues from various sources t ...

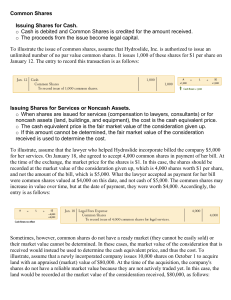

Common Shares

... $1.50 per share as assumed above. In this case, there would be a debit to the shareholders' equity account for the difference between the price paid to reacquire the shares and their average cost. If there is any balance in the contributed capital account from previous reacquisitions, this amount wo ...

... $1.50 per share as assumed above. In this case, there would be a debit to the shareholders' equity account for the difference between the price paid to reacquire the shares and their average cost. If there is any balance in the contributed capital account from previous reacquisitions, this amount wo ...

Laws: Securities Market Act of The Islamic Republic of Iran

... their legally assigned duties in the best possible manner, take the utmost care and impartiality in the exercise of their functions, ensure that all the resolutions adopted are in the interests of the country and observe the secrecy and confidentiality of the information provided by the Organization ...

... their legally assigned duties in the best possible manner, take the utmost care and impartiality in the exercise of their functions, ensure that all the resolutions adopted are in the interests of the country and observe the secrecy and confidentiality of the information provided by the Organization ...

The Role of Accounting in a Society

... expressed nicely by Arnold (2009, p. 805)—“cling to the disfunct notion that more transparency will somehow revive confidence in financial markets and enable them to function efficiently once again.” An in-depth social critique within such understanding of accounting is extremely difficult to make b ...

... expressed nicely by Arnold (2009, p. 805)—“cling to the disfunct notion that more transparency will somehow revive confidence in financial markets and enable them to function efficiently once again.” An in-depth social critique within such understanding of accounting is extremely difficult to make b ...

30DC, INC. (Form: SC 13D/A, Received: 01/08/2016

... Funded Capital Raise Of At Least $500,000, From Investors Introduced To Client By Consultant - Six Hundred Thousand (600,000) restricted 144 securities of the Client stock Client M&A Activity: Consummation Of Merger Or Acquisition Of Client By Party Introduced To Client By Consultant - Six Hundred T ...

... Funded Capital Raise Of At Least $500,000, From Investors Introduced To Client By Consultant - Six Hundred Thousand (600,000) restricted 144 securities of the Client stock Client M&A Activity: Consummation Of Merger Or Acquisition Of Client By Party Introduced To Client By Consultant - Six Hundred T ...

Local Government Ethics Law

... business organization in which he has an interest, shall solicit or accept any gift, favor, loan, political contribution, service, promise of future employment, or other thing of value based upon an understanding that the gift, favor, loan, contribution, service, promise, or other thing of value was ...

... business organization in which he has an interest, shall solicit or accept any gift, favor, loan, political contribution, service, promise of future employment, or other thing of value based upon an understanding that the gift, favor, loan, contribution, service, promise, or other thing of value was ...

As filed with the Securities and Exchange Commission on January

... that a corporation has the power to indemnify a director, officer, employee or agent of the corporation and certain other persons serving at the request of the corporation in related capacities against amounts paid and expenses incurred in connection with an action or proceeding to which he is or is ...

... that a corporation has the power to indemnify a director, officer, employee or agent of the corporation and certain other persons serving at the request of the corporation in related capacities against amounts paid and expenses incurred in connection with an action or proceeding to which he is or is ...

term sheet - Anti

... to the Series A Preferred];6 (iii) create or authorize the creation of [or issue or obligate itself to issue shares of,] any other security convertible into or exercisable for any equity security, having rights, preferences or privileges senior to or on parity with the Series A Preferred, or increa ...

... to the Series A Preferred];6 (iii) create or authorize the creation of [or issue or obligate itself to issue shares of,] any other security convertible into or exercisable for any equity security, having rights, preferences or privileges senior to or on parity with the Series A Preferred, or increa ...

