credit risk management: the next great financial challenge

... Calibration: How close are actual vs. predicted defaults, both for the book overall and for individual credit grades? Consistency: How consistent are the results across the different scorecards? Robustness: How consistent are the results across Industries, over time and across the Bank ...

... Calibration: How close are actual vs. predicted defaults, both for the book overall and for individual credit grades? Consistency: How consistent are the results across the different scorecards? Robustness: How consistent are the results across Industries, over time and across the Bank ...

Savvy Investors` Credit Workbook

... Financing residential real estate If you are trying to decide whether to obtain a traditional 30-year amortizing mortgage versus using securities-based lending to finance your real estate purchase, consider which approach will put you further ahead in the long term. One of the key benefits of a secu ...

... Financing residential real estate If you are trying to decide whether to obtain a traditional 30-year amortizing mortgage versus using securities-based lending to finance your real estate purchase, consider which approach will put you further ahead in the long term. One of the key benefits of a secu ...

NBER WORKING PAPER SERIES HOUSEHOLD LEVERAGING AND DELEVERAGING Alejandro Justiniano Giorgio E. Primiceri

... driven by a shock to households’ taste for housing services. This modeling approach captures the idea that collateral values were the main independent cause of the changes in debt, and allows us to illustrate its implications, although it punts on the ultimate source of the observed swing in house p ...

... driven by a shock to households’ taste for housing services. This modeling approach captures the idea that collateral values were the main independent cause of the changes in debt, and allows us to illustrate its implications, although it punts on the ultimate source of the observed swing in house p ...

Intergrated Bank Corporation (IBC) is a medium

... seasoned (i.e., older than one year) floating rate mortgages jumps contractually to a higher spread. The initial teaser and future spreads passed through to bond holders – less the servicing fee – are set so that GNMA ARMs trade at par at issuance. Specifically, the currently, the teaser spread on ...

... seasoned (i.e., older than one year) floating rate mortgages jumps contractually to a higher spread. The initial teaser and future spreads passed through to bond holders – less the servicing fee – are set so that GNMA ARMs trade at par at issuance. Specifically, the currently, the teaser spread on ...

Working Papers - Federal Reserve Bank of Philadelphia

... theoretical aspects of this effect have also been previously overlooked. First, to the extent that banks rely on common filters (shared databases and uniform screening criteria) in assessing applications, the adverse selection can be theoretically mitigated. An immediate corollary is that the use of ...

... theoretical aspects of this effect have also been previously overlooked. First, to the extent that banks rely on common filters (shared databases and uniform screening criteria) in assessing applications, the adverse selection can be theoretically mitigated. An immediate corollary is that the use of ...

Chapter 2

... • for debt securities, risk associated with changes in interest rates; consists of price risk and reinvestment rate risk Price Risk • a change in market interest rates produces an opposite change in the value of investments Reinvestment Rate Risk • risk as to what interest rate will be when income a ...

... • for debt securities, risk associated with changes in interest rates; consists of price risk and reinvestment rate risk Price Risk • a change in market interest rates produces an opposite change in the value of investments Reinvestment Rate Risk • risk as to what interest rate will be when income a ...

Pinnacle Academ y

... shall pay to A Inc. 1 % over the ¥ Loan interest rate, which the later will have to pay as a result of currency swap whereas A Inc. will reimburse interest to B Inc. only to the extent of 9%. Assuming stability of exchange rate, determine the net gain or loss to each of the party due to currency swa ...

... shall pay to A Inc. 1 % over the ¥ Loan interest rate, which the later will have to pay as a result of currency swap whereas A Inc. will reimburse interest to B Inc. only to the extent of 9%. Assuming stability of exchange rate, determine the net gain or loss to each of the party due to currency swa ...

IS-LM Tutorial

... Income and credit history– to get mortgages to buy home. One of these developments was securitization, the process by which one makes loans and then sells them to an investment bank which in turn bundles them together into a variety of “mortgage-backed securities” and then sells them to a third fina ...

... Income and credit history– to get mortgages to buy home. One of these developments was securitization, the process by which one makes loans and then sells them to an investment bank which in turn bundles them together into a variety of “mortgage-backed securities” and then sells them to a third fina ...

Institute of Actuaries of India MARKING SCHEDULE October 2009 EXAMINATION

... a. According to the model, the short rate can take negative values, which is not realistic. b. However, the probability of negative rates occurring is quite low. c. Negative rates are more likely to occur for medium terms than for long or short. d. The yield curve slopes upwards. e. The standard dev ...

