THE LAW OF SUPPLY - Oregon State University

... • Occurs when the market price is below the equilibrium price. • Consumers are willing to buy more of the product, at this lower price, than producers are willing to sell. ...

... • Occurs when the market price is below the equilibrium price. • Consumers are willing to buy more of the product, at this lower price, than producers are willing to sell. ...

Supply and Demand

... (Cars) Demand is inelastic when price changes have very little effect on the demand for the product (Medicine) ...

... (Cars) Demand is inelastic when price changes have very little effect on the demand for the product (Medicine) ...

Prices and Decision Making

... Many cities have rent control laws to make sure that poor people can find apartments they can afford. But landlords do not find it profitable to rent at these prices and sometimes convert their buildings to condominium or cooperative ownership. This reduces the number of apartments available: it cre ...

... Many cities have rent control laws to make sure that poor people can find apartments they can afford. But landlords do not find it profitable to rent at these prices and sometimes convert their buildings to condominium or cooperative ownership. This reduces the number of apartments available: it cre ...

Midterm Study Guide - Partial Answers

... U.S. manufacturers still want. You could model this in one of two ways redraw supply of car parts as very elastic, so the effects on graph 1 and 2 would be small, (and explain that the new quantity is composed of foreign parts), or you could shift the demand for U.S. parts INWARDS, since Thai parts ...

... U.S. manufacturers still want. You could model this in one of two ways redraw supply of car parts as very elastic, so the effects on graph 1 and 2 would be small, (and explain that the new quantity is composed of foreign parts), or you could shift the demand for U.S. parts INWARDS, since Thai parts ...

Assignment Guide: Unit II

... Objectives and Key Terms—You must be able to: 1) Define a market. 2) Define demand and state the law of demand. 3) Graph the demand curve when given a demand schedule. 4) Explain the difference between individual demand and market demand. 5) Differentiate between a change in demand and a change in q ...

... Objectives and Key Terms—You must be able to: 1) Define a market. 2) Define demand and state the law of demand. 3) Graph the demand curve when given a demand schedule. 4) Explain the difference between individual demand and market demand. 5) Differentiate between a change in demand and a change in q ...

Ap Econ Chap 4 - mrski-apecon-2008

... economic competition for the good or service.(a specific individual or enterprise has sufficient control over a particular product or service to determine significantly the terms on which other individuals shall have access to it) ...

... economic competition for the good or service.(a specific individual or enterprise has sufficient control over a particular product or service to determine significantly the terms on which other individuals shall have access to it) ...

Changes in Market Equilibrium

... Changes in Market Equilibrium In this lesson, students will identify factors that can shift a market into disequilibrium. Students will be able to identify and/or define the following terms: Disequilibrium Surplus Shortage ...

... Changes in Market Equilibrium In this lesson, students will identify factors that can shift a market into disequilibrium. Students will be able to identify and/or define the following terms: Disequilibrium Surplus Shortage ...

Economics 11

... engineers would have to rise, so that couldn’t happen. If the supply fell, then wages would rise and the number of engineers would fall, so that’s the answer (d). If demand and supply both increased, we would have more engineers, but the wage could have risen or fallen. 5. In Banda Aceh the price of ...

... engineers would have to rise, so that couldn’t happen. If the supply fell, then wages would rise and the number of engineers would fall, so that’s the answer (d). If demand and supply both increased, we would have more engineers, but the wage could have risen or fallen. 5. In Banda Aceh the price of ...

Chapter 12 - Pegasus @ UCF

... plus lecture drawings. Note Figure 12.6 covers all possibilities by assuming 3 different market prices(P1, P2, P3) ...

... plus lecture drawings. Note Figure 12.6 covers all possibilities by assuming 3 different market prices(P1, P2, P3) ...

Chapter 1

... Be able to describe the following four potential pitfalls in economic thinking: Measuring costs and benefits as proportions Ignoring implicit costs Failure to think at the margin Be able to explain the difference between normative and positive economics. Why a market system, in which individual firm ...

... Be able to describe the following four potential pitfalls in economic thinking: Measuring costs and benefits as proportions Ignoring implicit costs Failure to think at the margin Be able to explain the difference between normative and positive economics. Why a market system, in which individual firm ...

Assignment Guide: Unit II

... Objectives and Key Terms—You must be able to: 1) Define a market. 2) Define demand and state the law of demand. 3) Graph the demand curve when given a demand schedule. 4) Explain the difference between individual demand and market demand. 5) Differentiate between a change in demand and a change in q ...

... Objectives and Key Terms—You must be able to: 1) Define a market. 2) Define demand and state the law of demand. 3) Graph the demand curve when given a demand schedule. 4) Explain the difference between individual demand and market demand. 5) Differentiate between a change in demand and a change in q ...

Chapter 10: Monopoly and Monopsony • Objectives – By the end of

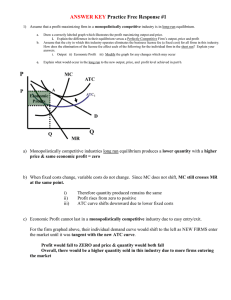

... o Explain how the problems facing monopolistically competitive firms change between the short and long run both verbally and graphically. You should also be able to compare monopolistic competition with the outcomes of perfectly competitive markets. o Graph the deadweight loss that can be associated ...

... o Explain how the problems facing monopolistically competitive firms change between the short and long run both verbally and graphically. You should also be able to compare monopolistic competition with the outcomes of perfectly competitive markets. o Graph the deadweight loss that can be associated ...

price determination

... Many buyers/Many Sellers – Many consumers with the willingness and ability to buy the product at a certain price, Many producers with the willingness and ability to supply the product at a certain price. Homogeneous Products – The products of the different firms are EXACTLY the same, e.g. fruit. Low ...

... Many buyers/Many Sellers – Many consumers with the willingness and ability to buy the product at a certain price, Many producers with the willingness and ability to supply the product at a certain price. Homogeneous Products – The products of the different firms are EXACTLY the same, e.g. fruit. Low ...

econ2000: intermediate microeconomics i – 2012/13

... it is clear that he or she can manage to get a higher utility by spending differently. ...

... it is clear that he or she can manage to get a higher utility by spending differently. ...

ceteris paribus

... Supply and demand model Single most useful tool of economic analysis. Explains how price of goods and the quantity bought and sold are determined in (certain kinds of) markets. Remember: The point is to be able to make conditional predictions: How will price and quantity for a particular good be aff ...

... Supply and demand model Single most useful tool of economic analysis. Explains how price of goods and the quantity bought and sold are determined in (certain kinds of) markets. Remember: The point is to be able to make conditional predictions: How will price and quantity for a particular good be aff ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