Accounting for Government and Society

... and patrons, and the belief systems and priorities of the cartographer. Maps are as much about money, empire and discovery as about space: “the idea of the world may be common to all societies, but different societies have very distinct ideas of the world and how it should be represented” (ibid). Li ...

... and patrons, and the belief systems and priorities of the cartographer. Maps are as much about money, empire and discovery as about space: “the idea of the world may be common to all societies, but different societies have very distinct ideas of the world and how it should be represented” (ibid). Li ...

Chapter 11

... & Investment Decisions • The Weighted Marginal Cost of Capital (WMCC) – The WACC typically increases as the volume of new capital raised within a given period increases. – This is true because companies need to raise the return to investors in order to entice them to invest to compensate them for th ...

... & Investment Decisions • The Weighted Marginal Cost of Capital (WMCC) – The WACC typically increases as the volume of new capital raised within a given period increases. – This is true because companies need to raise the return to investors in order to entice them to invest to compensate them for th ...

DMO Cost Principles - Department of Defence

... objective to standardise the applicability and transparency of the cost basis used in Defence contracts. The document details the Cost Principles that Defence and Industry will utilise towards contract costs. This release reflects the transition from the Defence Materiel Organisation to the Capabili ...

... objective to standardise the applicability and transparency of the cost basis used in Defence contracts. The document details the Cost Principles that Defence and Industry will utilise towards contract costs. This release reflects the transition from the Defence Materiel Organisation to the Capabili ...

FORM 8-K

... limited liability company, partnership, joint venture, trust or other entity or enterprise (collectively with the Company, " Enterprise ") or by reason of an action or inaction by Indemnitee in any such capacity (whether or not serving in such capacity at the time any Loss is incurred for which inde ...

... limited liability company, partnership, joint venture, trust or other entity or enterprise (collectively with the Company, " Enterprise ") or by reason of an action or inaction by Indemnitee in any such capacity (whether or not serving in such capacity at the time any Loss is incurred for which inde ...

Note Purchase Agreement

... and shall submit to the Company such further assurances of such status as may be reasonably requested by the Company. The residency of the Investor (or, in the case of a partnership or corporation, such entity’s principal place of business) is correctly set forth beneath such Investor’s name on Sche ...

... and shall submit to the Company such further assurances of such status as may be reasonably requested by the Company. The residency of the Investor (or, in the case of a partnership or corporation, such entity’s principal place of business) is correctly set forth beneath such Investor’s name on Sche ...

Aue2602 Summary

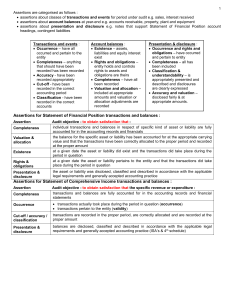

... payment from debtor actually occurred and pertains to entity (occurrence) receipts are recorded at correct amount (accuracy) and are allocated to the proper accounting period (cut-off) all receipts have been recorded (completeness) in the proper accounts (classification) Debtors and bank / cas ...

... payment from debtor actually occurred and pertains to entity (occurrence) receipts are recorded at correct amount (accuracy) and are allocated to the proper accounting period (cut-off) all receipts have been recorded (completeness) in the proper accounts (classification) Debtors and bank / cas ...

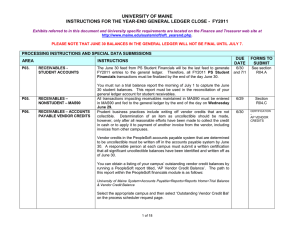

1 - University of Maine

... accrued to FY2011 and so that the System Office can roll open purchase orders over to FY2012. (2) Purchase Orders created between July 1 and July 19 Purchase Orders created between July 1 and July 19 must have an accounting date consistent with the fiscal year for which the purchase occurred. FY11 p ...