... a. According to the model, the short rate can take negative values, which is not realistic. b. However, the probability of negative rates occurring is quite low. c. Negative rates are more likely to occur for medium terms than for long or short. d. The yield curve slopes upwards. e. The standard dev ...

Private Information

... Moral hazard exists when one of the parties to an agreement has an incentive after the agreement is made to act in a manner that brings additional benefits to himself or herself at the expense of the other party. Adverse selection is the tendency for people to enter into agreements in which they can ...

... Moral hazard exists when one of the parties to an agreement has an incentive after the agreement is made to act in a manner that brings additional benefits to himself or herself at the expense of the other party. Adverse selection is the tendency for people to enter into agreements in which they can ...

Uncertainty and Risk

... Moral hazard exists when one of the parties to an agreement has an incentive after the agreement is made to act in a manner that brings additional benefits to himself or herself at the expense of the other party. Adverse selection is the tendency for people to enter into agreements in which they can ...

... Moral hazard exists when one of the parties to an agreement has an incentive after the agreement is made to act in a manner that brings additional benefits to himself or herself at the expense of the other party. Adverse selection is the tendency for people to enter into agreements in which they can ...

bam_513financial_mangement_final_exam

... ensure a market in which the price reflects the true value of the security. control the supply and demand for securities through price. allocate funds to the most productive uses. allow the price to be determined by supply and demand of securities. ...

... ensure a market in which the price reflects the true value of the security. control the supply and demand for securities through price. allocate funds to the most productive uses. allow the price to be determined by supply and demand of securities. ...

Presentation - Federal Reserve Bank of New York

... No more need to forecast reserve demand and adjust accordingly the supply Small adjustments of reserves via OMO, as in pre-crisis framework, would not impact the federal funds rate With abundant reserves, the IOER could be used to control the target rate Interest rate ...

... No more need to forecast reserve demand and adjust accordingly the supply Small adjustments of reserves via OMO, as in pre-crisis framework, would not impact the federal funds rate With abundant reserves, the IOER could be used to control the target rate Interest rate ...

Setting aside the debate on when the exact date of an interest rate

... Low absolute levels of interest actually significantly reduce the potential for future returns. One of the primary goals of a zero interest rate policy is to reduce the cost of financing for companies. Companies have been able to issue bonds to investors at all‐time low interest rates. While t ...

... Low absolute levels of interest actually significantly reduce the potential for future returns. One of the primary goals of a zero interest rate policy is to reduce the cost of financing for companies. Companies have been able to issue bonds to investors at all‐time low interest rates. While t ...

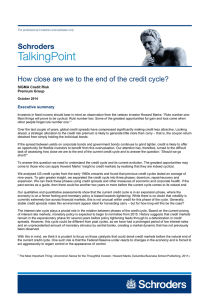

How close are we to the end of the credit cycle?

... The average length of historical credit cycles gives us some insight into the maturity of the current cycle, bearing in mind that this is under the significant assumption that the economy is closed to external macro or geopolitical shocks. As highlighted in the previous section, since the mid-1980s, ...

... The average length of historical credit cycles gives us some insight into the maturity of the current cycle, bearing in mind that this is under the significant assumption that the economy is closed to external macro or geopolitical shocks. As highlighted in the previous section, since the mid-1980s, ...

4 ccr 725-3 mortgage loan originators and mortgage companies 1

... a. Prepayment penalties that extend past the adjustment date of any teaser rate used to calculate a borrower’s monthly mortgage payment; b. Prepayment penalties that extend past the adjustment date of any interest rate used to calculate a borrower’s monthly mortgage payment; c. Prepayment penalties ...

... a. Prepayment penalties that extend past the adjustment date of any teaser rate used to calculate a borrower’s monthly mortgage payment; b. Prepayment penalties that extend past the adjustment date of any interest rate used to calculate a borrower’s monthly mortgage payment; c. Prepayment penalties ...

Loan Securitization and the Monetary Transmission Mechanism

... good, , at time , is the nominal hourly wage, while Π denotes the potential flow of profits from the business sector to the households, and Γ is the income share from renting the fixed amount of capital available in the economy to firms. In addition, [ | ] is the chance that the househ ...

... good, , at time , is the nominal hourly wage, while Π denotes the potential flow of profits from the business sector to the households, and Γ is the income share from renting the fixed amount of capital available in the economy to firms. In addition, [ | ] is the chance that the househ ...

