O T Q 2014 Q

... As Sir John Templeton indicated in the quote at the beginning of this letter, bull markets die of euphoria. They don’t die of old age. Clients fretting about how well the market has done is certainly not an indication of euphoria. In fact, from a contrarian perspective, clients’ disbelief suggest th ...

... As Sir John Templeton indicated in the quote at the beginning of this letter, bull markets die of euphoria. They don’t die of old age. Clients fretting about how well the market has done is certainly not an indication of euphoria. In fact, from a contrarian perspective, clients’ disbelief suggest th ...

solve(A*m^NR*(m^N-1)/(m

... We want to understand the relationships between the mortgage payment rate of a fixed rate mortgage, the principal (the amount borrowed), the annual interest rate, and the period of the loan. We are going to assume (as is usually the case in the U. S.) that payments are made monthly, even though the ...

... We want to understand the relationships between the mortgage payment rate of a fixed rate mortgage, the principal (the amount borrowed), the annual interest rate, and the period of the loan. We are going to assume (as is usually the case in the U. S.) that payments are made monthly, even though the ...

market process - College of Business and Economics

... • “The problem which we pretend to solve is how the spontaneous interaction of a number of people, each possessing only bits of knowledge, brings about a state of affairs in which product prices correspond to costs, etc., and which could be brought about by deliberate direction only by somebody who ...

... • “The problem which we pretend to solve is how the spontaneous interaction of a number of people, each possessing only bits of knowledge, brings about a state of affairs in which product prices correspond to costs, etc., and which could be brought about by deliberate direction only by somebody who ...

LCwasR47_en.pdf

... States is at a different point in the economic cycle compared to anywhere else in the developed and developing world. However, it appears as if there is no such decoupling o f world financial markets. On the contrary, on the heels o f the latest events, Wall Street seems even more central to the wo ...

... States is at a different point in the economic cycle compared to anywhere else in the developed and developing world. However, it appears as if there is no such decoupling o f world financial markets. On the contrary, on the heels o f the latest events, Wall Street seems even more central to the wo ...

Secured Transactions: The Power of Collateral

... What prevents the use of movable property as collateral in developing and transition countries? Three obstacles stand out: • The creation of security interests is difficult, expensive, and uncertain. • The perfection of security interests— the public demonstration of their existence and the establis ...

... What prevents the use of movable property as collateral in developing and transition countries? Three obstacles stand out: • The creation of security interests is difficult, expensive, and uncertain. • The perfection of security interests— the public demonstration of their existence and the establis ...

Mortgage Credit & Subprime Lending: Implications of a

... • Monetary Policy: Irresponsible monetary policy followed by the FOMC in the early part of the decade, which poured gasoline on a real estate market that was already overheating and would run five more years in manic mode. www.institutionalriskanalytics.com ...

... • Monetary Policy: Irresponsible monetary policy followed by the FOMC in the early part of the decade, which poured gasoline on a real estate market that was already overheating and would run five more years in manic mode. www.institutionalriskanalytics.com ...

Session 33- Market Timing Indicators II

... period is negatively correlated with the level of rates at the end of the prior year; if rates were high (low), they were more likely to decrease (increase). Second, for every 1% increase in the level of current rates, the expected drop in interest rates in the next period increases by 0.1456%. ...

... period is negatively correlated with the level of rates at the end of the prior year; if rates were high (low), they were more likely to decrease (increase). Second, for every 1% increase in the level of current rates, the expected drop in interest rates in the next period increases by 0.1456%. ...

This PDF is a selection from a published volume from... National Bureau of Economic Research

... payments specified by the average contract in the class, and (b) the average credit quality of the class. Stock versus flows. The following suggestions apply diVerently whether the data collected are stocks or flows, and collection of information about flows is preferable if possible. If stocks are ...

... payments specified by the average contract in the class, and (b) the average credit quality of the class. Stock versus flows. The following suggestions apply diVerently whether the data collected are stocks or flows, and collection of information about flows is preferable if possible. If stocks are ...

"Why Interest Rates Will Rise," Funds Society

... cause some erosion in value. The effect will depend on what happens to the credit spread – the interest paid to investors for assuming credit risk. If the credit spread narrows, the overall effect may be slight. If it widens, the market could be hit with a double whammy. Historically, the credit spr ...

