Chapter 11 Perfect Competition

... Consumers maximize utility given budget restriction No excess demand or supply (demand = supply) ...

... Consumers maximize utility given budget restriction No excess demand or supply (demand = supply) ...

Long Run Market Supply Curve

... • We have calculated a point at which the market will be in long run equilibrium. • This is a point on the long run market supply curve. Definition: The Long Run Market Supply Curve tells us the total quantity of output that will be supplied at various market prices, assuming that all long run ...

... • We have calculated a point at which the market will be in long run equilibrium. • This is a point on the long run market supply curve. Definition: The Long Run Market Supply Curve tells us the total quantity of output that will be supplied at various market prices, assuming that all long run ...

Topic Homework Sets - University of Nevada, Las Vegas

... What factors do consumers take into consideration in making their consumption choices? Show the possible equilibrium and disequilibrium conditions for a consumer in the single alternative case; show this case graphically. Show the possible equilibrium and disequilibrium conditions for a consumer in ...

... What factors do consumers take into consideration in making their consumption choices? Show the possible equilibrium and disequilibrium conditions for a consumer in the single alternative case; show this case graphically. Show the possible equilibrium and disequilibrium conditions for a consumer in ...

ECON 100:11 Monopoly Monopoly Monopoly is a market structure

... no one else what to get a piece of the pie? Here are some reasons for the existence of barriers to entry: 1. Economies of Scale: When production is characterized by increasing returns to scale such that the larger the firm becomes, the more cost effective it becomes for it to produce output. This th ...

... no one else what to get a piece of the pie? Here are some reasons for the existence of barriers to entry: 1. Economies of Scale: When production is characterized by increasing returns to scale such that the larger the firm becomes, the more cost effective it becomes for it to produce output. This th ...

Document

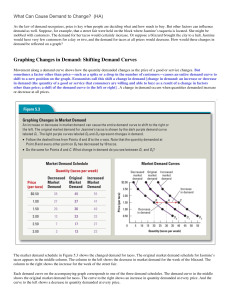

... DEMAND AND SUPPLY • SHIFTS IN SUPPLY AND DEMAND: – What may cause a change in demand? • more optimistic (pessimistic) investors enter the market • investors income may change • the supply or demand for a complementary product for the stock changes ...

... DEMAND AND SUPPLY • SHIFTS IN SUPPLY AND DEMAND: – What may cause a change in demand? • more optimistic (pessimistic) investors enter the market • investors income may change • the supply or demand for a complementary product for the stock changes ...

Chapter 3 - FSU Blackboard

... out of luck – remember there are many ways to ration goods, price is most efficient). Some generators were taken out of the city and sold in for higher prices in less damaged markets Watch: Stossell Myth 2 – Price Gouging (4:35) ...

... out of luck – remember there are many ways to ration goods, price is most efficient). Some generators were taken out of the city and sold in for higher prices in less damaged markets Watch: Stossell Myth 2 – Price Gouging (4:35) ...

To do today: finish the derivation of the demand curve using

... tells us how much of the good on the y axis we are willing to give up to get more of the x good How do we know this amount? From the MU. Slope of the indifference curve is the ratio MUx/ MUy ...

... tells us how much of the good on the y axis we are willing to give up to get more of the x good How do we know this amount? From the MU. Slope of the indifference curve is the ratio MUx/ MUy ...

Lecture Slides 9

... Any firm facing a downward sloping demand curve Firm picks P and Q on the demand curve Market power comes from factors that limit competition ...

... Any firm facing a downward sloping demand curve Firm picks P and Q on the demand curve Market power comes from factors that limit competition ...

P 1

... • Monopoly power, however, does not guarantee profits. • Profit depends on average cost relative to price. • One firm may have more monopoly power, but lower profits due to high average costs ...

... • Monopoly power, however, does not guarantee profits. • Profit depends on average cost relative to price. • One firm may have more monopoly power, but lower profits due to high average costs ...

Perfect-Competition

... The Demand Curve in Perfect Competition • Since the firm is a price taker and an insignificant part of the total market, the individual firm has no control over the price it can charge. The demand curve, therefore will be “perfectly elastic” (horizontal) at the market price. The firm can sell an in ...

