The effect of rising interest rates on bonds, stocks and real

... and market conditions. Past performance is not indicative of future results. This material is for informational or educational purposes only and does not constitute a recommendation or investment advice in connection with a distribution, transfer or rollover, a purchase or sale of securities or othe ...

... and market conditions. Past performance is not indicative of future results. This material is for informational or educational purposes only and does not constitute a recommendation or investment advice in connection with a distribution, transfer or rollover, a purchase or sale of securities or othe ...

Supplemental Instruction Finance 301: Porter 1o/22/08 A bond that

... 6. Six years ago a company issued 20 year bonds with a 14% annual coupon rate at their $1000 par value. The bonds had a 9% call premium, with 5 years of call protection. Today, they called the bonds. Compute the realized rate of return for an investor who purchased the bonds when they were issued an ...

... 6. Six years ago a company issued 20 year bonds with a 14% annual coupon rate at their $1000 par value. The bonds had a 9% call premium, with 5 years of call protection. Today, they called the bonds. Compute the realized rate of return for an investor who purchased the bonds when they were issued an ...

Savings Accounts

... Rule of 72. A method used to estimate the amount of time or interest it will take for savings to double in value. Truth in Savings Act-Law established in 1991, requires financial institutions to provide information about costs and interest-earning accounts in uniform terms. Helps consumers compare s ...

... Rule of 72. A method used to estimate the amount of time or interest it will take for savings to double in value. Truth in Savings Act-Law established in 1991, requires financial institutions to provide information about costs and interest-earning accounts in uniform terms. Helps consumers compare s ...

Model of debt crisis, Romer 4th edition section 12.10

... • So there are two equilibria, one when the interest factor and the probability of default are low, one where no investor want to hold the debt • For a sufficiently large riskless rate RMIN (Figure 12.6 next) the red curve is on the right of the blue curve and the only equilibrium is π=1. You don’t ...

... • So there are two equilibria, one when the interest factor and the probability of default are low, one where no investor want to hold the debt • For a sufficiently large riskless rate RMIN (Figure 12.6 next) the red curve is on the right of the blue curve and the only equilibrium is π=1. You don’t ...

Term Structure

... “The bond will pay interest at a rate of 16% of par, semiannually on each October 15 and April 15 from April 15, 2009 through April 15, 2024. The annual interest rate is 16%. On April 15, 2024 the bond will make its final interest payment and also pay the holder the par value of $1,000. ...

... “The bond will pay interest at a rate of 16% of par, semiannually on each October 15 and April 15 from April 15, 2009 through April 15, 2024. The annual interest rate is 16%. On April 15, 2024 the bond will make its final interest payment and also pay the holder the par value of $1,000. ...

Low interest rates pressuring US bank margins

... closer look, however, reveals this profitability was mainly a result of lower loan loss provisions. Provisions declined year-over-year for the ninth consecutive quarter, but now appear to be levelling off. Whether or not banks can continue these profitability trends remains a key concern in the near ...

... closer look, however, reveals this profitability was mainly a result of lower loan loss provisions. Provisions declined year-over-year for the ninth consecutive quarter, but now appear to be levelling off. Whether or not banks can continue these profitability trends remains a key concern in the near ...

Short Questions

... Assume that the velocity of circulation of money remains unchanged. (1) %M = %P + %Y = 4% + 2% = 6% (2) The government should maintain the growth rate of money supply at 6% per year. 2(a) The cost of holding cash is the nominal interest rate, i.e., 9%. (2) 2(b) Fisher equation: Nominal interest r ...

... Assume that the velocity of circulation of money remains unchanged. (1) %M = %P + %Y = 4% + 2% = 6% (2) The government should maintain the growth rate of money supply at 6% per year. 2(a) The cost of holding cash is the nominal interest rate, i.e., 9%. (2) 2(b) Fisher equation: Nominal interest r ...

Caught in a deflation trap

... with the Great Depression of the 1930s and Japan’s more recent slump. Six years ago I wrote a paper along with some of my former colleagues at the US Federal Reserve that examined Japan’s experience to shed light on how countries might prevent deflation. Alas, I think it’s time to dust off that stud ...

... with the Great Depression of the 1930s and Japan’s more recent slump. Six years ago I wrote a paper along with some of my former colleagues at the US Federal Reserve that examined Japan’s experience to shed light on how countries might prevent deflation. Alas, I think it’s time to dust off that stud ...

ECON 4110

... A) at higher bond prices more loanable funds will be supplied. B) an increase in the interest rate makes lenders more willing and able to supply more funds. C) higher interest rates reduce the inflation rate. D) a decrease in the interest rate makes lenders more willing and able to supply more funds ...

... A) at higher bond prices more loanable funds will be supplied. B) an increase in the interest rate makes lenders more willing and able to supply more funds. C) higher interest rates reduce the inflation rate. D) a decrease in the interest rate makes lenders more willing and able to supply more funds ...

Questions

... If officials try to restrain the bubble through interest rates, the real economy may be damaged (by hurting export and investment). If the bubble is burst, a recession may be triggered. In the case of the property market in NZ and other countries if the monetary authorities raise interest rates, low ...

... If officials try to restrain the bubble through interest rates, the real economy may be damaged (by hurting export and investment). If the bubble is burst, a recession may be triggered. In the case of the property market in NZ and other countries if the monetary authorities raise interest rates, low ...

Negative real yields on inflation linked bonds

... This short comment provides an explanation of why real yields are negative in the US, and whether they offer good value as an investment at current levels. Bonds are loans, and we are used to the idea that in return for lending money we receive interest as compensation. This same logic applies to bo ...

