08ETT Chapter 07

... Click the Return button in a feature to return to the main presentation. Click the Economics Online button to access online textbook features. Click the Reference Atlas button to access the Interactive Reference Atlas. Click the Exit button or press the Escape key [Esc] to end the chapter slide show ...

... Click the Return button in a feature to return to the main presentation. Click the Economics Online button to access online textbook features. Click the Reference Atlas button to access the Interactive Reference Atlas. Click the Exit button or press the Escape key [Esc] to end the chapter slide show ...

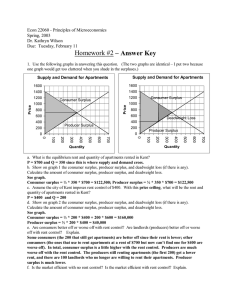

Homework #2 – Answer Key

... e. Who has the higher tax incidence of this tax? Explain what we mean by tax incidence. Consumers have the higher tax incidence. Their price goes from $.80 with no tax to $1.20 with the tax, an increase of $0.40. Supply price goes from $.80 with no tax to $.60 with the tax (consumer pays $1.20 and . ...

... e. Who has the higher tax incidence of this tax? Explain what we mean by tax incidence. Consumers have the higher tax incidence. Their price goes from $.80 with no tax to $1.20 with the tax, an increase of $0.40. Supply price goes from $.80 with no tax to $.60 with the tax (consumer pays $1.20 and . ...

California Standards for the Teaching of Social Studies

... 1. Examine the causal relationship between scarcity and the need for choices. 2. Explain opportunity cost and marginal benefit and marginal cost. 3. Identify the difference between monetary and nonmonetary incentives and how changes in incentives cause changes in behavior. 4. Evaluate the role of pr ...

... 1. Examine the causal relationship between scarcity and the need for choices. 2. Explain opportunity cost and marginal benefit and marginal cost. 3. Identify the difference between monetary and nonmonetary incentives and how changes in incentives cause changes in behavior. 4. Evaluate the role of pr ...

Answer to Quiz #4

... d. (1 point) Suppose this monopolist practices first degree price discrimination. How many units of the good will the perfect price discriminating monopolist produce? Explain this choice of output. Answer: The perfect price discriminating monopolist charges different prices for each consumer. The de ...

... d. (1 point) Suppose this monopolist practices first degree price discrimination. How many units of the good will the perfect price discriminating monopolist produce? Explain this choice of output. Answer: The perfect price discriminating monopolist charges different prices for each consumer. The de ...

hw5 scheme

... b. The decline in the price of stereos increases consumer surplus from area A to A + B + C + D, an increase in the amount B + C + D. Prior to the shift in supply, producer surplus was areas B + E (the area above the supply curve and below the price). After the shift in supply, producer surplus is ar ...

... b. The decline in the price of stereos increases consumer surplus from area A to A + B + C + D, an increase in the amount B + C + D. Prior to the shift in supply, producer surplus was areas B + E (the area above the supply curve and below the price). After the shift in supply, producer surplus is ar ...

Demand_ Identifying what consumers want and need File

... Factors affecting demand - incomes • You get paid – which is nice • Then you have to pay your bills like rent and food (can you think of any other regular bills?) • What is left is called disposable income • As your disposable income rises you will demand more NORMAL goods and some LUXURY goods • A ...

... Factors affecting demand - incomes • You get paid – which is nice • Then you have to pay your bills like rent and food (can you think of any other regular bills?) • What is left is called disposable income • As your disposable income rises you will demand more NORMAL goods and some LUXURY goods • A ...

The Demand Curve for Output

... cut again sometime in the future, and may decide to postpone purchases until it happens again. The opposite can happen if the firm temporarily raises price. It may encourage some customers to try substitutes, which they may find suit them better than the original product. Or it may encourage custome ...

... cut again sometime in the future, and may decide to postpone purchases until it happens again. The opposite can happen if the firm temporarily raises price. It may encourage some customers to try substitutes, which they may find suit them better than the original product. Or it may encourage custome ...

Economics 441: Arvind Panagariya

... Determine the supply of apples relative to the supply of bananas at each relative price of apples in terms of bananas. The lowest relative price at which apples are harvested is 3/2 bananas per apple. The relative supply curve is flat at this price. The maximum number of apples supplied at the price ...

... Determine the supply of apples relative to the supply of bananas at each relative price of apples in terms of bananas. The lowest relative price at which apples are harvested is 3/2 bananas per apple. The relative supply curve is flat at this price. The maximum number of apples supplied at the price ...

Economics 441: Arvind Panagariya

... Determine the supply of apples relative to the supply of bananas at each relative price of apples in terms of bananas. The lowest relative price at which apples are harvested is 3/2 bananas per apple. The relative supply curve is flat at this price. The maximum number of apples supplied at the price ...

... Determine the supply of apples relative to the supply of bananas at each relative price of apples in terms of bananas. The lowest relative price at which apples are harvested is 3/2 bananas per apple. The relative supply curve is flat at this price. The maximum number of apples supplied at the price ...

Price Elasticity of Demand - Business-TES

... price increases to $75 and the number of products sold falls to 450. The firm sells 1200 products at $44. The price decreases to $37 and the number of products sold increases to 1365. What happens to revenue in each of these cases? What is the PED in each of these cases? IGCSE ECONOMICS ...

... price increases to $75 and the number of products sold falls to 450. The firm sells 1200 products at $44. The price decreases to $37 and the number of products sold increases to 1365. What happens to revenue in each of these cases? What is the PED in each of these cases? IGCSE ECONOMICS ...

Econ 101, section 6, S05

... d. a marginal abatement. 25. The Acme paper company owns two factories, factory A and factory B, along the Wolf River. Currently, each factory dumps 500 tons of toxins per year into the river, polluting it. The EPA has ordered Acme to reduce its emissions to a total of 400 tons per year for the two ...

... d. a marginal abatement. 25. The Acme paper company owns two factories, factory A and factory B, along the Wolf River. Currently, each factory dumps 500 tons of toxins per year into the river, polluting it. The EPA has ordered Acme to reduce its emissions to a total of 400 tons per year for the two ...

Lecture Notes 5 on sections of chapters 3 and 4

... – How much households would like to buy when they take into account the opportunity cost of their decisions? ...

... – How much households would like to buy when they take into account the opportunity cost of their decisions? ...

price floors. - University of Nevada, Reno

... • In the short run, some inputs are fixed, so supply is difficult to change, while in the long run, all inputs are variable. – As with demand, short-run elasticities of supply are lower than long-run elasticities of supply. – Once a farm crop is planted, no more can be produced in that growing cycle ...

... • In the short run, some inputs are fixed, so supply is difficult to change, while in the long run, all inputs are variable. – As with demand, short-run elasticities of supply are lower than long-run elasticities of supply. – Once a farm crop is planted, no more can be produced in that growing cycle ...

price. - Cloudfront.net

... increases the use of the other Price of complement goes up - curve shifts left; Price of complement goes down - curve shifts right Change in Expectations: If you expect something better to come out - curve shifts left; If you expect something to be scarce in the future - curve shifts right Number of ...

... increases the use of the other Price of complement goes up - curve shifts left; Price of complement goes down - curve shifts right Change in Expectations: If you expect something better to come out - curve shifts left; If you expect something to be scarce in the future - curve shifts right Number of ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