... cause some erosion in value. The effect will depend on what happens to the credit spread – the interest paid to investors for assuming credit risk. If the credit spread narrows, the overall effect may be slight. If it widens, the market could be hit with a double whammy. Historically, the credit spr ...

1 Solutions to End-of-Chapter Problems in

... expected to be higher and this causes the current IS schedule to shift to the left. The net effect on the IS curve is ambiguous. (b) Expected future taxes will be lower causing the current IS schedule to shift to the right. To keep future Y constant, the central bank will have to reduce the future m ...

... expected to be higher and this causes the current IS schedule to shift to the left. The net effect on the IS curve is ambiguous. (b) Expected future taxes will be lower causing the current IS schedule to shift to the right. To keep future Y constant, the central bank will have to reduce the future m ...

It is not appropriate to discount the cash flows of a bond by the yield

... strategy that produces an interest rate risk exposure if the expected return from the investment strategy or expected cost from borrowing strategy is sufficient to compensate for the additional interest rate risk exposure. The term structure theories discussed in the text (pages 111-116) are predica ...

... strategy that produces an interest rate risk exposure if the expected return from the investment strategy or expected cost from borrowing strategy is sufficient to compensate for the additional interest rate risk exposure. The term structure theories discussed in the text (pages 111-116) are predica ...

Document

... The analysis of interest rate behavior (i.e., changes in the market equilibrium interest rate) needs to explore why the curves shift in or ...

... The analysis of interest rate behavior (i.e., changes in the market equilibrium interest rate) needs to explore why the curves shift in or ...

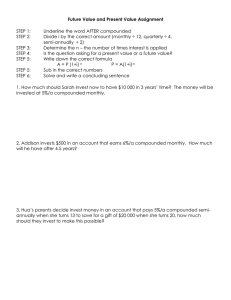

Future Value and Present Value Assignment

... 3. Hua’s parents decide invest money in an account that pays 5%/a compounded semiannually when she turns 13 to save for a gift of $20 000 when she turns 20, how much should they invest to make this possible? ...

... 3. Hua’s parents decide invest money in an account that pays 5%/a compounded semiannually when she turns 13 to save for a gift of $20 000 when she turns 20, how much should they invest to make this possible? ...

Ch#18 Bank Management

... can be purchased or sold on a specified future settlement date. • So Futures are Contracts that call for the future sale or purchase of specific types of financial assets at a fixed price to profit or hedge against loss • For example, there are future contracts available on CDs. When banks lock in t ...

... can be purchased or sold on a specified future settlement date. • So Futures are Contracts that call for the future sale or purchase of specific types of financial assets at a fixed price to profit or hedge against loss • For example, there are future contracts available on CDs. When banks lock in t ...

Chapter 14 - Capital Markets

... Equilibrium could only occur if the price increase equaled the real rate of interest. ...

... Equilibrium could only occur if the price increase equaled the real rate of interest. ...

Turkey’s Experience with Macroprudential Policy Central Bank of Turkey Hakan Kara

... Historically, sharp capital flow reversals (sudden stops) in Turkey are associated with large output losses. Net Capital Flows / GDP ...

... Historically, sharp capital flow reversals (sudden stops) in Turkey are associated with large output losses. Net Capital Flows / GDP ...

What Agencies Can Expect Accessing Bank Capital in

... company data (production reports or experi- will seek to borrow the least amount of ence reports) from your top five carriers to money for the shortest reasonable period. confirm the data. This will reduce risk, reduce cumulative 4. Do you use the capabilities of your agency interest paid, and keep ...

... company data (production reports or experi- will seek to borrow the least amount of ence reports) from your top five carriers to money for the shortest reasonable period. confirm the data. This will reduce risk, reduce cumulative 4. Do you use the capabilities of your agency interest paid, and keep ...

Nicolas Magud Carmen M Reinhart Esteban R Vesperoni 24

... currency. As for creditors, the increase in banks’ leverage – loan-to-deposit ratios – that large capital inflows usually bring about can place incentives to lend directly in foreign currency, as this would allow banks to avoid currency mismatches in their balance sheets. As for debtors – in credibl ...

