Course Home. - Primary Residential Mortgage

... for Successful Mortgage Professionals. PRMI has a simple, but powerful plan that is guided by a clear and focused vision to find the best and most enterprising mortgage professionals in the industry, and provide them an unmatched opportunity to grow themselves and their business. As a PRMI mortgage ...

... for Successful Mortgage Professionals. PRMI has a simple, but powerful plan that is guided by a clear and focused vision to find the best and most enterprising mortgage professionals in the industry, and provide them an unmatched opportunity to grow themselves and their business. As a PRMI mortgage ...

Expected Return Standard Deviation

... CAPM Terminologies: Systematic and Unsystematic risk In the development of portfolio theory Markowitz (1958) defined the variance of the rate of return as the appropriate measure of risk. However this can be sub-divided into two general types of risk: systematic and unsystematic risk. William Sh ...

... CAPM Terminologies: Systematic and Unsystematic risk In the development of portfolio theory Markowitz (1958) defined the variance of the rate of return as the appropriate measure of risk. However this can be sub-divided into two general types of risk: systematic and unsystematic risk. William Sh ...

model answers and marking scheme

... 1. Systematic or Market risk - is associated with systematic factors. The risk can be hedged but cannot be diversified away; it is undiversifiable. All investors assume this risk whenever assets owned or claims issued can change following broad economic factors e.g. interest rates and foreign exchan ...

... 1. Systematic or Market risk - is associated with systematic factors. The risk can be hedged but cannot be diversified away; it is undiversifiable. All investors assume this risk whenever assets owned or claims issued can change following broad economic factors e.g. interest rates and foreign exchan ...

statement on subprime mortgage lending

... savings and loan holding companies and their subsidiaries, and credit unions. Recognizing that the interagency Subprime Statement does not apply to subprime loan originations of independent mortgage lenders and mortgage brokers, on June 29, 2007 the Conference of State Bank Supervisors (CSBS), the A ...

... savings and loan holding companies and their subsidiaries, and credit unions. Recognizing that the interagency Subprime Statement does not apply to subprime loan originations of independent mortgage lenders and mortgage brokers, on June 29, 2007 the Conference of State Bank Supervisors (CSBS), the A ...

Chapter 13

... An American depository receipt (ADR) is a marketable receipt showing ownership of a ...

... An American depository receipt (ADR) is a marketable receipt showing ownership of a ...

IV - LSE

... Tax and regulatory reforms – There were three principal reforms in the 1980s which helped to spur the development of the subprime lending market. The Depository Institutions Deregulation and Monetary Control Act of 1980 pre-empted state level limitations on interest rates. As a result of this legis ...

... Tax and regulatory reforms – There were three principal reforms in the 1980s which helped to spur the development of the subprime lending market. The Depository Institutions Deregulation and Monetary Control Act of 1980 pre-empted state level limitations on interest rates. As a result of this legis ...

Demystifying the Federal Home Loan Banks:

... These programs were begun to help community lenders retain more of the value of their mortgage originations. Lenders, particularly smaller lenders who know their customers better than any GSE can, have traditionally originated very high-quality fixed-rate mortgages. However, they often were not able ...

... These programs were begun to help community lenders retain more of the value of their mortgage originations. Lenders, particularly smaller lenders who know their customers better than any GSE can, have traditionally originated very high-quality fixed-rate mortgages. However, they often were not able ...

What is a Systemically Important Financial Institution?

... a principal components analysis becomes concentrated in a single factor. A modification of this approach by Reyngold, Shnyra, and Stein (2013) denoted Credit Absorption Ratio (CAR) extends AR to default risk data. And Carciente, Kenett, Avakia, Stanley, and Havlin (2015) undertake systemic stress te ...

... a principal components analysis becomes concentrated in a single factor. A modification of this approach by Reyngold, Shnyra, and Stein (2013) denoted Credit Absorption Ratio (CAR) extends AR to default risk data. And Carciente, Kenett, Avakia, Stanley, and Havlin (2015) undertake systemic stress te ...

