Chapter 9.2 Organization of the US Economy

... 2. To make individual choices 3. To engage in economic competition 4. To make decisions based on self-interest 5. To participate in the economy with limited government involvement and regulation. ...

... 2. To make individual choices 3. To engage in economic competition 4. To make decisions based on self-interest 5. To participate in the economy with limited government involvement and regulation. ...

![Chapter_23[1]](http://s1.studyres.com/store/data/008225109_1-11ea091a04b742c5dc8b7150833e6ba6-300x300.png)

Chapter_23[1]

... Advisor to the UK National Coal Board for two decades along with many socialist, anarchists, and utopians ...

... Advisor to the UK National Coal Board for two decades along with many socialist, anarchists, and utopians ...

Homework H due 7th November68.5 KB

... The test of any economy is the extent to which it solves the basic _____________________ problem. In a free market, resources are allocated via the ___________________ mechanism. This system of allocation is commonly referred to as _________________________. In the free market, an increase in demand ...

... The test of any economy is the extent to which it solves the basic _____________________ problem. In a free market, resources are allocated via the ___________________ mechanism. This system of allocation is commonly referred to as _________________________. In the free market, an increase in demand ...

Chapter 9.2 Organization of the U.S. Economy

... 2. To make individual choices 3. To engage in economic competition 4. To make decisions based on self-interest 5. To participate in the economy with limited government involvement and regulation. ...

... 2. To make individual choices 3. To engage in economic competition 4. To make decisions based on self-interest 5. To participate in the economy with limited government involvement and regulation. ...

Comparing countries KEY

... Directions: After reviewing the PowerPoint on European Economies, fill in the chart below with information that you have learned. Economic System What to produce? Business ...

... Directions: After reviewing the PowerPoint on European Economies, fill in the chart below with information that you have learned. Economic System What to produce? Business ...

Chapter 1 Notes

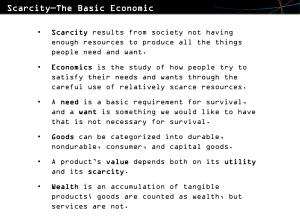

... Economics is the study of how people try to satisfy their needs and wants through the careful use of relatively scarce resources. ...

... Economics is the study of how people try to satisfy their needs and wants through the careful use of relatively scarce resources. ...

Economic Systems - Swan Hills School

... takes a laissez-faire (“hands-off”) approach to the economy. ...

... takes a laissez-faire (“hands-off”) approach to the economy. ...

Marx and Smith

... • Adam Smith wrote in his book “The Wealth of Nations” that if the government did not interfere with business and competition then the economy would grow. Prices would be competitive and products would be better quality. • Similar to Market Economy, and Laissez-faire economics. ...

... • Adam Smith wrote in his book “The Wealth of Nations” that if the government did not interfere with business and competition then the economy would grow. Prices would be competitive and products would be better quality. • Similar to Market Economy, and Laissez-faire economics. ...

Review Questions with answers

... the EU members more trading power; create a peaceful, stable Europe; assist each other in social and environmental issues 2. What are some advantages (benefits) members of the EU received because of the formation of the European Union? More trading power; no tariffs for member nations; higher standa ...

... the EU members more trading power; create a peaceful, stable Europe; assist each other in social and environmental issues 2. What are some advantages (benefits) members of the EU received because of the formation of the European Union? More trading power; no tariffs for member nations; higher standa ...

Economic Vocabulary Quiz - Southwest Golden Eagles

... a. market b. demand c. scarcity d. rate 2. In _____________ economy decisions are guided by the change in prices that occur between individual buyers and sellers in the market place. a. traditional b. market c. capitalism d. enterprise 3. In ______________ economy customs and habits of the past are ...

... a. market b. demand c. scarcity d. rate 2. In _____________ economy decisions are guided by the change in prices that occur between individual buyers and sellers in the market place. a. traditional b. market c. capitalism d. enterprise 3. In ______________ economy customs and habits of the past are ...

Unit 8 Types of economies

... ◦ Answers the 3 economic questions-How, What and to Whom should we produce. ◦ Sets prices for wages, goods, services ◦ Makes production decisions. ...

... ◦ Answers the 3 economic questions-How, What and to Whom should we produce. ◦ Sets prices for wages, goods, services ◦ Makes production decisions. ...

Econ 2101 Macroeconomic Theory

... ANSWER: The MARKET! Adam Smith (1723-1790) first suggested that a complex market system with no one in charge would work to coordinate all economic activity. This idea became known as Capitalism. - Traditionalism - Centralized Planning - Capitalism and Free Markets ...

... ANSWER: The MARKET! Adam Smith (1723-1790) first suggested that a complex market system with no one in charge would work to coordinate all economic activity. This idea became known as Capitalism. - Traditionalism - Centralized Planning - Capitalism and Free Markets ...

Essential Question: What are the similarities and differences in

... Service industries like banking, insurance, and business services account for most of the UK’s gross domestic product Over the decades, the government has turned over many state-owned companies to private ownership setting up free market competition ...

... Service industries like banking, insurance, and business services account for most of the UK’s gross domestic product Over the decades, the government has turned over many state-owned companies to private ownership setting up free market competition ...

A SUMMARY OF THE HISTORY OF ECONOMIC THEORIES Mgt. 704

... • Different perspectives are appropriate for analyzing the short run and the long run. • The primary difference is that prices and expectations are flexible in the long run, while they can be sticky in the short run. • Lags in the effects of fiscal and monetary ...

... • Different perspectives are appropriate for analyzing the short run and the long run. • The primary difference is that prices and expectations are flexible in the long run, while they can be sticky in the short run. • Lags in the effects of fiscal and monetary ...

Gross Domestic Product (“GDP”)

... produced yearly by the nation and the amount of income people have to spend. ...

... produced yearly by the nation and the amount of income people have to spend. ...

Command & Traditional Economies - Hamburg Central School District

... practice of people taking factory light bulbs to use in their homes was the result of: a) Shortage b) Scarcity ...

... practice of people taking factory light bulbs to use in their homes was the result of: a) Shortage b) Scarcity ...

L3-Why Ecological Economics

... • Sustainable growth is an oxymoron • Ever continuing growth in material consumption is an impossible goal • BUT welfare is a psychic flux, not a physical flux. • Economic development is possible, but not continuous economic growth ...

... • Sustainable growth is an oxymoron • Ever continuing growth in material consumption is an impossible goal • BUT welfare is a psychic flux, not a physical flux. • Economic development is possible, but not continuous economic growth ...

Lesson 2.1 Worksheet

... 13. Complete the tables below to show how the quantity produced and the quantity purchased change in a typical market. On the lines below the tables, describe what might happen if consumers were willing to pay a high price for a new sustainable product, such as a very energy and water efficient yet ...

... 13. Complete the tables below to show how the quantity produced and the quantity purchased change in a typical market. On the lines below the tables, describe what might happen if consumers were willing to pay a high price for a new sustainable product, such as a very energy and water efficient yet ...