... accrued to FY2011 and so that the System Office can roll open purchase orders over to FY2012. (2) Purchase Orders created between July 1 and July 19 Purchase Orders created between July 1 and July 19 must have an accounting date consistent with the fiscal year for which the purchase occurred. FY11 p ...

xerium technologies, inc. - corporate

... This Xerium Technologies, Inc. 2016-2018 Executive Long Term Incentive Plan (the "Executive LTIP") contains rules supplemental to those set forth in the Xerium Technologies, Inc. 2010 Equity Incentive Plan (the "EIP"). The Executive LTIP provides for the grant of incentive award opportunities (each, ...

... This Xerium Technologies, Inc. 2016-2018 Executive Long Term Incentive Plan (the "Executive LTIP") contains rules supplemental to those set forth in the Xerium Technologies, Inc. 2010 Equity Incentive Plan (the "EIP"). The Executive LTIP provides for the grant of incentive award opportunities (each, ...

Chap007

... period, and the allowance is the accumulated result of events over a number of prior periods. The only way that they could be equal would be if write-offs during the prior period exactly equaled the beginning balance of the Allowance account. ...

... period, and the allowance is the accumulated result of events over a number of prior periods. The only way that they could be equal would be if write-offs during the prior period exactly equaled the beginning balance of the Allowance account. ...

Pricing Decisions EMBA 5412 Fall 2010

... Nownew company feels that there is a market niche for a mouse with special new features. After surveying the features and prices of available mouses on the market, Marketing department believes that a price of TL 30 would be about right for the new mouse. Marketing department estimates to sell about ...

... Nownew company feels that there is a market niche for a mouse with special new features. After surveying the features and prices of available mouses on the market, Marketing department believes that a price of TL 30 would be about right for the new mouse. Marketing department estimates to sell about ...

FAP 20e Chapter 9 SM

... for estimated uncollectibles be recorded in the same period when revenues from those receivables are recorded. This means that in the case of accounts receivable, both U.S. GAAP and IFRS require the allowance method for uncollectibles (unless immaterial). ...

... for estimated uncollectibles be recorded in the same period when revenues from those receivables are recorded. This means that in the case of accounts receivable, both U.S. GAAP and IFRS require the allowance method for uncollectibles (unless immaterial). ...

FREE Sample Here - We can offer most test bank and

... A company sells goods for $150,000 that cost $60,000 to manufacture. Which statement(s) are true? The company will recognize sales on the balance sheet of $150,000. The company will recognize $90,000 gross profit on the balance sheet. The company will decrease finished goods by $60,000. All of these ...

... A company sells goods for $150,000 that cost $60,000 to manufacture. Which statement(s) are true? The company will recognize sales on the balance sheet of $150,000. The company will recognize $90,000 gross profit on the balance sheet. The company will decrease finished goods by $60,000. All of these ...

Fiscal Policies and Procedures Guide

... 205 Government Access to Records ........................................................................ 10 206 Security of Financial Data ................................................................................ 10 207 Security of School Documents............................................ ...

... 205 Government Access to Records ........................................................................ 10 206 Security of Financial Data ................................................................................ 10 207 Security of School Documents............................................ ...

Cost Accounting

... xi. To supply useful data to the management to take various financial decisions such as introduction of new products, replacement of labour by machine etc. xii. To organize an effective information system so that different levels of management may get required information at the right time in right ...

... xi. To supply useful data to the management to take various financial decisions such as introduction of new products, replacement of labour by machine etc. xii. To organize an effective information system so that different levels of management may get required information at the right time in right ...

Time book

A time book is a mostly outdated accounting record, that registered the hours worked by employees in a certain organization in a certain period. These records usually contain names of employees, type of work, hours worked, and sometimes wages paid.In the 19th and early 20th century time books were separate held records. In those days time books were held by company clerks or foremen or specialized timekeepers. These time books were used by the bookkeeper to determine the wages to be paid. The data was used in financial accounting to determine the weekly, monthly and annual labour costs, and in cost accounting to determine the cost price. Late 19th century additional time cards came in use to register labour hours.Nowadays the time book can be a part of an integrated payroll system, or cost accounting system. Those systems can contain registers that describe the labour time spend to produced products, but those registers are not regularly called time books, but timesheets.