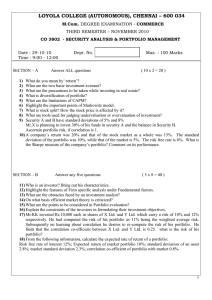

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI – 600 034

... What is stock split? How the stock price is affected by it? What are tools used for judging undervaluation or overvaluation of investment? Security A and B have standard deviations of 5% and 8% Mr.X is planning to invest 30% of his funds in security A and the balance in Security B. Ascertain portfol ...

... What is stock split? How the stock price is affected by it? What are tools used for judging undervaluation or overvaluation of investment? Security A and B have standard deviations of 5% and 8% Mr.X is planning to invest 30% of his funds in security A and the balance in Security B. Ascertain portfol ...

Fronting Programs: Benefits and Considerations

... parties. Certain property-casualty coverages may be provided by a surplus lines insurer. Surplus lines insurers do not generally participate in state guaranty funds, and insureds are therefore not protected by such funds. Insurance coverage is account specific and is governed by actual policy langua ...

... parties. Certain property-casualty coverages may be provided by a surplus lines insurer. Surplus lines insurers do not generally participate in state guaranty funds, and insureds are therefore not protected by such funds. Insurance coverage is account specific and is governed by actual policy langua ...

Grattan Institute submission - Rate of return guidelines issues paper

... Grattan Institute’s research is informed by an analytical approach to the evidence. In our Report, we concluded that the monopoly electricity distribution businesses have been making unduly high profits, given the relatively low risks they face. In our view, the risk/return balance is central to the ...

... Grattan Institute’s research is informed by an analytical approach to the evidence. In our Report, we concluded that the monopoly electricity distribution businesses have been making unduly high profits, given the relatively low risks they face. In our view, the risk/return balance is central to the ...

Seeing the positive - The Business Times

... becoming the norm, we have a situation where investors’ returns will be increasingly driven by their tolerance for volatility and risk. In other words, investors will need to reduce their return expectations or they will need to take more risk to generate the same level of yield/returns that they ha ...

... becoming the norm, we have a situation where investors’ returns will be increasingly driven by their tolerance for volatility and risk. In other words, investors will need to reduce their return expectations or they will need to take more risk to generate the same level of yield/returns that they ha ...

What Agencies Can Expect Accessing Bank Capital in

... Only high quality, well-prepared, and creditBankers prefer to make loans to more tradiworthy individuals and businesses will find tional borrowers with tangible assets. Thus, credit available in this crunch. in difficult credit environments, working Throughout my career, I have observed a with a len ...

... Only high quality, well-prepared, and creditBankers prefer to make loans to more tradiworthy individuals and businesses will find tional borrowers with tangible assets. Thus, credit available in this crunch. in difficult credit environments, working Throughout my career, I have observed a with a len ...

The Regulatory Framework... A Change of Direction Bucharest – 12

... investors and other stakeholders because they do not provide a basis on which exposures to risk can be quantified, aggregated and reported as they accumulate • The Basel Committee and Financial Stability Board have conducted a number of studies of the regulatory framework and their conclusion is tha ...

... investors and other stakeholders because they do not provide a basis on which exposures to risk can be quantified, aggregated and reported as they accumulate • The Basel Committee and Financial Stability Board have conducted a number of studies of the regulatory framework and their conclusion is tha ...

Click to Add Title - BusinessinAfrica Events

... while creating investment and risk dispersion opportunities for insurance companies ...

... while creating investment and risk dispersion opportunities for insurance companies ...

Cost of borrowing and credit risk management

... It is clear therefore that lending will become ‘scientifically’ priced in the future, which should be fairer all round. The pricing will depend to a large extent on three key factors for each institution, namely the loss given default (LGD), the probability of default (PD) and the default correlatio ...

... It is clear therefore that lending will become ‘scientifically’ priced in the future, which should be fairer all round. The pricing will depend to a large extent on three key factors for each institution, namely the loss given default (LGD), the probability of default (PD) and the default correlatio ...