... This short comment provides an explanation of why real yields are negative in the US, and whether they offer good value as an investment at current levels. Bonds are loans, and we are used to the idea that in return for lending money we receive interest as compensation. This same logic applies to bo ...

The 10-Year Yield Is A Whopping 4 Standard

... which substantially underperformed Treasuries during the rate rise—now recovering sharply," With the reality that the economy has likely peaked for this current economic cycle, deflationary pressures rising and the potential for less monetary interventions in the quarters ahead the catalysts for hig ...

... which substantially underperformed Treasuries during the rate rise—now recovering sharply," With the reality that the economy has likely peaked for this current economic cycle, deflationary pressures rising and the potential for less monetary interventions in the quarters ahead the catalysts for hig ...

Problem Set 3 Answers - University of Wisconsin–Madison

... 10. Consider the case of a manager of a bank that is attempting to reduce the risk associated with interest rate changes. The bank has $30 million of fixed-rate assets, $20 million of rate-sensitive assets, $10 million of fixed-rate liabilities, and $40 million of rate-sensitive liabilities. If the ...

... 10. Consider the case of a manager of a bank that is attempting to reduce the risk associated with interest rate changes. The bank has $30 million of fixed-rate assets, $20 million of rate-sensitive assets, $10 million of fixed-rate liabilities, and $40 million of rate-sensitive liabilities. If the ...

Measuring the Duration of Liabilities

... • Examples of loss costs that might go into m – Medical evaluations performed immediately prior to determining the settlement offer – General damages to the extent they are based on the cost of living at the time of settlement – Loss adjustment expenses connected with settling the claim ...

... • Examples of loss costs that might go into m – Medical evaluations performed immediately prior to determining the settlement offer – General damages to the extent they are based on the cost of living at the time of settlement – Loss adjustment expenses connected with settling the claim ...

The Great Recession

... Economy grows via increases in consumption of goods & services • Stagnant wages posed a problem for growth • Real estate became focus of investment & cheap money • Low interest rates & high growth in housing prices • Homeowners could take out cheap equity loans to consume • Speculators could realiz ...

... Economy grows via increases in consumption of goods & services • Stagnant wages posed a problem for growth • Real estate became focus of investment & cheap money • Low interest rates & high growth in housing prices • Homeowners could take out cheap equity loans to consume • Speculators could realiz ...

Interest Rate and Credit Default Swaps

... BONUS Exotic Investments Lesson 2 Interest Rate and Credit Default Swaps ...

... BONUS Exotic Investments Lesson 2 Interest Rate and Credit Default Swaps ...

Chapter 9 - McGraw Hill Higher Education

... 6. Show how a line of credit affects financial statements. 7. Explain how to account for bonds issued at face value and their related interest costs. 8. Use the straight-line method to amortize bond discounts and premiums. 9. Distinguish between current and noncurrent assets and liabilities. 10. Pre ...

... 6. Show how a line of credit affects financial statements. 7. Explain how to account for bonds issued at face value and their related interest costs. 8. Use the straight-line method to amortize bond discounts and premiums. 9. Distinguish between current and noncurrent assets and liabilities. 10. Pre ...

Chapter 6

... tax rate on what appear to be comparable bonds. Why? Not widely held → more difficult to buy and sell in secondary markets → must pay a positive liquidity premium. ...

... tax rate on what appear to be comparable bonds. Why? Not widely held → more difficult to buy and sell in secondary markets → must pay a positive liquidity premium. ...

presentation source

... willing to delay consumption ), the supply of savings will increase and the equilibrium interest rate will decrease. ...

... willing to delay consumption ), the supply of savings will increase and the equilibrium interest rate will decrease. ...

1 of 35

... including zero-coupon rate bonds, floating rate bonds and real return bonds. (LO4) 5. Outline the characteristics of long-term ...

... including zero-coupon rate bonds, floating rate bonds and real return bonds. (LO4) 5. Outline the characteristics of long-term ...

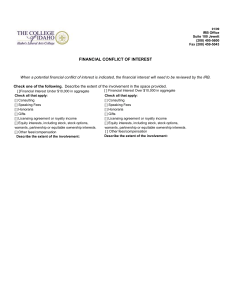

FinancialDisclosure

... When a potential financial conflict of interest is indicated, the financial interest will need to be reviewed by the IRB. Check one of the following. Describe the extent of the involvement in the space provided. [ ]Financial Interest Under $10,000 in aggregate Check all that apply: [ ] Consulting [ ...

... When a potential financial conflict of interest is indicated, the financial interest will need to be reviewed by the IRB. Check one of the following. Describe the extent of the involvement in the space provided. [ ]Financial Interest Under $10,000 in aggregate Check all that apply: [ ] Consulting [ ...

Interest

Interest is money paid by a borrower to a lender for a credit or a similar liability. Important examples are bond yields, interest paid for bank loans, and returns on savings. Interest differs from profit in that it is paid to a lender, whereas profit is paid to an owner. In economics, the various forms of credit are also referred to as loanable funds.When money is borrowed, interest is typically calculated as a percentage of the principal, the amount owed to the lender. The percentage of the principal that is paid over a certain period of time (typically a year) is called the interest rate. Interest rates are market prices which are determined by supply and demand. They are generally positive because loanable funds are scarce.Interest is often compounded, which means that interest is earned on prior interest in addition to the principal. The total amount of debt grows exponentially, and its mathematical study led to the discovery of the number e. In practice, interest is most often calculated on a daily, monthly, or yearly basis, and its impact is influenced greatly by its compounding rate.