The Economics of Solicited and Unsolicited Credit Ratings

... • How realistic is assumption that 0-type cannot be rated? – Firms are collections of projects and a very large proportion of major firms have some basis on which they could be rated – Using this device seems to unnecessarily limit scope of model; if a similar result could be obtained with a less re ...

... • How realistic is assumption that 0-type cannot be rated? – Firms are collections of projects and a very large proportion of major firms have some basis on which they could be rated – Using this device seems to unnecessarily limit scope of model; if a similar result could be obtained with a less re ...

Chapter 12 Overlapping generations in continuous time

... In this chapter we return to issues where life-cycle aspects of the economy are important and a representative agent framework therefore not suitable. We shall see how an overlapping generations (OLG) structure can be made compatible with continuous time analysis. The two-period OLG models considere ...

... In this chapter we return to issues where life-cycle aspects of the economy are important and a representative agent framework therefore not suitable. We shall see how an overlapping generations (OLG) structure can be made compatible with continuous time analysis. The two-period OLG models considere ...

Norges Bank Working Paper 2012/18

... sensitive than collateral to the average quality of borrowers in a pool. If that average is too low, high-quality borrowers will prefer to post collateral rather than be screened, even though that may lead to higher loan losses and be inefficient from a social point of view. In contrast, we examine ...

... sensitive than collateral to the average quality of borrowers in a pool. If that average is too low, high-quality borrowers will prefer to post collateral rather than be screened, even though that may lead to higher loan losses and be inefficient from a social point of view. In contrast, we examine ...

Value at Risk - dedeklegacy.cz

... repayment of a bond or coupons of the bond, repayment of loan or charged interest); ii) debtors are downgraded by credit agencies iii) credit spreads are widened due to external events beyond debtor’s control (i.e. increased political uncertainty, a higher macroeconomic instability) rating agencies ...

... repayment of a bond or coupons of the bond, repayment of loan or charged interest); ii) debtors are downgraded by credit agencies iii) credit spreads are widened due to external events beyond debtor’s control (i.e. increased political uncertainty, a higher macroeconomic instability) rating agencies ...

Mensch tracht, und Gott lacht

... about the impact of monetary policy: since interest rates have been at such exceptionally low levels for so long there is unusual uncertainty about how the return towards more usual levels will affect the economy. The third source of uncertainty is how fast the economy grows in the absence of moneta ...

... about the impact of monetary policy: since interest rates have been at such exceptionally low levels for so long there is unusual uncertainty about how the return towards more usual levels will affect the economy. The third source of uncertainty is how fast the economy grows in the absence of moneta ...

Read now

... NCREIF income is less valid as a proxy for the timber discount rate because income can vary based on the underlying age class of timberland properties in the index. Also, NCREIF timber cash yields are a snapshot based on a single quarter’s return, whereas in practice timberland is typically valued b ...

... NCREIF income is less valid as a proxy for the timber discount rate because income can vary based on the underlying age class of timberland properties in the index. Also, NCREIF timber cash yields are a snapshot based on a single quarter’s return, whereas in practice timberland is typically valued b ...

Interest Rate Risk Management for Commercial

... Variation in market interest rates can also affect the economic value of a banking institution‟s assets, liabilities and OBS positions. The economic value of an instrument represents an assessment of the present value of its expected net cash flows, discounted to reflect market rates. The economic v ...

... Variation in market interest rates can also affect the economic value of a banking institution‟s assets, liabilities and OBS positions. The economic value of an instrument represents an assessment of the present value of its expected net cash flows, discounted to reflect market rates. The economic v ...

The effect of monetary and fiscal policy on interest

... Fiscal policy has been used where all other mechanisms including monetary policy have failed. The industrialized world suffered over the last few years a number of large negative shocks, initially driven by sharp declines in house and stock prices and by a tightening of credit and financial conditio ...

... Fiscal policy has been used where all other mechanisms including monetary policy have failed. The industrialized world suffered over the last few years a number of large negative shocks, initially driven by sharp declines in house and stock prices and by a tightening of credit and financial conditio ...

Valuation of Corporate Loans: A Credit Migration Approach

... more than the usage option, and the importance of this option increased over the timeframe of the sample. Finally, we show that loans for which the option values are high are more likely to prepay. The next section of this paper provides an overview on how CreditMark values a loan. It presents some ...

... more than the usage option, and the importance of this option increased over the timeframe of the sample. Finally, we show that loans for which the option values are high are more likely to prepay. The next section of this paper provides an overview on how CreditMark values a loan. It presents some ...

