CVA: Default Probability ain`t matter?

... In order to further illustrate things we could use a simple analogy that should make the reader familiar with this matter. Let’s say, for example, that we are into the business of promoting boxers. We have a boxer in our book, called Max, who is fighting soon with another boxer. It so happens that b ...

... In order to further illustrate things we could use a simple analogy that should make the reader familiar with this matter. Let’s say, for example, that we are into the business of promoting boxers. We have a boxer in our book, called Max, who is fighting soon with another boxer. It so happens that b ...

capital markets players survey 2013

... Table 5: Total Assets in the Ugandan and Kenyan Capital Markets .................................................... 16 Table 6: Total Balance Sheet Assets by Licence Category in Uganda and Kenya .............................. 17 Table 7: Licence Category of Market Players with Agents .............. ...

... Table 5: Total Assets in the Ugandan and Kenyan Capital Markets .................................................... 16 Table 6: Total Balance Sheet Assets by Licence Category in Uganda and Kenya .............................. 17 Table 7: Licence Category of Market Players with Agents .............. ...

Institutional Investors and Stock Market Liquidity

... institutional holdings were more pronounced for NASDAQ stocks than for NYSE stocks. 3.1. Trends in Stock Ownership: All Stocks We begin by partitioning US equities into ten equal-capitalization deciles (hereafter, equal-cap deciles). Specifically, for each quarter during the period 1980 to 2010, we ...

... institutional holdings were more pronounced for NASDAQ stocks than for NYSE stocks. 3.1. Trends in Stock Ownership: All Stocks We begin by partitioning US equities into ten equal-capitalization deciles (hereafter, equal-cap deciles). Specifically, for each quarter during the period 1980 to 2010, we ...

Firms are

... Cartel theory: explicit collusion A Cartel is a group of firms that act together to coordinate output decisions and control prices. In other words, act like a monopoly. Conditions needed to establish and maintain a Cartel: 1) Large barriers to entry and few good substitutes …to prevent other seller ...

... Cartel theory: explicit collusion A Cartel is a group of firms that act together to coordinate output decisions and control prices. In other words, act like a monopoly. Conditions needed to establish and maintain a Cartel: 1) Large barriers to entry and few good substitutes …to prevent other seller ...

Decimals and Liquidity: A study of the NYSE

... regional stock exchanges posting quotes simultaneously in those stocks. In short, BBOs are generated by the specialist and public limit orders originating both in the primary market and in the regional stock exchanges, which dictates which exchange at any time has the BBO quotes. The fraction of tim ...

... regional stock exchanges posting quotes simultaneously in those stocks. In short, BBOs are generated by the specialist and public limit orders originating both in the primary market and in the regional stock exchanges, which dictates which exchange at any time has the BBO quotes. The fraction of tim ...

Determination of forward and futures prices

... ijSell for more than bought Receive divsyz j z P&L=$500ä jj H100 - 120L +1 zz = -$500ä 19 = -$9500 k ...

... ijSell for more than bought Receive divsyz j z P&L=$500ä jj H100 - 120L +1 zz = -$500ä 19 = -$9500 k ...

The Capital Asset Pricing model is based on the relationship

... return as a linear function of the S&P 500 returns. Write down the estimated model. 1. Calculate the coefficient of determination, r2 of the regression, and correlation coefficient r between XOM and S&P returns. Explain briefly what they mean. 2. Can you say with confidence (α =.05) that the populat ...

... return as a linear function of the S&P 500 returns. Write down the estimated model. 1. Calculate the coefficient of determination, r2 of the regression, and correlation coefficient r between XOM and S&P returns. Explain briefly what they mean. 2. Can you say with confidence (α =.05) that the populat ...

to Official Notice - The Stock Exchange of Mauritius

... (ii) the listing of up to 425,342,317 ordinary shares of BLL on the Official Market of the Stock Exchange of Mauritius Ltd following the above amalgamation, which will involve the migration of BLL from the DEM to the Official Market and consequently, the withdrawal of BLL from the DEM. 2. Suspension ...

... (ii) the listing of up to 425,342,317 ordinary shares of BLL on the Official Market of the Stock Exchange of Mauritius Ltd following the above amalgamation, which will involve the migration of BLL from the DEM to the Official Market and consequently, the withdrawal of BLL from the DEM. 2. Suspension ...

