Are banks still special when there is a secondary market for loans?

... It is commonly argued that banks play a special role in the financial system because they resolve important information asymmetries. Theoretical models (e.g., Diamond (1984), Ramakrishnan and Thakor (1984), Fama (1985)) highlight the unique monitoring functions of banks, and show that banks have a ...

... It is commonly argued that banks play a special role in the financial system because they resolve important information asymmetries. Theoretical models (e.g., Diamond (1984), Ramakrishnan and Thakor (1984), Fama (1985)) highlight the unique monitoring functions of banks, and show that banks have a ...

Research Institute

... frontier markets relative to their emerging market peers. The normalized standard deviation in real GDP growth over the past 35 years is 0.6% for CS FM, double that of MSCI emerging markets, although excluding China raises the volatility for the rest of emerging markets to 0.5%. Using International ...

... frontier markets relative to their emerging market peers. The normalized standard deviation in real GDP growth over the past 35 years is 0.6% for CS FM, double that of MSCI emerging markets, although excluding China raises the volatility for the rest of emerging markets to 0.5%. Using International ...

11: Corporate Finance: Corporate Investing and Financing Decisions

... The weighted average cost of capital is a weighted average of the marginal costs of each relevant component. The weights are based on the percentage each particular component represents in the firm’s capital structure. Those sources providing more financing of firm assets have a greater weight in ca ...

... The weighted average cost of capital is a weighted average of the marginal costs of each relevant component. The weights are based on the percentage each particular component represents in the firm’s capital structure. Those sources providing more financing of firm assets have a greater weight in ca ...

NP 2012 COC 1 Q.

... feasible portfolio proportions (X1, … XN) into feasible combinations of: (i) expected return and variance of return; or (ii) expected return and standard deviation of return. Figure I shows one such feasible set of Ep, SDp, combinations. Consider portfolio A shown in Figure I. Rational Markowitz mea ...

... feasible portfolio proportions (X1, … XN) into feasible combinations of: (i) expected return and variance of return; or (ii) expected return and standard deviation of return. Figure I shows one such feasible set of Ep, SDp, combinations. Consider portfolio A shown in Figure I. Rational Markowitz mea ...

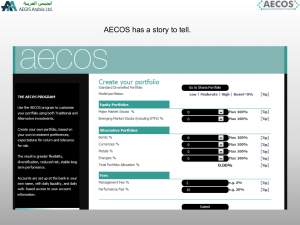

Portfolio Comparisons. - Artex Component System

... The AECOS program allows investors to test different portfolio strategies to determine the best mix of sectors, and the proper leverage to apply. Results for each sector are from the Aegis investment programs. Past results cannot predict future returns, but the AECOS program is designed primarily to ...

... The AECOS program allows investors to test different portfolio strategies to determine the best mix of sectors, and the proper leverage to apply. Results for each sector are from the Aegis investment programs. Past results cannot predict future returns, but the AECOS program is designed primarily to ...

Shaping change in insurance - Analysts` conference 2017

... without weakening resilience against future volatility Run-off change of ultimate basic and major losses1 ...

... without weakening resilience against future volatility Run-off change of ultimate basic and major losses1 ...

printmgr file - Goldman Sachs

... Commitments, contingencies and guarantees Shareholders’ equity Preferred stock, par value $0.01 per share; aggregate liquidation preference of $9,200 and $7,200 as of September 2014 and December 2013, respectively Common stock, par value $0.01 per share; 4,000,000,000 shares authorized, 851,632,488 ...

... Commitments, contingencies and guarantees Shareholders’ equity Preferred stock, par value $0.01 per share; aggregate liquidation preference of $9,200 and $7,200 as of September 2014 and December 2013, respectively Common stock, par value $0.01 per share; 4,000,000,000 shares authorized, 851,632,488 ...

What Difference Do Dividends Make?

... Once the sample was segmented by investment style, we formed four dividend yield portfolios within each style category: no dividend, low dividend, high dividend, and extreme dividend. We divided the dividend payers, roughly in half, into low- and high-dividend portfolios; within the dividend-paying ...

... Once the sample was segmented by investment style, we formed four dividend yield portfolios within each style category: no dividend, low dividend, high dividend, and extreme dividend. We divided the dividend payers, roughly in half, into low- and high-dividend portfolios; within the dividend-paying ...