PDF

... may affect the incentives of the borrower (Townsend, 1979) or reduce the cost of monitoring to the lender (Myers and Majluf, 1984; de Meza and Webb, 1987). An important intertemporal issue is short-term verses long-term debt. Borrowers usually prefer longer-term debt contacts due to the liquidity (i ...

... may affect the incentives of the borrower (Townsend, 1979) or reduce the cost of monitoring to the lender (Myers and Majluf, 1984; de Meza and Webb, 1987). An important intertemporal issue is short-term verses long-term debt. Borrowers usually prefer longer-term debt contacts due to the liquidity (i ...

Set 6 - Personal.psu.edu

... c) That means if this hypothesis is correct then we would typically see short rates increasing. Since short rates often go up as well as go down, then we have a problem with this theory. 6. Market segmentation theory (the other extreme) A. Market for different maturity bonds are completely separate. ...

... c) That means if this hypothesis is correct then we would typically see short rates increasing. Since short rates often go up as well as go down, then we have a problem with this theory. 6. Market segmentation theory (the other extreme) A. Market for different maturity bonds are completely separate. ...

competition and leader-follower interactions: panel

... and relatively rigid. This could be an indication of uncompetitive market (Cottarelli dan Kourelis, 1994; Borio and Fritz, 1995). Moreover, responses towards monetary policy among group of banks with different assets are heterogenous. Therefore, it indicates that some behavior related to individual ...

... and relatively rigid. This could be an indication of uncompetitive market (Cottarelli dan Kourelis, 1994; Borio and Fritz, 1995). Moreover, responses towards monetary policy among group of banks with different assets are heterogenous. Therefore, it indicates that some behavior related to individual ...

Uncertainty and Risk

... Private Information Moral hazard exists when one of the parties to an agreement has an incentive after the agreement is made to act in a manner that brings additional benefits to himself or herself at the expense of the other party. Adverse selection is the tendency for people to enter into agreeme ...

... Private Information Moral hazard exists when one of the parties to an agreement has an incentive after the agreement is made to act in a manner that brings additional benefits to himself or herself at the expense of the other party. Adverse selection is the tendency for people to enter into agreeme ...

Solutions to Chapter 11

... expect to see more 40-point days in 2010 even if market risk as measured by percentage returns is no higher than it was in 1990. Est time: 01–05 ...

... expect to see more 40-point days in 2010 even if market risk as measured by percentage returns is no higher than it was in 1990. Est time: 01–05 ...

Understanding Derivative – Beyond Accounting Presented By Safwat Khalid

... relationship. Such changes usually affect securities inversely and can be reduced by diversifying (investing in fixed-income securities with different durations) or hedging (e.g. through an interest rate swap). • Interest rate risk affects the value of bonds more directly than stocks, and it is a ma ...

... relationship. Such changes usually affect securities inversely and can be reduced by diversifying (investing in fixed-income securities with different durations) or hedging (e.g. through an interest rate swap). • Interest rate risk affects the value of bonds more directly than stocks, and it is a ma ...

Merrill Finch Inc

... economy, because the firm’s sales, and hence profits, will generally experience the same type of ups and downs as the economy. If the economy is booming, so will High Tech. On the other hand, Collections is considered by many investors to be a hedge against both bad times and high inflation, so if t ...

... economy, because the firm’s sales, and hence profits, will generally experience the same type of ups and downs as the economy. If the economy is booming, so will High Tech. On the other hand, Collections is considered by many investors to be a hedge against both bad times and high inflation, so if t ...

Financially Speaking

... periods of time the equity risk premium, loosely defined as the extra return investors expect from equities over bonds, has been stable. Therefore, low interest rates ultimately imply higher prices for growth assets, which ultimately flow through to lower prospective returns. It’s fairly easy to justi ...

... periods of time the equity risk premium, loosely defined as the extra return investors expect from equities over bonds, has been stable. Therefore, low interest rates ultimately imply higher prices for growth assets, which ultimately flow through to lower prospective returns. It’s fairly easy to justi ...

Credit rationing

Credit rationing refers to the situation where lenders limit the supply of additional credit to borrowers who demand funds, even if the latter are willing to pay higher interest rates. It is an example of market imperfection, or market failure, as the price mechanism fails to bring about equilibrium in the market. It should not be confused with cases where credit is simply ""too expensive"" for some borrowers, that is, situations where the interest rate is deemed too high. On the contrary, the borrower would like to acquire the funds at the current rates, and the imperfection refers to the absence of equilibrium in spite of willing borrowers. In other words, at the prevailing market interest rate, demand exceeds supply, but lenders are not willing to either loan more funds, or raise the interest rate charged, as they are already maximising profits.