RossFCF8ce_SM_ch13

... (LO3) If the market expected the growth rate in the coming year to be 2 percent, then there would be no change in security prices if this expectation had been fully anticipated and priced. However, if the market had been expecting a growth rate different than 2 percent and the expectation was incorp ...

... (LO3) If the market expected the growth rate in the coming year to be 2 percent, then there would be no change in security prices if this expectation had been fully anticipated and priced. However, if the market had been expecting a growth rate different than 2 percent and the expectation was incorp ...

Is There Price Discovery in Equity Options?

... that option market price discovery appears to have declined since the sample period used in some of the earlier literature, e.g. Chakravarty, Gulen, and Mayhew (2004), and thus help reconcile our results with those in the earlier literature. In interpreting our results within the context of the exis ...

... that option market price discovery appears to have declined since the sample period used in some of the earlier literature, e.g. Chakravarty, Gulen, and Mayhew (2004), and thus help reconcile our results with those in the earlier literature. In interpreting our results within the context of the exis ...

The Hybrid Consumer: Exploring the Drivers of a New

... trading down to low-priced products and services and simultaneously trading up to premium ones and avoiding the “boring middle”, which is perceived as offering little added value: neither unbeatable prices nor unbeatable quality. Understanding the changing attitudes, behaviours and values of middle- ...

... trading down to low-priced products and services and simultaneously trading up to premium ones and avoiding the “boring middle”, which is perceived as offering little added value: neither unbeatable prices nor unbeatable quality. Understanding the changing attitudes, behaviours and values of middle- ...

PDF

... The sample for this study consists of a subset of the advisory programs that were evaluated by the AgMAS Project from 1995 to 2001.4 The term “advisory program” is used because several advisory services have more than one distinct marketing program. When it was first launched, AgMAS monitored and ev ...

... The sample for this study consists of a subset of the advisory programs that were evaluated by the AgMAS Project from 1995 to 2001.4 The term “advisory program” is used because several advisory services have more than one distinct marketing program. When it was first launched, AgMAS monitored and ev ...

Effect of Investor Sentiment on Market Response to Stock Splits

... as the difference of the average market-to-book ratios of dividend paying stocks and nondividend paying stocks as the sentiment proxy. Since dividend paying stocks resemble bonds in that their predictable income stream represents a salient characteristic of safety, investors prefer dividend payers t ...

... as the difference of the average market-to-book ratios of dividend paying stocks and nondividend paying stocks as the sentiment proxy. Since dividend paying stocks resemble bonds in that their predictable income stream represents a salient characteristic of safety, investors prefer dividend payers t ...

Merrill Edge® Self-Directed Investing Terms of Service

... In addition to retaining the sole responsibility for investment decisions, you understand and agree that you are responsible for knowing the rights and terms of all securities in your account, specifically including valuable rights that expire unless the holder takes action. This includes, but is no ...

... In addition to retaining the sole responsibility for investment decisions, you understand and agree that you are responsible for knowing the rights and terms of all securities in your account, specifically including valuable rights that expire unless the holder takes action. This includes, but is no ...

Technical Analysis

... Many non-arbitrage algorithmic trading systems rely on the idea of trend-following, as do many hedge funds. A relatively recent trend, both in research and industrial practice, has been the development of increasingly sophisticated automated trading strategies. These often rely on underlying technic ...

... Many non-arbitrage algorithmic trading systems rely on the idea of trend-following, as do many hedge funds. A relatively recent trend, both in research and industrial practice, has been the development of increasingly sophisticated automated trading strategies. These often rely on underlying technic ...

The market impact of large trading orders

... based on empirically observable assumptions, taking the strategic motivations for order splitting as a given. The model contains only two types of traders, liquidity takers and liquidity providers. The liquidity takers are noise traders who decide to buy or sell at random, picking a random size V fo ...

... based on empirically observable assumptions, taking the strategic motivations for order splitting as a given. The model contains only two types of traders, liquidity takers and liquidity providers. The liquidity takers are noise traders who decide to buy or sell at random, picking a random size V fo ...

Tax and Liquidity Effects in Pricing Government Bonds

... wishes to thank Nasdaq for financial assistance. ...

... wishes to thank Nasdaq for financial assistance. ...

Option Trading, Reference Prices, and Volatility Kelley Bergsma

... a new setting for testing of the well-known disposition effect. A few studies document a traditional disposition effect in derivatives, including executive stock option grants, futures, and bank-issued warrants (Heath, Huddart, and Lang 1999; Coval and Shumway 2005; Choe and Eom 2009; Schmitz and W ...

... a new setting for testing of the well-known disposition effect. A few studies document a traditional disposition effect in derivatives, including executive stock option grants, futures, and bank-issued warrants (Heath, Huddart, and Lang 1999; Coval and Shumway 2005; Choe and Eom 2009; Schmitz and W ...

Stop-loss orders and price cascades in currency markets

... which suggests that share purchases affect prices differently than sales. Short sales constraints, which are fairly severe in U.S. equity markets, have been implicated as a potential source of the difference between the effects of share purchases and sales on stock prices. Since there are no short s ...

... which suggests that share purchases affect prices differently than sales. Short sales constraints, which are fairly severe in U.S. equity markets, have been implicated as a potential source of the difference between the effects of share purchases and sales on stock prices. Since there are no short s ...

stop-loss orders and price cascades in currency markets

... which suggests that share purchases affect prices differently than sales. Short sales constraints, which are fairly severe in U.S. equity markets, have been implicated as a potential source of the difference between the effects of share purchases and sales on stock prices. Since there are no short s ...

... which suggests that share purchases affect prices differently than sales. Short sales constraints, which are fairly severe in U.S. equity markets, have been implicated as a potential source of the difference between the effects of share purchases and sales on stock prices. Since there are no short s ...

