Supply and Demand

... social settings. One such natural law is the law of demand, which relates the price of a good to the quantity of that good demanded. According to the law of demand, the quantity of a good or service demanded varies inversely with its price, ceteris paribus. More directly, the law of demand says that ...

... social settings. One such natural law is the law of demand, which relates the price of a good to the quantity of that good demanded. According to the law of demand, the quantity of a good or service demanded varies inversely with its price, ceteris paribus. More directly, the law of demand says that ...

Price elasticity of demand - University of Maryland Department of

... • If there are only two firms in the market before the merger, then the proposed transactions would create a monopoly and is usually prohibited. • What determines the market though? Copyright © 2004 South-Western/Thomson Learning ...

... • If there are only two firms in the market before the merger, then the proposed transactions would create a monopoly and is usually prohibited. • What determines the market though? Copyright © 2004 South-Western/Thomson Learning ...

MC=MR, or Cost Functions and the Theory of the Firm (pages 13-30)

... Formulas (for competitive market): ............................................................................................................................................ 42 (for monopoly) .......................................................................................................... ...

... Formulas (for competitive market): ............................................................................................................................................ 42 (for monopoly) .......................................................................................................... ...

Ch04

... to the price, because firms supplying goods and services want to increase their profits, and the higher the price per unit, the greater the profitability generated by supplying more of that good or service. Also, if costs are rising for producers as they produce more units, they must receive a highe ...

... to the price, because firms supplying goods and services want to increase their profits, and the higher the price per unit, the greater the profitability generated by supplying more of that good or service. Also, if costs are rising for producers as they produce more units, they must receive a highe ...

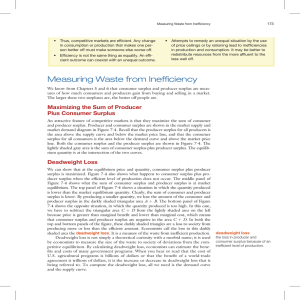

Deadweight Loss

... producing more or less than the efficient amount. Economists call the loss in this darkly shaded area the deadweight loss. It is a measure of the waste from inefficient production. Deadweight loss is not simply a theoretical curiosity with a morbid name; it is used by economists to measure the size ...

... producing more or less than the efficient amount. Economists call the loss in this darkly shaded area the deadweight loss. It is a measure of the waste from inefficient production. Deadweight loss is not simply a theoretical curiosity with a morbid name; it is used by economists to measure the size ...

Value pricing

... Price - definition The amount of money charged for a product or service, or the sum of all the values that consumers/customers exchange for the benefits of having or using the product or service. ...

... Price - definition The amount of money charged for a product or service, or the sum of all the values that consumers/customers exchange for the benefits of having or using the product or service. ...

lecture 9 - WordPress @ VIU Sites

... competitive markets. One distinguishing feature is the absence of strategic interaction among the firms (in monopoly markets, strategic interaction is irrelevant since only one firms exists). • This chapter focuses on how managers select the optimal price and quantity in the following market oligopo ...

... competitive markets. One distinguishing feature is the absence of strategic interaction among the firms (in monopoly markets, strategic interaction is irrelevant since only one firms exists). • This chapter focuses on how managers select the optimal price and quantity in the following market oligopo ...

CHAPTER OVERVIEW

... monopolist charges the price that consumers will pay for that output level. 3. Allocative efficiency is not achieved because price (what product is worth to consumers) is above marginal cost (opportunity cost of product). Ideally, output should expand to a level where price = marginal revenue = marg ...

... monopolist charges the price that consumers will pay for that output level. 3. Allocative efficiency is not achieved because price (what product is worth to consumers) is above marginal cost (opportunity cost of product). Ideally, output should expand to a level where price = marginal revenue = marg ...

PDF

... import protection regime, the relevant price faced by foreign pork suppliers is determined by their respective marginal cost given the import quantity demanded. As smaller quantities of pork are demanded under an SG, total revenue (and net revenue, too) of foreign pork suppliers declines because bot ...

... import protection regime, the relevant price faced by foreign pork suppliers is determined by their respective marginal cost given the import quantity demanded. As smaller quantities of pork are demanded under an SG, total revenue (and net revenue, too) of foreign pork suppliers declines because bot ...

Chapter 5

... Instructor's Manual 69 of other goods could reimburse consumers of computers for their loss in benefits and still be better off. Net benefits, and hence efficiency, will increase. At any point where the supply price is greater than the demand price, net benefit can be increased by reallocating re ...

... Instructor's Manual 69 of other goods could reimburse consumers of computers for their loss in benefits and still be better off. Net benefits, and hence efficiency, will increase. At any point where the supply price is greater than the demand price, net benefit can be increased by reallocating re ...

Topic 3.1b – Long-Run Labour Demand Professor H.J. Schuetze

... The main determinants of the elasticity of demand are (Marshall’s rule): (i) The availability of substitute inputs (ii) The elasticity of supply of substitute output (iii) The elasticity of demand for the output (iv) The ratio of labour cost to total cost We will discuss these separately – discussin ...

... The main determinants of the elasticity of demand are (Marshall’s rule): (i) The availability of substitute inputs (ii) The elasticity of supply of substitute output (iii) The elasticity of demand for the output (iv) The ratio of labour cost to total cost We will discuss these separately – discussin ...

presentation source

... The price at which the firm is indifferent between operating and shutting down: point ‘s’ of the following diagram. If the total revenue is less than variable cost, the benefit of operating the facility is less than the cost; irrational to continue operating.. ...

... The price at which the firm is indifferent between operating and shutting down: point ‘s’ of the following diagram. If the total revenue is less than variable cost, the benefit of operating the facility is less than the cost; irrational to continue operating.. ...

Problems compendium ie

... Suppose that the domestic demand (D) and supply (S) for peanuts in the small country Home are given by D: Q = 400 – 10P and S: Q = 50 + 4P. a. Derive the country’s import demand curve for peanuts. Draw the graphs for the domestic and import markets. Briefly explain. b. What are the levels of domesti ...

... Suppose that the domestic demand (D) and supply (S) for peanuts in the small country Home are given by D: Q = 400 – 10P and S: Q = 50 + 4P. a. Derive the country’s import demand curve for peanuts. Draw the graphs for the domestic and import markets. Briefly explain. b. What are the levels of domesti ...

Elastic - McGraw Hill Higher Education

... Meaning the amount of crime that drug users commit depends not on the quantity of drugs they consume but rather on their total expenditures • How responsive is quantity demanded to price? ...

... Meaning the amount of crime that drug users commit depends not on the quantity of drugs they consume but rather on their total expenditures • How responsive is quantity demanded to price? ...

Solutions Seminar1 Exercise 1 – Competitive market with

... A confident students may go straight to the Hotelling Rule, but a more elaborate approach would be to formulate the profit maximization problem as a Hotelling control theoretic problem a sin lecture 1, trying to get everything right. The price path should be described or explained, which is most con ...

... A confident students may go straight to the Hotelling Rule, but a more elaborate approach would be to formulate the profit maximization problem as a Hotelling control theoretic problem a sin lecture 1, trying to get everything right. The price path should be described or explained, which is most con ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.