Student ID Name Microeconomics Exercises MULTIPLE CHOICE

... In 2001, the adjustable gastric banding system, commonly known as a lap band, was approved by the FDA for use in the United States. Surgically implanted, the lap band helps a person gradually lose and control weight by reducing the amount of food intake. Serious medical conditions, such as diabetes ...

... In 2001, the adjustable gastric banding system, commonly known as a lap band, was approved by the FDA for use in the United States. Surgically implanted, the lap band helps a person gradually lose and control weight by reducing the amount of food intake. Serious medical conditions, such as diabetes ...

Eco 284

... have completed the task, then you will convince yourself that you can and have learned some complex material. Be patient with yourself and your teammate, and the rewards will come through. Complete the following questions. Label all graphs completely. 10 points each. 1. Keeping in mind the MRS, expl ...

... have completed the task, then you will convince yourself that you can and have learned some complex material. Be patient with yourself and your teammate, and the rewards will come through. Complete the following questions. Label all graphs completely. 10 points each. 1. Keeping in mind the MRS, expl ...

Answers to Homework #1

... (e) The degree of gain Bill and Bob individually experience depends on how they split their total production. However, both of them gain from specialization and trade because otherwise, they would not cooperate. This is a simple example of gains from trade. ...

... (e) The degree of gain Bill and Bob individually experience depends on how they split their total production. However, both of them gain from specialization and trade because otherwise, they would not cooperate. This is a simple example of gains from trade. ...

Assignment 1 Dute Sept 13 2002

... there is a new equilibrium price that will be higher. Once all factors have been taken into account the equilibrium price is reached by a movement along the curve. This is always the case, the shift of the curve happens, then the movement along the curve is kind of like s settling point until the eq ...

... there is a new equilibrium price that will be higher. Once all factors have been taken into account the equilibrium price is reached by a movement along the curve. This is always the case, the shift of the curve happens, then the movement along the curve is kind of like s settling point until the eq ...

Supply - Images

... Cause for a change in supply= Number of Factors, such as: 1. Change in Technology 2. Change in the Cost of inputs ...

... Cause for a change in supply= Number of Factors, such as: 1. Change in Technology 2. Change in the Cost of inputs ...

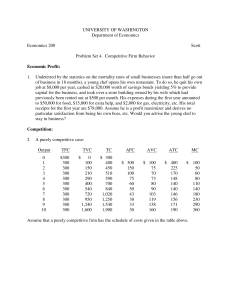

Equilibrium in Perfectly Competitive Markets

... of short run equilibria with higher and higher quantities, and lower and lower prices. The economy stops adjusting when the price falls back to min(ATC), and we are back in long run equilibrium. Notice that in the long run, an increase in demand does not provide firms with profits or increase the pr ...

... of short run equilibria with higher and higher quantities, and lower and lower prices. The economy stops adjusting when the price falls back to min(ATC), and we are back in long run equilibrium. Notice that in the long run, an increase in demand does not provide firms with profits or increase the pr ...

Notes3 - Vassar economics

... market demand curve, D. This is an array of pairs of prices and quantities that reflect how much of a good the individuals who compose the market would be willing to purchase at given prices. This market demand curve is an aggregation of the demands of individuals, households, firms, and government. ...

... market demand curve, D. This is an array of pairs of prices and quantities that reflect how much of a good the individuals who compose the market would be willing to purchase at given prices. This market demand curve is an aggregation of the demands of individuals, households, firms, and government. ...

1.2 Linear functions

... •If price of an item increases, then consumers less likely to buy so the demand for the item decreases ...

... •If price of an item increases, then consumers less likely to buy so the demand for the item decreases ...

EC 220 Microeconomics - College of Micronesia

... 19. Define elasticity of demand 20. Define and distinguish between income and substitution effects of a price change. 21. Explain why a consumer will buy more (less) of a commodity when its price falls (rises) by using income and substitution effects. 22. Define marginal utility and state the law of ...