2. Return

... underwriting of a bond issue. Less well known is the fundamental role that duality theory plays in the theoretical treatment of the pricing of options and contingent claims, both in its discrete state and time formulation using linear programming and in its continuous time counterparts. This duality ...

... underwriting of a bond issue. Less well known is the fundamental role that duality theory plays in the theoretical treatment of the pricing of options and contingent claims, both in its discrete state and time formulation using linear programming and in its continuous time counterparts. This duality ...

Remaking the corporate bond market

... nuanced discussion of the state and evolution of the market, rather than drawing more linear or reductionist conclusions. ...

... nuanced discussion of the state and evolution of the market, rather than drawing more linear or reductionist conclusions. ...

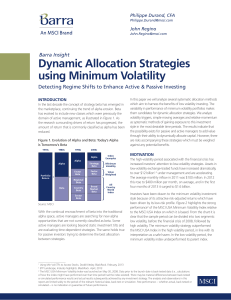

Dynamic Allocation Strategies using Minimum Volatility

... them candidates for dynamic allocation strategies. We analyze volatility triggers, simple moving averages and relative momentum as systematic methods of gaining exposure to this investment style in the most desirable time periods. The results indicate that the possibility exists for passive and acti ...

... them candidates for dynamic allocation strategies. We analyze volatility triggers, simple moving averages and relative momentum as systematic methods of gaining exposure to this investment style in the most desirable time periods. The results indicate that the possibility exists for passive and acti ...

Chicago Board of Trade (CBOT)

... • Treasury futures contracts are based on a 6% coupon • There are several issues that are deliverable into a Treasury futures contract • Treasury futures prices track the “cheapest to deliver” security, the single instrument that generally stands out as the “cheapest” or most economical to deliver-- ...

... • Treasury futures contracts are based on a 6% coupon • There are several issues that are deliverable into a Treasury futures contract • Treasury futures prices track the “cheapest to deliver” security, the single instrument that generally stands out as the “cheapest” or most economical to deliver-- ...

Common Option Strategies - NYU Stern School of Business

... long vol or being short vol? The answer is short vol, at least since the beginning of the 2001 calendar year. Option time values were “taken in” during 2001 arguably because there has been a “volatility supply glut” or “volatility overhang”. If one thinks of volatility as a commodity like wheat, the ...

... long vol or being short vol? The answer is short vol, at least since the beginning of the 2001 calendar year. Option time values were “taken in” during 2001 arguably because there has been a “volatility supply glut” or “volatility overhang”. If one thinks of volatility as a commodity like wheat, the ...

The Effects of Capital Structure Change on Security Prices

... approximations to pure capital structure changes: intra-firm exchange offers and recapitalizations. These two events are unique in that they do not entail any firm cash inflows or outflows (with the exception of expenses), while they cause major changes in the firm's capital structure. These changes ...

... approximations to pure capital structure changes: intra-firm exchange offers and recapitalizations. These two events are unique in that they do not entail any firm cash inflows or outflows (with the exception of expenses), while they cause major changes in the firm's capital structure. These changes ...

VaR Exceedances at Large Financial Institutions

... The concept of VaR is easy to understand. VaR can be applied to different asset classes and security types. It allows us to boil down the risk of an entire portfolio, no matter how complex, to a single number. Importantly for the purposes of this paper, VaR is easy to backtest. Large financial insti ...

... The concept of VaR is easy to understand. VaR can be applied to different asset classes and security types. It allows us to boil down the risk of an entire portfolio, no matter how complex, to a single number. Importantly for the purposes of this paper, VaR is easy to backtest. Large financial insti ...

Shareholder Wealth and Volatility Effects of Stock Splits Some

... undertaken a stock split during the research period of 1988–1997 were the earlier master’s theses of Hovmöller & Wasing (1997) and Olsson & Söderblom (1996). For the years 1996– 1997 the primary source was the www-on-line service of the Stockholm Stock Exchange13. Furthermore, the Datastream system ...

... undertaken a stock split during the research period of 1988–1997 were the earlier master’s theses of Hovmöller & Wasing (1997) and Olsson & Söderblom (1996). For the years 1996– 1997 the primary source was the www-on-line service of the Stockholm Stock Exchange13. Furthermore, the Datastream system ...

Research on SOGO SHOSHA: Origins, Establishment, and

... companies like SOGO SHOSHA. As a result, general trading companies grew rapidly in South Korea and heavily contributed to its economic development. They have similarities to Japanese SOGO SHOSHA, but also have many differences such as that they couldn’t get out of the role of contact center they pla ...

... companies like SOGO SHOSHA. As a result, general trading companies grew rapidly in South Korea and heavily contributed to its economic development. They have similarities to Japanese SOGO SHOSHA, but also have many differences such as that they couldn’t get out of the role of contact center they pla ...

Workbook for Currency Derivatives Certification Examination

... get a paper promising that value of that paper at any point of time would be equal to certain number of gold coins. This system of book entry of coins against paper was the start of paper currency. With time, countries started trading across borders as they realized that everything cannot be produce ...

... get a paper promising that value of that paper at any point of time would be equal to certain number of gold coins. This system of book entry of coins against paper was the start of paper currency. With time, countries started trading across borders as they realized that everything cannot be produce ...

Mastering The Markets

... The average person has absolutely no idea what drives the financial markets. Even more surprising is the fact that the average trader doesn’t understand what drives the markets either! Many traders are quite happy to blindly follow mechanical systems, based on mathematical formulas that have been ba ...

... The average person has absolutely no idea what drives the financial markets. Even more surprising is the fact that the average trader doesn’t understand what drives the markets either! Many traders are quite happy to blindly follow mechanical systems, based on mathematical formulas that have been ba ...