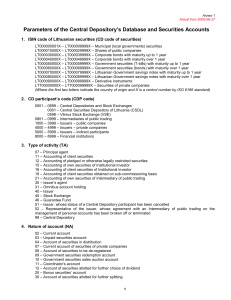

1. ISIN code of Lithuanian securities (CD code of securities)

... 015 – Stock exchange securities transactions with a postponed settlement day (T+x) 016 – Public sale of a block of state-owned shares 017 – Public sale of a block of non-state-owned shares 018 – Execution of a voluntary tender offer carrying settlement in cash 019 – Execution of a competitive tender ...

... 015 – Stock exchange securities transactions with a postponed settlement day (T+x) 016 – Public sale of a block of state-owned shares 017 – Public sale of a block of non-state-owned shares 018 – Execution of a voluntary tender offer carrying settlement in cash 019 – Execution of a competitive tender ...

Option Valuation

... If the two positions are worth the same at the end, they must cost the same at the beginning This leads to the put-call parity condition S + P = C + PV(E) If this condition does not hold, there is an arbitrage opportunity Buy the “low” side and sell the “high” side You can also use this ...

... If the two positions are worth the same at the end, they must cost the same at the beginning This leads to the put-call parity condition S + P = C + PV(E) If this condition does not hold, there is an arbitrage opportunity Buy the “low” side and sell the “high” side You can also use this ...

an empirical determinant of equity share price of some quoted

... about determinants of share prices and the possible impact they incited. These factors could be controllable (within the firm) or uncontrollable (outside the influence of the firm). Dividend, earning per share, share price in previous year for example, are internal while government policy, interest ...

... about determinants of share prices and the possible impact they incited. These factors could be controllable (within the firm) or uncontrollable (outside the influence of the firm). Dividend, earning per share, share price in previous year for example, are internal while government policy, interest ...

2010 Flash Crash

The May 6, 2010, Flash Crash also known as The Crash of 2:45, the 2010 Flash Crash or simply the Flash Crash, was a United States trillion-dollar stock market crash, which started at 2:32 and lasted for approximately 36 minutes. Stock indexes, such as the S&P 500, Dow Jones Industrial Average and Nasdaq 100, collapsed and rebounded very rapidly.The Dow Jones Industrial Average had its biggest intraday point drop (from the opening) up to that point, plunging 998.5 points (about 9%), most within minutes, only to recover a large part of the loss. It was also the second-largest intraday point swing (difference between intraday high and intraday low) up to that point, at 1,010.14 points. The prices of stocks, stock index futures, options and ETFs were volatile, thus trading volume spiked. A CFTC 2014 report described it as one of the most turbulent periods in the history of financial markets.On April 21, 2015, nearly five years after the incident, the U.S. Department of Justice laid ""22 criminal counts, including fraud and market manipulation"" against Navinder Singh Sarao, a trader. Among the charges included was the use of spoofing algorithms; just prior to the Flash Crash, he placed thousands of E-mini S&P 500 stock index futures contracts which he planned on canceling later. These orders amounting to about ""$200 million worth of bets that the market would fall"" were ""replaced or modified 19,000 times"" before they were canceled. Spoofing, layering and front-running are now banned.The Commodity Futures Trading Commission (CFTC) investigation concluded that Sarao ""was at least significantly responsible for the order imbalances"" in the derivatives market which affected stock markets and exacerbated the flash crash. Sarao began his alleged market manipulation in 2009 with commercially available trading software whose code he modified ""so he could rapidly place and cancel orders automatically."" Traders Magazine journalist, John Bates, argued that blaming a 36-year-old small-time trader who worked from his parents' modest stucco house in suburban west London for sparking a trillion-dollar stock market crash is a little bit like blaming lightning for starting a fire"" and that the investigation was lengthened because regulators used ""bicycles to try and catch Ferraris."" Furthermore, he concluded that by April 2015, traders can still manipulate and impact markets in spite of regulators and banks' new, improved monitoring of automated trade systems.As recently as May 2014, a CFTC report concluded that high-frequency traders ""did not cause the Flash Crash, but contributed to it by demanding immediacy ahead of other market participants.""Recent research shows that Flash Crashes are not isolated occurrences, but have occurred quite often over the past century. For instance, Irene Aldridge, the author of High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems, 2nd ed., Wiley & Sons, shows that Flash Crashes have been frequent and their causes predictable in market microstructure analysis.