... 19. Define elasticity of demand 20. Define and distinguish between income and substitution effects of a price change. 21. Explain why a consumer will buy more (less) of a commodity when its price falls (rises) by using income and substitution effects. 22. Define marginal utility and state the law of ...

Set 7 Perfect Competition

... firm increases its output from q1 to q2 and its profits become positive (P>AC). The industry is not in long run equilibrium because the firms are earning positive profits. 4. In the long run there will be entry, which will cause supply to increase from s to s1 in the graph above. Price will be drive ...

... firm increases its output from q1 to q2 and its profits become positive (P>AC). The industry is not in long run equilibrium because the firms are earning positive profits. 4. In the long run there will be entry, which will cause supply to increase from s to s1 in the graph above. Price will be drive ...

Day 1 - Mr

... following question. You need to write a one paragraph response, so fill out all of Day 4. There should be little to no talking during the Bellwork. ...

... following question. You need to write a one paragraph response, so fill out all of Day 4. There should be little to no talking during the Bellwork. ...

Peak Oil Economics - University of Dayton

... Low or zero barriers to entry and exit of buyers and sellers Standardized product or resource Near-perfect information ...

... Low or zero barriers to entry and exit of buyers and sellers Standardized product or resource Near-perfect information ...

Supply and Demand Notes

... *Make sure to include: a title, labels for the x and y axis, and numbers that are labeled consistently ...

... *Make sure to include: a title, labels for the x and y axis, and numbers that are labeled consistently ...

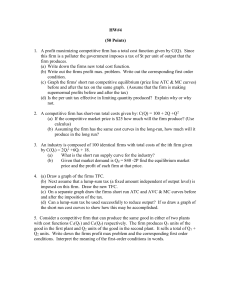

HW3

... firm produces. (a) Write down the firms new total cost function. (b) Write out the firms profit max. problem. Write out the corresponding first order condition. (c) Graph the firms' short run competitive equilibrium (price line ATC & MC curves) before and after the tax on the same graph. (Assume tha ...

... firm produces. (a) Write down the firms new total cost function. (b) Write out the firms profit max. problem. Write out the corresponding first order condition. (c) Graph the firms' short run competitive equilibrium (price line ATC & MC curves) before and after the tax on the same graph. (Assume tha ...

Chapter 4 question 7.

... b) It will have a larger effect 5 years from now because the elasticity of demand for cigarettes will increase over time as people have more time to find substitutes. People will be less price-sensitive in the shorter time span because it is harder to adjust to the price change with a change in smok ...

... b) It will have a larger effect 5 years from now because the elasticity of demand for cigarettes will increase over time as people have more time to find substitutes. People will be less price-sensitive in the shorter time span because it is harder to adjust to the price change with a change in smok ...

Microeconomics: Theory and Applications David Besanko and

... Definition: The Demand Curve plots the aggregate quantity of a good that consumers are willing to buy at different prices, holding constant other demand drivers such as prices of other goods ...

... Definition: The Demand Curve plots the aggregate quantity of a good that consumers are willing to buy at different prices, holding constant other demand drivers such as prices of other goods ...

Demand and supply - Hodder Education

... Bringing demand and supply curves together — a market is in equilibrium when demand and supply are equal. In Figure 3, P* is the unique price at which the quantity that consumers wish to buy is balanced by Q*, the quantity that firms wish to supply. For any price above P*, there is excess supply — f ...

... Bringing demand and supply curves together — a market is in equilibrium when demand and supply are equal. In Figure 3, P* is the unique price at which the quantity that consumers wish to buy is balanced by Q*, the quantity that firms wish to supply. For any price above P*, there is excess supply — f ...

Answers Chapter 4

... the tickets. Some nonprice rationing system was used to allocate the tickets to people willing to pay as little as Px . What a scalper does is pay those near Px more than they paid for the tickets and then sells the tickets to someone nearer or even above P*. Since both the buyers and sellers engage ...

... the tickets. Some nonprice rationing system was used to allocate the tickets to people willing to pay as little as Px . What a scalper does is pay those near Px more than they paid for the tickets and then sells the tickets to someone nearer or even above P*. Since both the buyers and sellers engage ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.