Contents and summary observations

... framework agreement with the United States. The Malaysian authorities maintain that existing as well as planned bilateral and regional free-trade agreements are consistent with, and complement, the multilateral framework for trade negotiations. Although, negotiation of a number of ASEAN-wide as well ...

... framework agreement with the United States. The Malaysian authorities maintain that existing as well as planned bilateral and regional free-trade agreements are consistent with, and complement, the multilateral framework for trade negotiations. Although, negotiation of a number of ASEAN-wide as well ...

Presentation - Sharjah Chamber of Commerce and Industry

... Agreement, the COMCEC (Standing Committee for Economic and Commercial Cooperation of the Organization of Islamic Cooperation) - the platform for Islamic world (UMMAH) cooperation in economic & commercial aspects.) established the TNC (trade negotiating committee) in 2003. The Member States of the TN ...

... Agreement, the COMCEC (Standing Committee for Economic and Commercial Cooperation of the Organization of Islamic Cooperation) - the platform for Islamic world (UMMAH) cooperation in economic & commercial aspects.) established the TNC (trade negotiating committee) in 2003. The Member States of the TN ...

What should a well-designed and well

... carefully. Decisions taken at the appraisal stage affect the whole lifecycle of new policies, programmes and projects. Similarly, the proper evaluation of previous initiatives is essential in avoiding past mistakes and to enable us to learn from experience.” “The first step is to carry out an overvi ...

... carefully. Decisions taken at the appraisal stage affect the whole lifecycle of new policies, programmes and projects. Similarly, the proper evaluation of previous initiatives is essential in avoiding past mistakes and to enable us to learn from experience.” “The first step is to carry out an overvi ...

Cohesion Policy after 2013

... R&D subsidies should not be the prior areas for the Cohesion Policies within the lagging regions Direct aid to the firms is at least problematic. A reduction of the upper limit of subsidies would be an ...

... R&D subsidies should not be the prior areas for the Cohesion Policies within the lagging regions Direct aid to the firms is at least problematic. A reduction of the upper limit of subsidies would be an ...

Chapter Twenty - Cengage Learning

... What financial goals do you want to achieve? How much money will you need, and when? What will you use the money for? Is it reasonable to assume that you can obtain the amount of money you will need to meet your investment goals? Do you expect your personal situation to change in a way that will aff ...

... What financial goals do you want to achieve? How much money will you need, and when? What will you use the money for? Is it reasonable to assume that you can obtain the amount of money you will need to meet your investment goals? Do you expect your personal situation to change in a way that will aff ...

Special_Economix_Zone_Lodz

... Special Economic Zone (SEZ) is an area designated by the Polish Government, where business activity can operate on preferential conditions (State Aid). The State Aid in SEZs is granted in a form of a total exemption from Corporate Income Tax (CIT) from the activity conducted within the Zone’s area. ...

... Special Economic Zone (SEZ) is an area designated by the Polish Government, where business activity can operate on preferential conditions (State Aid). The State Aid in SEZs is granted in a form of a total exemption from Corporate Income Tax (CIT) from the activity conducted within the Zone’s area. ...

The Fed`s reinvestment policy

... ‘test the water’ in a bid to avoid a repeat of the 2013 Taper Tantrum. They’ve learnt that often their words speak louder than actions, but in this instance any action is some way off. The comments are also a release valve for dollar strength, as too strong a currency can cause problems for the Fed ...

... ‘test the water’ in a bid to avoid a repeat of the 2013 Taper Tantrum. They’ve learnt that often their words speak louder than actions, but in this instance any action is some way off. The comments are also a release valve for dollar strength, as too strong a currency can cause problems for the Fed ...

investment incentives

... course of action (or inaction) might not be more appropriate. This paper attempts to provide a basis for such a broader understanding and also looks at the consequential issue of national treatment with respect to investment incentives. What is an investment incentive? Typically, only a small propor ...

... course of action (or inaction) might not be more appropriate. This paper attempts to provide a basis for such a broader understanding and also looks at the consequential issue of national treatment with respect to investment incentives. What is an investment incentive? Typically, only a small propor ...

Primary Market Liquidity Vs. Secondary Market Liquidity

... The products discussed in this document are issued by Boost Issuer PLC (the “Issuer”) under a Prospectus approved by the Central Bank of Ireland as having been drawn up in accordance with the Directive 2003/71/EC (the “Prospectus”). The Prospectus has been passported from Ireland into the United Kin ...

... The products discussed in this document are issued by Boost Issuer PLC (the “Issuer”) under a Prospectus approved by the Central Bank of Ireland as having been drawn up in accordance with the Directive 2003/71/EC (the “Prospectus”). The Prospectus has been passported from Ireland into the United Kin ...

Beyond Libor: The Evolution of `Risk-Free` Benchmarks

... This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment produ ...

... This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment produ ...