Banks, Bonds, and the Liquidity Effect

... an unexpected “easing” of monetary policy in terms of the dynamic response of each of the five variables in the model. Rows A and B correspond to the quarterly model, where the responses to a one standard deviation positive shock to RES (row A) and to a one standard deviation negative shock to RFF (a ...

... an unexpected “easing” of monetary policy in terms of the dynamic response of each of the five variables in the model. Rows A and B correspond to the quarterly model, where the responses to a one standard deviation positive shock to RES (row A) and to a one standard deviation negative shock to RFF (a ...

The Macroeconomic Transition to High Household Debt Jeffrey R. Campbell Zvi Hercowitz

... amortizes. The implied forced savings reflected the desire of the Roosevelt administration to reduce the likelihood of a mass default of highly-leveraged mortgagees, as occurred at the beginning of the Great Depression. A host of financial regulations supported this policy. The most prominent gave t ...

... amortizes. The implied forced savings reflected the desire of the Roosevelt administration to reduce the likelihood of a mass default of highly-leveraged mortgagees, as occurred at the beginning of the Great Depression. A host of financial regulations supported this policy. The most prominent gave t ...

Modeling Portfolios that Contain Risky Assets I: Risk and

... secondary markets where their value is based on current interest rates. For example, if interest rates go up then bond values will go down on the secondary market. The risk associated with a bond reflects the uncertainty about the credit worthiness of the borrower. Short term bonds are generally les ...

... secondary markets where their value is based on current interest rates. For example, if interest rates go up then bond values will go down on the secondary market. The risk associated with a bond reflects the uncertainty about the credit worthiness of the borrower. Short term bonds are generally les ...

a letter to our peers

... elsewhere, even if less so with those doing village banking in low end markets. But as mentioned before, the most important differences between Mexico and other markets is loan size, both in nominal as well as in adjusted terms, as well as the wealth of the economy. If we had a loan size double of w ...

... elsewhere, even if less so with those doing village banking in low end markets. But as mentioned before, the most important differences between Mexico and other markets is loan size, both in nominal as well as in adjusted terms, as well as the wealth of the economy. If we had a loan size double of w ...

Recent episodes of credit card distress in Asia

... networks tried to enter the credit card market through direct marketing. In Taiwan, financial liberalisation in the early 1990s doubled the number of banks in an already crowded market. These newcomers targeted the consumer banking business, doubling their market share from 28% in 1994 to 56% in 200 ...

... networks tried to enter the credit card market through direct marketing. In Taiwan, financial liberalisation in the early 1990s doubled the number of banks in an already crowded market. These newcomers targeted the consumer banking business, doubling their market share from 28% in 1994 to 56% in 200 ...

Risk Management and Financial Institutions

... a good one for exchange rates. What should you do? – You should buy deep-out-of-the-money call and put options on a variety of different currencies – and wait. These options will be relatively inexpensive and more of them will close in the money than the lognormal model predicts. The present value o ...

... a good one for exchange rates. What should you do? – You should buy deep-out-of-the-money call and put options on a variety of different currencies – and wait. These options will be relatively inexpensive and more of them will close in the money than the lognormal model predicts. The present value o ...

National Foreclosure Settlement

... higher credits, so servicers may be more likely to offer those types of modifications. “Consumer relief” granted between March 1, 2012, and February 28, 2013, will receive a 25% bonus credit, so motivation exists for servicers to move quickly this first year. Principal write-downs for liens with hig ...

... higher credits, so servicers may be more likely to offer those types of modifications. “Consumer relief” granted between March 1, 2012, and February 28, 2013, will receive a 25% bonus credit, so motivation exists for servicers to move quickly this first year. Principal write-downs for liens with hig ...

PPT

... • Equilibrium real federal funds rate is the estimate of the inflation-adjusted federal funds rate that would be consistent with maintaining real GDP at its potential level in the long run. • Inflation gap is the difference between current inflation and the Fed’s target rate of inflation (could be p ...

... • Equilibrium real federal funds rate is the estimate of the inflation-adjusted federal funds rate that would be consistent with maintaining real GDP at its potential level in the long run. • Inflation gap is the difference between current inflation and the Fed’s target rate of inflation (could be p ...

A Brief Postwar History of US Consumer Finance

... complexity and flexibility of financial options, was not matched by a commensurate rise either in financial capabilities of consumers nor in financial advice provided by third parties. We begin this paper by outlining the basic functions of household finance. We trace the rising demand for consumer ...

