Sample Packet for: Tim Taylor’s Includes:

... Economists use the term demand to refer to a relationship between price and the quantity demanded. Price is what a buyer pays (or the seller receives) for a unit of the specific good or service. Quantity demanded refers to the total number of units that are purchased at that price. A rise in price o ...

... Economists use the term demand to refer to a relationship between price and the quantity demanded. Price is what a buyer pays (or the seller receives) for a unit of the specific good or service. Quantity demanded refers to the total number of units that are purchased at that price. A rise in price o ...

Theory of Consumer Behavior

... 2. The slope of the TU curve = TU/Q = MU 3. As long as MU is positive, TU increases. Since each of the first 6 units has positive MU, the student’s TU increases as he consumes the first 6 slices. This means each of the first 6 units added to his TU. 4. When MU is zero, TU has stopped increasing an ...

... 2. The slope of the TU curve = TU/Q = MU 3. As long as MU is positive, TU increases. Since each of the first 6 units has positive MU, the student’s TU increases as he consumes the first 6 slices. This means each of the first 6 units added to his TU. 4. When MU is zero, TU has stopped increasing an ...

price elasticity of demand

... price elasticity of demand between wireless and wired phone services is about 0.02. • This estimate implies that a 10% increase in the price of land-wired phone services induces a 0.2% increase in the quantity of wireless phone services demanded. • Thus, the two types of phone services appear to be ...

... price elasticity of demand between wireless and wired phone services is about 0.02. • This estimate implies that a 10% increase in the price of land-wired phone services induces a 0.2% increase in the quantity of wireless phone services demanded. • Thus, the two types of phone services appear to be ...

Monopoly WHY MONOPOLIES ARISE WHY MONOPOLIES ARISE

... • Price discrimination is not possible when a good is sold in a competitive market since there are many firms all selling at the market price. In order to price discriminate, the firm must ...

... • Price discrimination is not possible when a good is sold in a competitive market since there are many firms all selling at the market price. In order to price discriminate, the firm must ...

Making decisions

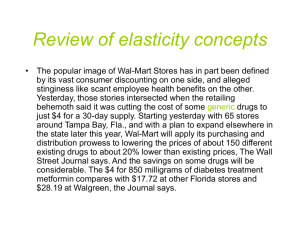

... the state later this year, Wal-Mart will apply its purchasing and distribution prowess to lowering the prices of about 150 different existing drugs to about 20% lower than existing prices, The Wall Street Journal says. And the savings on some drugs will be considerable. The $4 for 850 milligrams of ...

... the state later this year, Wal-Mart will apply its purchasing and distribution prowess to lowering the prices of about 150 different existing drugs to about 20% lower than existing prices, The Wall Street Journal says. And the savings on some drugs will be considerable. The $4 for 850 milligrams of ...

PowerPoint Demand and Supply

... • Substitution effect is when people can replace one product with another if it satisfies the same need. • Utility is the ability of any good or service to satisfy consumer wants. • People will purchase additional items until the satisfaction from the last unit is equal to the price. • The les ...

... • Substitution effect is when people can replace one product with another if it satisfies the same need. • Utility is the ability of any good or service to satisfy consumer wants. • People will purchase additional items until the satisfaction from the last unit is equal to the price. • The les ...

Pdf - Text of NPTEL IIT Video Lectures

... regarding the change in the Q. That happens in the last box, the last row last column when there is a decrease in the supply and increase in demand that leads to ambiguity for the, change of P, but the Q generally decreases. So, to summarize this, we can say that, when there is a, when there is both ...

... regarding the change in the Q. That happens in the last box, the last row last column when there is a decrease in the supply and increase in demand that leads to ambiguity for the, change of P, but the Q generally decreases. So, to summarize this, we can say that, when there is a, when there is both ...

Firms decision making

... • Demand curve (1): for different prices, the quantity of output that customers will choose to purchase from that firm (individual firm but all buyers) • Demand curve (2): shows us the maximum price the firm can charge to sell any given amount of output (one degree of freedom; price or level of outp ...

... • Demand curve (1): for different prices, the quantity of output that customers will choose to purchase from that firm (individual firm but all buyers) • Demand curve (2): shows us the maximum price the firm can charge to sell any given amount of output (one degree of freedom; price or level of outp ...

Consumers, Producers, and the Efficiency of Markets

... to pay for the second unit and so on (on a price and quantity graph), we have plotted the market demand curve for the good. That is, the height of the demand curve is the marginal buyers’ willingness to pay. Because some buyers value a good more than other buyers, the demand curve is downward slopin ...

... to pay for the second unit and so on (on a price and quantity graph), we have plotted the market demand curve for the good. That is, the height of the demand curve is the marginal buyers’ willingness to pay. Because some buyers value a good more than other buyers, the demand curve is downward slopin ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