6% Marginal Cost of Capital

... This commonly used model takes into account the risk differential between a particular investor’s (say, company) stock and that of the stock of private investors/companies in general, as well as the differential between the investor’s stock and government securities. The former differential is measu ...

... This commonly used model takes into account the risk differential between a particular investor’s (say, company) stock and that of the stock of private investors/companies in general, as well as the differential between the investor’s stock and government securities. The former differential is measu ...

Lecture 2

... equity confers the right to share in profits distributed through dividend payments upon the decision of the Board of Directors ...

... equity confers the right to share in profits distributed through dividend payments upon the decision of the Board of Directors ...

To Buy or Not to Buy? – That is the question

... Debt to 50% LVR drawn day one, anticipate obtaining facility of 55% to provide a buffer ...

... Debt to 50% LVR drawn day one, anticipate obtaining facility of 55% to provide a buffer ...

14 App 1 Appendix 14(1): Interpretation

... (ii) a firm falling within IPRU-INV rule 14.1.1(1); (b) is subsidiary undertakings are either exclusively or mainly: (i) credit institutions;, (ii) investment firms; (iii) broad scope firms or undertakings carrying on activities which (if they were firms doing those activities in the United Kingdom) ...

... (ii) a firm falling within IPRU-INV rule 14.1.1(1); (b) is subsidiary undertakings are either exclusively or mainly: (i) credit institutions;, (ii) investment firms; (iii) broad scope firms or undertakings carrying on activities which (if they were firms doing those activities in the United Kingdom) ...

FTA Morningstar 90 10 FS 3-31-17_Layout 1

... of the company. Among the factors considered are the cash flow generated by the company, the asset base employed to generate that cash flow, management’s stewardship of investor capital and risk/return tradeoff. The entire process is focused on identifying companies whose true value is not being ref ...

... of the company. Among the factors considered are the cash flow generated by the company, the asset base employed to generate that cash flow, management’s stewardship of investor capital and risk/return tradeoff. The entire process is focused on identifying companies whose true value is not being ref ...

Development Benefits of PACER Plus for the Forum Island

... Objective: Reduce barriers to trade in services among the Parties; increase the participation of the FICs in regional/ international services trade. Main negotiating issues: Special and differential treatment of the FICs ; Scheduling Approach; Scope of the right to regulate; Technical assistance and ...

... Objective: Reduce barriers to trade in services among the Parties; increase the participation of the FICs in regional/ international services trade. Main negotiating issues: Special and differential treatment of the FICs ; Scheduling Approach; Scope of the right to regulate; Technical assistance and ...

How to invest offshore?

... should not be relied upon. This communication is provided for general information only and for distribution only in South Africa. It is not an invitation to make an investment nor does it constitute an offer for sale. The full documentation that should be considered before making an investment, incl ...

... should not be relied upon. This communication is provided for general information only and for distribution only in South Africa. It is not an invitation to make an investment nor does it constitute an offer for sale. The full documentation that should be considered before making an investment, incl ...

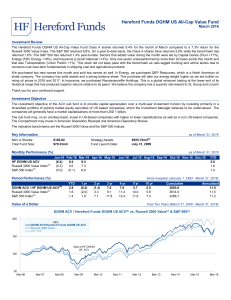

Click to download DGHM ACV March 2016

... guarantee that its investment objectives will be achieved. Potential investors shall be aware that the value of investments can fall as well as rise and that they may not get back the full amount invested. Past performance is no guide to future performance. The information provided in this document ...

... guarantee that its investment objectives will be achieved. Potential investors shall be aware that the value of investments can fall as well as rise and that they may not get back the full amount invested. Past performance is no guide to future performance. The information provided in this document ...

Edison QuickView Template - Edison Investment Research

... and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securitie ...

... and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is registered as an investment adviser with the Securitie ...

Appendix A University of Virginia Investment Management Company

... estate funds, the 7.5% limitation applies to the net amount committed to active funds (calculated as the total cost basis of current investments plus total unfunded commitments, if any). For purposes of this limitation, separate funds managed by an investment company or business group are aggregated ...

... estate funds, the 7.5% limitation applies to the net amount committed to active funds (calculated as the total cost basis of current investments plus total unfunded commitments, if any). For purposes of this limitation, separate funds managed by an investment company or business group are aggregated ...

05 HF DGHM ACV MAY 2011

... (e) Share Class A is German tax registered from 27/5/10, registered with the AFM for public distribution in the Netherlands, and has been granted Reporting Status by HMRC as of October 1st, 2010 (f) Share Class D is German tax registered from 1/10/10 and registered with the AFM for public distributi ...

... (e) Share Class A is German tax registered from 27/5/10, registered with the AFM for public distribution in the Netherlands, and has been granted Reporting Status by HMRC as of October 1st, 2010 (f) Share Class D is German tax registered from 1/10/10 and registered with the AFM for public distributi ...