Capital Flows are Fickle: Anytime, Anywhere 183 WP/13/

... mixed enthusiasm (see Broner and Rigobon, 2006). There are also concerns that flows to emerging markets are overly sensitive to “push” factors that are beyond the influence of domestic policies. Over the last decade however, even as emerging markets have become more attractive for foreign investors, ...

... mixed enthusiasm (see Broner and Rigobon, 2006). There are also concerns that flows to emerging markets are overly sensitive to “push” factors that are beyond the influence of domestic policies. Over the last decade however, even as emerging markets have become more attractive for foreign investors, ...

Limit Order Markets: A Survey 1

... the Paris Bourse ran batch auctions. Periodically, an auctioneer aggregated orders and announced a market-clearing price. Later in the 1980s when Kyle [1985] and Glosten and Milgrom [1985] published their own eponymous theories of financial markets, the intermediation activities of NYSE specialists, ...

... the Paris Bourse ran batch auctions. Periodically, an auctioneer aggregated orders and announced a market-clearing price. Later in the 1980s when Kyle [1985] and Glosten and Milgrom [1985] published their own eponymous theories of financial markets, the intermediation activities of NYSE specialists, ...

OECD - Business Angels Netzwerk Deutschland eV

... outside equity financing for start-ups in a number of countries, yet it is frequently overlooked as angel investors are often not visible. Following the recent financial crisis and continued difficult economic environment, angel investors have been playing an important role in filling financing gaps ...

... outside equity financing for start-ups in a number of countries, yet it is frequently overlooked as angel investors are often not visible. Following the recent financial crisis and continued difficult economic environment, angel investors have been playing an important role in filling financing gaps ...

2009 Annual Report - Berkshire Hathaway Inc.

... Berkshire shares sold at an appropriate discount to the book value of its underearning textile assets, whereas today Berkshire shares regularly sell at a premium to the accounting values of its first-class businesses. Summed up, the table on page 2 conveys three messages, two positive and one hugely ...

... Berkshire shares sold at an appropriate discount to the book value of its underearning textile assets, whereas today Berkshire shares regularly sell at a premium to the accounting values of its first-class businesses. Summed up, the table on page 2 conveys three messages, two positive and one hugely ...

Cumulative Prospect Theory, Aggregation, and Pricing

... One might wonder how CPT performs in an incomplete market with limited trading opportunities. However, the context in which the CPT has been used to explain anomalies — the stock market — is unlikely to be a good example since derivative financial assets are so easily created. In any case, as aggreg ...

... One might wonder how CPT performs in an incomplete market with limited trading opportunities. However, the context in which the CPT has been used to explain anomalies — the stock market — is unlikely to be a good example since derivative financial assets are so easily created. In any case, as aggreg ...

Aggregation of risks and Allocation of capital

... The current focus is on calculating economic capital. However, business decisions need to be made based on risk budget and risk/return optimization. Economic capital plays a central role in prudential supervision, product pricing, risk assessment, risk management and hedging, capital allocation / pr ...

... The current focus is on calculating economic capital. However, business decisions need to be made based on risk budget and risk/return optimization. Economic capital plays a central role in prudential supervision, product pricing, risk assessment, risk management and hedging, capital allocation / pr ...

Distress Anomaly and Shareholder Risk: International Evidence Assaf Eisdorfer

... We also examine the effect of information transparency on the distress anomaly. Low quality of accounting standards/disclosures makes it harder to assess the true probability of bankruptcy and therefore leaves more room for misvaluation of distressed securities. This represents an additional source ...

... We also examine the effect of information transparency on the distress anomaly. Low quality of accounting standards/disclosures makes it harder to assess the true probability of bankruptcy and therefore leaves more room for misvaluation of distressed securities. This represents an additional source ...

Guidance on Substantive Merger Control

... The purpose of merger control is to protect competition as an effective process. Protecting competition at the same time protects the interests of consumers, not necessarily in the short term but rather in the longer term and on a more permanent basis.4 The general aim of merger control is to protec ...

... The purpose of merger control is to protect competition as an effective process. Protecting competition at the same time protects the interests of consumers, not necessarily in the short term but rather in the longer term and on a more permanent basis.4 The general aim of merger control is to protec ...

ASX Clear Schedule 01 - Risk Based Capital Requirements

... against Australian dollars on each Business Day, having a settlement period of 2 days. “Non-Standard Risk Requirement” means the amount calculated in accordance with Rule S1.2.9 to cover unusual or non-standard exposures. “Operational Risk Requirement” means the amount calculated in accordance with ...