... The Demand Curve in Perfect Competition • Since the firm is a price taker and an insignificant part of the total market, the individual firm has no control over the price it can charge. The demand curve, therefore will be “perfectly elastic” (horizontal) at the market price. The firm can sell an in ...

Schiller, Ch - GEOCITIES.ws

... How do we decide how much of any good to buy? How does a change in the price of a good affect the quantity we purchase or the amount of money we spend on it? Why do we buy certain goods but not others? Demand is the willingness and ability to buy specific quantities of a good at alternative pr ...

... How do we decide how much of any good to buy? How does a change in the price of a good affect the quantity we purchase or the amount of money we spend on it? Why do we buy certain goods but not others? Demand is the willingness and ability to buy specific quantities of a good at alternative pr ...

Click to edit Master title style - McGraw-Hill

... The law of demand says: An increase in price causes a decrease in quantity demanded (and vice-versa) But how much does quantity demanded change in response to a change in price? Elasticity gives us a measure of responsiveness ...

... The law of demand says: An increase in price causes a decrease in quantity demanded (and vice-versa) But how much does quantity demanded change in response to a change in price? Elasticity gives us a measure of responsiveness ...

MULTIPLE CHOICE 1. In general, elasticity is a measure of a. the

... How does the concept of elasticity allow us to improve upon our understanding of supply and demand? a. Elasticity allows us to analyze supply and demand with greater precision than would be the case in the absence of the elasticity concept. b. Elasticity provides us with a better rationale for state ...

... How does the concept of elasticity allow us to improve upon our understanding of supply and demand? a. Elasticity allows us to analyze supply and demand with greater precision than would be the case in the absence of the elasticity concept. b. Elasticity provides us with a better rationale for state ...

MATH101 06SP Final

... Please show all your work! No partial credit will be given for incorrect answers with no work shown. Please draw a box around your final answer. Calculators are permitted, but no notes, text, laptops, PDAs, or electronic dictionaries. Cell phones should be muted and left in your pocket or bag. ...

... Please show all your work! No partial credit will be given for incorrect answers with no work shown. Please draw a box around your final answer. Calculators are permitted, but no notes, text, laptops, PDAs, or electronic dictionaries. Cell phones should be muted and left in your pocket or bag. ...

Unit 2: Supply, Demand, and Consumer Choice

... start to decrease • In other words, the more you buy of ANY GOOD the less satisfaction you get from each new unit. Discussion Questions: 1. What does this have to do with the Law of Demand? ...

... start to decrease • In other words, the more you buy of ANY GOOD the less satisfaction you get from each new unit. Discussion Questions: 1. What does this have to do with the Law of Demand? ...

Demand and Supply

... • The theory of demand and supply is a simple example of an economic theory • It can be used to make predictions about the price and quantity of some commodity • In a free-market economy, most economic decisions are guided by prices • Therefore, without a reliable theory of prices, you will get nowh ...

... • The theory of demand and supply is a simple example of an economic theory • It can be used to make predictions about the price and quantity of some commodity • In a free-market economy, most economic decisions are guided by prices • Therefore, without a reliable theory of prices, you will get nowh ...

Demand Schedule for Coffee Beans

... economists talk of increasing or decreasing supply, they mean shifts of the supply curve—a change in the quantity supplied at any given price. 8. There are five main factors that shift the supply curve: • A change in input prices • A change in the prices of related goods and services • A change in t ...

... economists talk of increasing or decreasing supply, they mean shifts of the supply curve—a change in the quantity supplied at any given price. 8. There are five main factors that shift the supply curve: • A change in input prices • A change in the prices of related goods and services • A change in t ...

Supply and demand

In microeconomics, supply and demand is an economic model of price determination in a market. It concludes that in a competitive market, the unit price for a particular good, or other traded item such as labor or liquid financial assets, will vary until it settles at a point where the quantity demanded (at the current price) will equal the quantity supplied (at the current price), resulting in an economic equilibrium for price and quantity transacted.The four basic laws of supply and demand are: If demand increases (demand curve shifts to the right) and supply remains unchanged, a shortage occurs, leading to a higher equilibrium price. If demand decreases (demand curve shifts to the left) and supply remains unchanged, a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply increases (supply curve shifts to the right), a surplus occurs, leading to a lower equilibrium price. If demand remains unchanged and supply decreases (supply curve shifts to the left), a shortage occurs, leading to a higher equilibrium price.↑