Ch_8_Supply_Demand

... Taxes—businesses are normally taxed on the amount of supply they produce Technology—creating new methods to produce supply. ...

... Taxes—businesses are normally taxed on the amount of supply they produce Technology—creating new methods to produce supply. ...

w05ex2 - Rose

... B. The output of the typical firm increases and the typical firm earns economic profits. E. Only A and B. C. The short-run market supply curve shifts to the right. ___ 11. Assume a perfectly competitive industry was initially in long-run equilibrium, demand increased and the industry moved to its ne ...

... B. The output of the typical firm increases and the typical firm earns economic profits. E. Only A and B. C. The short-run market supply curve shifts to the right. ___ 11. Assume a perfectly competitive industry was initially in long-run equilibrium, demand increased and the industry moved to its ne ...

ProbSet1.pdf

... If General Motors increases its production of SUV’s this year, it will have to spend more on advertising. d. If Borders Books increases the number of titles it carries, it will have to reallocate shelf space to accommodate the new titles. ...

... If General Motors increases its production of SUV’s this year, it will have to spend more on advertising. d. If Borders Books increases the number of titles it carries, it will have to reallocate shelf space to accommodate the new titles. ...

Preview Sample 1

... other things being equal. What are these other things that must be equal? In other words, don’t consumers always tend to buy more at lower prices than at higher prices? ...

... other things being equal. What are these other things that must be equal? In other words, don’t consumers always tend to buy more at lower prices than at higher prices? ...

Comparing Equilibrium situations for Monopoly and perfect

... Comparing Equilibrium situations for Monopoly and perfect Competition ...

... Comparing Equilibrium situations for Monopoly and perfect Competition ...

Cameron ECON 100: FIRST MIDTERM (A) Winter 01

... a. the income effect is to increase housing and the substitution effect is to increase housing b. the income effect is to increase housing and the substitution effect is to decrease housing c. the income effect is to decrease housing and the substitution effect is to increase housing d. the income e ...

... a. the income effect is to increase housing and the substitution effect is to increase housing b. the income effect is to increase housing and the substitution effect is to decrease housing c. the income effect is to decrease housing and the substitution effect is to increase housing d. the income e ...

Q - people.vcu.edu

... This chapter presents a second model, the theory of price and quantity determination. This model should be a review for most of you. Nevertheless, it is of prominent importance. The purpose of this model is both explanatory and predictive. It is the primary tool that you can use to infer the effect ...

... This chapter presents a second model, the theory of price and quantity determination. This model should be a review for most of you. Nevertheless, it is of prominent importance. The purpose of this model is both explanatory and predictive. It is the primary tool that you can use to infer the effect ...

College of Administrative Sciences

... Name\ ------------------------------------------------------- Univ. No.\--------------------Serial No.\ -----------------The demand for a product is inelastic with respect to price if: A) consumers are largely unresponsive to a per unit price change. B) the elasticity coefficient is greater than 1. ...

... Name\ ------------------------------------------------------- Univ. No.\--------------------Serial No.\ -----------------The demand for a product is inelastic with respect to price if: A) consumers are largely unresponsive to a per unit price change. B) the elasticity coefficient is greater than 1. ...

UTILITY and DEMAND

... quantity demanded falls and vice versa (other factors being equal). As price increases MU/P falls, so we buy less. If we are consuming at P=MU and price rises then P>MU so we buy less until P=MU. ...

... quantity demanded falls and vice versa (other factors being equal). As price increases MU/P falls, so we buy less. If we are consuming at P=MU and price rises then P>MU so we buy less until P=MU. ...

ECON_CH06_Demand Supply and Prices

... Marketers sometimes overestimate popularity, others underestimate Tickle Me Elmo doll introduced for holidays in 1996 – at first sold slowly at $30; seemed stores would have surplus – fad caught on; shortage developed, price went up – by spring, supply doubled; demand decreased, price dropped to ...

... Marketers sometimes overestimate popularity, others underestimate Tickle Me Elmo doll introduced for holidays in 1996 – at first sold slowly at $30; seemed stores would have surplus – fad caught on; shortage developed, price went up – by spring, supply doubled; demand decreased, price dropped to ...

Supply, Demand, and Market Equilibrium

... shift in supply we are interested in what happens to (P,Q) at equilibrium just as before, but we get different results than if we get a shift of demand. ii. Shift out of Supply Graphically Results: If the supply curve shifts out we get P dropping and Q increasing. This can be seen in the graph below ...

... shift in supply we are interested in what happens to (P,Q) at equilibrium just as before, but we get different results than if we get a shift of demand. ii. Shift out of Supply Graphically Results: If the supply curve shifts out we get P dropping and Q increasing. This can be seen in the graph below ...

The Role of Price in Demand and Supply

... The Impact of Changes in Demand and Supply We have discussed price changes. But in many real situations, there are simultaneous changes in demand and supply. Let us consider an example in the HKSAR property market. The HKSAR government decided to cool down the property market and on 22 February 201 ...

... The Impact of Changes in Demand and Supply We have discussed price changes. But in many real situations, there are simultaneous changes in demand and supply. Let us consider an example in the HKSAR property market. The HKSAR government decided to cool down the property market and on 22 February 201 ...

Chapter 4 Working with Supply and Demand

... c. Since the price ceiling is non-binding, the market will move to equilibrium, where 400 apartments will be rented. There will be neither excess supply nor excess demand. ...

... c. Since the price ceiling is non-binding, the market will move to equilibrium, where 400 apartments will be rented. There will be neither excess supply nor excess demand. ...

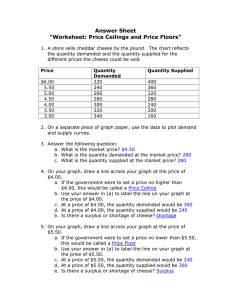

5 - The Citadel

... Equilibrium Price for a Consumer Good Hint: Never say "demand" in place of "quantity demanded" or "supply" in place of "quantity supplied." The equilibrium price is the price where the quantity demanded is equal to the quantity supplied for a particular good or service. That implies that the equilib ...

... Equilibrium Price for a Consumer Good Hint: Never say "demand" in place of "quantity demanded" or "supply" in place of "quantity supplied." The equilibrium price is the price where the quantity demanded is equal to the quantity supplied for a particular good or service. That implies that the equilib ...

Econ 101, section 6, S05

... Choose the single best answer for each question. 1. When an economy cannot produce all the goods and services people wish to have it is said to be experiencing a. externalities. b. market failure. *. scarcity. d. excludability. 2. Which of the following is an example of a normative statement? a. If ...

... Choose the single best answer for each question. 1. When an economy cannot produce all the goods and services people wish to have it is said to be experiencing a. externalities. b. market failure. *. scarcity. d. excludability. 2. Which of the following is an example of a normative statement? a. If ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.