... against Australian dollars on each Business Day, having a settlement period of 2 days. “Non-Standard Risk Requirement” means the amount calculated in accordance with Rule S1.2.9 to cover unusual or non-standard exposures. “Operational Risk Requirement” means the amount calculated in accordance with ...

Submission 7 - Fiduciary Friend Pty Ltd

... different investment options for members based on lifecycle factors such as age. While this recognises the different investment priorities of say a 20 year old compared with a 55 year old, it does not recognise that even two 20 year olds may have different investment horizons due to say differences ...

... different investment options for members based on lifecycle factors such as age. While this recognises the different investment priorities of say a 20 year old compared with a 55 year old, it does not recognise that even two 20 year olds may have different investment horizons due to say differences ...

Negotiating an Equity Capital Infusion from Outside Investors

... The process of seeking and securing third-party financing is often lengthy. For an MFI that is seeking outside capital for the first time, it may take as long as six months or more to complete the process. Investors will typically conduct a thorough due diligence investigation of the financial, oper ...

... The process of seeking and securing third-party financing is often lengthy. For an MFI that is seeking outside capital for the first time, it may take as long as six months or more to complete the process. Investors will typically conduct a thorough due diligence investigation of the financial, oper ...

Two Essays on Managerial Behaviors in the Mutual Fund Industry

... Because the SEC allows managers to file their reports with 60-day delay, a large number of mutual funds postpone their portfolio disclosure. Poorly performing managers could benefit from window-dressing with delayed reports. If a poorly performing manager window-dresses and fund performance improve ...

... Because the SEC allows managers to file their reports with 60-day delay, a large number of mutual funds postpone their portfolio disclosure. Poorly performing managers could benefit from window-dressing with delayed reports. If a poorly performing manager window-dresses and fund performance improve ...

Mutual Funds and Bubbles: The Surprising Role of Contractual

... See Dow Jones News Service (1997), for instance. ...

... See Dow Jones News Service (1997), for instance. ...

Aims and purpose of the Fund

... The discount rate in excess of CPI inflation (the “real discount rate”) has been derived based on the expected return on the Fund’s assets based on the long term strategy set out in its Investment Strategy Statement (ISS). When assessing the appropriate prudent discount rate, consideration has been ...

... The discount rate in excess of CPI inflation (the “real discount rate”) has been derived based on the expected return on the Fund’s assets based on the long term strategy set out in its Investment Strategy Statement (ISS). When assessing the appropriate prudent discount rate, consideration has been ...

Transition to IFRS and value relevance in a small but developed

... statements (IASC Framework, paragraph 10). They are not debt and tax oriented as traditionally are the accounting regulations in code law or continental European countries. In fact, IFRS are supposed to reflect economic gains and losses in a more timely fashion (Barth et al., 2008) and to provide mo ...

... statements (IASC Framework, paragraph 10). They are not debt and tax oriented as traditionally are the accounting regulations in code law or continental European countries. In fact, IFRS are supposed to reflect economic gains and losses in a more timely fashion (Barth et al., 2008) and to provide mo ...

Private equity secondary market

In finance, the private equity secondary market (also often called private equity secondaries or secondaries) refers to the buying and selling of pre-existing investor commitments to private equity and other alternative investment funds. Given the absence of established trading markets for these interests, the transfer of interests in private equity funds as well as hedge funds can be more complex and labor-intensive.Sellers of private equity investments sell not only the investments in the fund but also their remaining unfunded commitments to the funds. By its nature, the private equity asset class is illiquid, intended to be a long-term investment for buy-and-hold investors, including ""pension funds, endowments and wealthy families selling off their private equity funds before the pools have sold off all their assets."" For the vast majority of private equity investments, there is no listed public market; however, there is a robust and maturing secondary market available for sellers of private equity assets.Buyers seek to acquire private equity interests in the secondary market for multiple reasons. For example, the duration of the investment may be much shorter than an investment in the private equity fund initially. Likewise, the buyer may be able to acquire these interests at an attractive price. Finally, the buyer can evaluate the fund's holdings before deciding to purchase an interest in the fund. Conversely, sellers may seek to sell interest for various reasons, including the need to raise capital, the desire to avoid future capital calls, the need to reduce an over-allocation to the asset class or for regulatory reasons.Driven by strong demand for private equity exposure over the past decade, a significant amount of capital has been committed to secondary market funds from investors looking to increase and diversify their private equity exposure.