... complexity and flexibility of financial options, was not matched by a commensurate rise either in financial capabilities of consumers nor in financial advice provided by third parties. We begin this paper by outlining the basic functions of household finance. We trace the rising demand for consumer ...

view - Pacra.com

... PACRA may provide consultancy/advisory services or other services to any of its clients or to any of its clients' associated companies and associated undertakings that is being rated or has been rated by it. In such cases, PACRA has adequate mechanism in place ensuring that provision of such service ...

... PACRA may provide consultancy/advisory services or other services to any of its clients or to any of its clients' associated companies and associated undertakings that is being rated or has been rated by it. In such cases, PACRA has adequate mechanism in place ensuring that provision of such service ...

NBER WORKING PAPER SERIES ON OVERBORROWING Martin Uribe Working Paper 11913

... by rough indicators of the emerging country’s macroeconomic performance and not by careful assessment of individual borrowers’ abilities to repay. This is because individual agents fail to internalize the effect their own borrowing decisions have on the country’s aggregate credit conditions. Overbor ...

... by rough indicators of the emerging country’s macroeconomic performance and not by careful assessment of individual borrowers’ abilities to repay. This is because individual agents fail to internalize the effect their own borrowing decisions have on the country’s aggregate credit conditions. Overbor ...

Chapter 11 Money and Monetary Policy

... recession. Over the next several years, prices gently but steadily fell at a rate of about 1% per year. These situations can be very frustrating, when looked at from the perspective of the real potential productivity of an economy. People may want to work and spend, and businesses might have great i ...

... recession. Over the next several years, prices gently but steadily fell at a rate of about 1% per year. These situations can be very frustrating, when looked at from the perspective of the real potential productivity of an economy. People may want to work and spend, and businesses might have great i ...

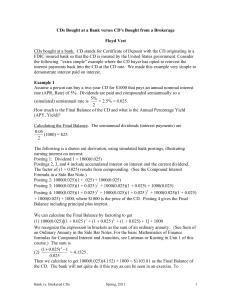

CDs Bought at a Bank verses CD`s Bought from a Brokerage Floyd

... APY. Write down the 1-, 2-, and 5-year rates. Write down the National Average rates and compare with the top rates. Do some math to compare the differences on a $100,000 CD from age 30 to 70. • For CDs bought from a brokerage, go to www.vanguard.com. Click on Go to Personal Investors Site. Under Res ...

... APY. Write down the 1-, 2-, and 5-year rates. Write down the National Average rates and compare with the top rates. Do some math to compare the differences on a $100,000 CD from age 30 to 70. • For CDs bought from a brokerage, go to www.vanguard.com. Click on Go to Personal Investors Site. Under Res ...

Selecting Project Portfolios by Optimizing Simulations

... talking about project portfolios, we assume here that a firm can have fractional participation levels in a project. We can easily modify the equation so that the decision is whether or not to invest in a project, by writing w (0, 1) instead. In practice, small changes in the estimated parameter in ...

... talking about project portfolios, we assume here that a firm can have fractional participation levels in a project. We can easily modify the equation so that the decision is whether or not to invest in a project, by writing w (0, 1) instead. In practice, small changes in the estimated parameter in ...

NBER WORKING PAPER SERIES HUMAN CAPITAL FORMATION WITH ENDOGENOUS CREDIT CONSTRAINTS

... Disagreement about the importance of credit constraints in determining schooling levels in the U.S. abounds. Kane [30] argues that differences in family income are responsible for a sizeable difference in college enrollment rates. However, Cameron and Heckman [8, 9] find that after controlling for c ...

... Disagreement about the importance of credit constraints in determining schooling levels in the U.S. abounds. Kane [30] argues that differences in family income are responsible for a sizeable difference in college enrollment rates. However, Cameron and Heckman [8, 9] find that after controlling for c ...

Credit rationing

Credit rationing refers to the situation where lenders limit the supply of additional credit to borrowers who demand funds, even if the latter are willing to pay higher interest rates. It is an example of market imperfection, or market failure, as the price mechanism fails to bring about equilibrium in the market. It should not be confused with cases where credit is simply ""too expensive"" for some borrowers, that is, situations where the interest rate is deemed too high. On the contrary, the borrower would like to acquire the funds at the current rates, and the imperfection refers to the absence of equilibrium in spite of willing borrowers. In other words, at the prevailing market interest rate, demand exceeds supply, but lenders are not willing to either loan more funds, or raise the interest rate charged, as they are already maximising profits.