... currency. As for creditors, the increase in banks’ leverage – loan-to-deposit ratios – that large capital inflows usually bring about can place incentives to lend directly in foreign currency, as this would allow banks to avoid currency mismatches in their balance sheets. As for debtors – in credibl ...

Floating rate Term Deposits

... benchmark. When interest rate increases, the outflow on the housing loan will be higher, but so will the inflow from the floating rate deposit. Banks normally do not offer such products, as they do not have the technology to support them. The reason that floating rate of interest is now being offere ...

... benchmark. When interest rate increases, the outflow on the housing loan will be higher, but so will the inflow from the floating rate deposit. Banks normally do not offer such products, as they do not have the technology to support them. The reason that floating rate of interest is now being offere ...

Treasury Policy

... Council will utilize long-term variable interest rate borrowing facilities, such as the LGFA’s Cash Advance Debenture, that require interest payments only and that enables any amount of principal to be repaid or redrawn at call. The redraw facility will provide Council with access to liquidity when ...

... Council will utilize long-term variable interest rate borrowing facilities, such as the LGFA’s Cash Advance Debenture, that require interest payments only and that enables any amount of principal to be repaid or redrawn at call. The redraw facility will provide Council with access to liquidity when ...

CT Cengage PPT template

... for sale but no increase has been made in the available money. • With twice as much to buy for the same amount of money, the price of each unit of goods and services would drop to $50. • If the money supply was increased to $3 million, then each unit would be worth $150. ...

... for sale but no increase has been made in the available money. • With twice as much to buy for the same amount of money, the price of each unit of goods and services would drop to $50. • If the money supply was increased to $3 million, then each unit would be worth $150. ...

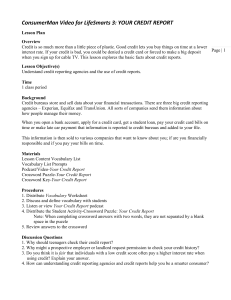

ConsumerMan Video for LifeSmarts 3: YOUR CREDIT REPORT

... Credit is so much more than a little piece of plastic. Good credit lets you buy things on time at a lower Page | 1 interest rate. If your credit is bad, you could be denied a credit card or forced to make a big deposit when you sign up for cable TV. This lesson explores the basic facts about credit ...

... Credit is so much more than a little piece of plastic. Good credit lets you buy things on time at a lower Page | 1 interest rate. If your credit is bad, you could be denied a credit card or forced to make a big deposit when you sign up for cable TV. This lesson explores the basic facts about credit ...

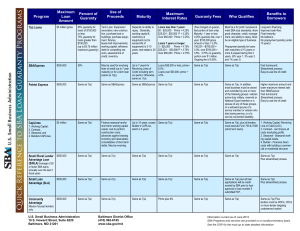

Program Maximum Loan Amount Percent of Guaranty Use of

... Same as 504 plus borrower must have been current on last 12 monthly payments. Can not refinance an existing federal government loan. ...

... Same as 504 plus borrower must have been current on last 12 monthly payments. Can not refinance an existing federal government loan. ...

INDIVIDUAL FINANCIAL STATEMENT

... Individual Credit. If a married applicant is applying for individual credit, complete this statement including all marital property and all individual property of the applicant, but do not include individual property of the non-applicant spouse. Include all liabilities of both spouses. Only the appl ...

... Individual Credit. If a married applicant is applying for individual credit, complete this statement including all marital property and all individual property of the applicant, but do not include individual property of the non-applicant spouse. Include all liabilities of both spouses. Only the appl ...

Credit rationing

Credit rationing refers to the situation where lenders limit the supply of additional credit to borrowers who demand funds, even if the latter are willing to pay higher interest rates. It is an example of market imperfection, or market failure, as the price mechanism fails to bring about equilibrium in the market. It should not be confused with cases where credit is simply ""too expensive"" for some borrowers, that is, situations where the interest rate is deemed too high. On the contrary, the borrower would like to acquire the funds at the current rates, and the imperfection refers to the absence of equilibrium in spite of willing borrowers. In other words, at the prevailing market interest rate, demand exceeds supply, but lenders are not willing to either loan more funds, or raise the interest rate charged, as they are already maximising profits.