The State of Financial Guaranty Insurance

... interest rates. • Asset-backed securities on mortgages are created also known as mortgage backed securities (MBSs). At first with normal mortgages. • As housing boom continues after 2002, new assetbacked securities are created, but these new securities included sub-prime mortgages. • Some of these s ...

... interest rates. • Asset-backed securities on mortgages are created also known as mortgage backed securities (MBSs). At first with normal mortgages. • As housing boom continues after 2002, new assetbacked securities are created, but these new securities included sub-prime mortgages. • Some of these s ...

- ePrints Soton

... independent of the covariates. Most products show a distinctive ‘spike’ in the hazard curves after a certain time period. This may reflect the fact that customers are most likely to default at the end of their introductory fixed rate period, when they transfer onto a less favourable rate of interest ...

... independent of the covariates. Most products show a distinctive ‘spike’ in the hazard curves after a certain time period. This may reflect the fact that customers are most likely to default at the end of their introductory fixed rate period, when they transfer onto a less favourable rate of interest ...

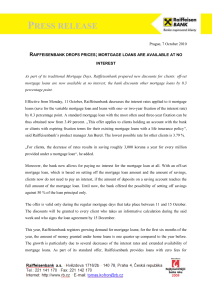

Praha, 2 - Raiffeisenbank

... mortgage loans are now available at no interest; the bank discounts other mortgage loans by 0.3 percentage point. Effective from Monday, 11 October, Raiffeisenbank decreases the interest rates applied to it mortgage loans (save for the variable mortgage loan and loans with one- or two-year fixation ...

... mortgage loans are now available at no interest; the bank discounts other mortgage loans by 0.3 percentage point. Effective from Monday, 11 October, Raiffeisenbank decreases the interest rates applied to it mortgage loans (save for the variable mortgage loan and loans with one- or two-year fixation ...

Lecture 11: Real Estate

... • SWW conclude that the biggest single factor in increase in personal bankruptcies in US has been growth of credit card debt.Average debtor in bankruptcy in 1997 had nine months’ income in credit card debt. – Credit card debt continues to be extended after initial application – Debt is incurred a li ...

... • SWW conclude that the biggest single factor in increase in personal bankruptcies in US has been growth of credit card debt.Average debtor in bankruptcy in 1997 had nine months’ income in credit card debt. – Credit card debt continues to be extended after initial application – Debt is incurred a li ...

U.S. Annuity Market Dynamics and Regulatory Requirements

... Foster an effective level of ERM at all insurers Provide a group-level perspective on risk and capital ...

... Foster an effective level of ERM at all insurers Provide a group-level perspective on risk and capital ...

Expected Return Standard Deviation Increasing Utility

... Investor’s preferences toward the exp. return and risk may be expressed by the utility function that is higher for higher exp. returns and lower for higher risks. More risk-averse investors will apply greater penalties for risk. The greater the risk, the larger the penalty. We can formalize the risk ...

... Investor’s preferences toward the exp. return and risk may be expressed by the utility function that is higher for higher exp. returns and lower for higher risks. More risk-averse investors will apply greater penalties for risk. The greater the risk, the larger the penalty. We can formalize the risk ...

A New View of Mortgages (and life)

... – Developer lets option expire without purchasing land – Farmer keeps the payment $X. ...

... – Developer lets option expire without purchasing land – Farmer keeps the payment $X. ...

Payment Mortgages

... loans that it will purchase from banks and other lenders. The action … will encourage those banks to extend home mortgages to individuals whose credit is generally not good enough to qualify for conventional loans. Fannie Mae officials say they hope to make it a nationwide program by next spring. Fa ...

... loans that it will purchase from banks and other lenders. The action … will encourage those banks to extend home mortgages to individuals whose credit is generally not good enough to qualify for conventional loans. Fannie Mae officials say they hope to make it a nationwide program by next spring. Fa ...