MANAGERIAL ECONOMICS 11th Edition

... Profit Maximization in Competitive Markets Marginal Cost and Firm Supply Competitive Market Supply Curve Competitive Market Equilibrium ...

... Profit Maximization in Competitive Markets Marginal Cost and Firm Supply Competitive Market Supply Curve Competitive Market Equilibrium ...

Supply and Demand

... than Pe. • This generates a surplus (Qs > Qd). • The market mechanism cannot clear the market. • A permanent surplus exists. ...

... than Pe. • This generates a surplus (Qs > Qd). • The market mechanism cannot clear the market. • A permanent surplus exists. ...

SL 151 Name ______ CM ______ Bremmer I May 12, 2006 3rd In

... Which of the following statements about the loanable funds model is correct? A shortage will cause the nominal interest rate to fall. During times of growing real GDP, the demand for loanable funds shifts to the left and the nominal interest rate falls. A decrease in expected inflation causes a decr ...

... Which of the following statements about the loanable funds model is correct? A shortage will cause the nominal interest rate to fall. During times of growing real GDP, the demand for loanable funds shifts to the left and the nominal interest rate falls. A decrease in expected inflation causes a decr ...

Document

... 1. A survey indicated that chocolate ice cream is America’s favorite ice-cream flavor. For each of the following, indicate the possible effects on demand and/or supply and equilibrium price and quantity of chocolate ice cream. a. A severe drought in the Midwest causes dairy farmers to reduce the num ...

... 1. A survey indicated that chocolate ice cream is America’s favorite ice-cream flavor. For each of the following, indicate the possible effects on demand and/or supply and equilibrium price and quantity of chocolate ice cream. a. A severe drought in the Midwest causes dairy farmers to reduce the num ...

4 EQUILIBRIUM PRICES

... greater than the amount supplied by sellers, there is excess demand, and market price will tend to rise. On the other hand, if the amount demanded by consumers is less than the amount supplied by sellers, excess demand is negative, and market price will fall. A market is in equilibrium if excess dem ...

... greater than the amount supplied by sellers, there is excess demand, and market price will tend to rise. On the other hand, if the amount demanded by consumers is less than the amount supplied by sellers, excess demand is negative, and market price will fall. A market is in equilibrium if excess dem ...

4 EQUILIBRIUM PRICES

... greater than the amount supplied by sellers, there is excess demand, and market price will tend to rise. On the other hand, if the amount demanded by consumers is less than the amount supplied by sellers, excess demand is negative, and market price will fall. A market is in equilibrium if excess dem ...

... greater than the amount supplied by sellers, there is excess demand, and market price will tend to rise. On the other hand, if the amount demanded by consumers is less than the amount supplied by sellers, excess demand is negative, and market price will fall. A market is in equilibrium if excess dem ...

Chapter 17 Lecture Notes (no voice)

... at the point where average total cost is minimized, which is the efficient scale of the firm. There is excess capacity in monopolistic competition in the long run. o In monopolistic competition, output is less than the efficient scale of perfect competition. For a competitive firm, price equals marg ...

... at the point where average total cost is minimized, which is the efficient scale of the firm. There is excess capacity in monopolistic competition in the long run. o In monopolistic competition, output is less than the efficient scale of perfect competition. For a competitive firm, price equals marg ...

Economics Review

... Producers & consumers motivated by self-interest. To make more money, producers try to make goods and services that consumers want. Producers engage in competition (by lowering prices, advertising, improving quality) to get more people to buy goods. Consumers serve self interest by purchasing the be ...

... Producers & consumers motivated by self-interest. To make more money, producers try to make goods and services that consumers want. Producers engage in competition (by lowering prices, advertising, improving quality) to get more people to buy goods. Consumers serve self interest by purchasing the be ...

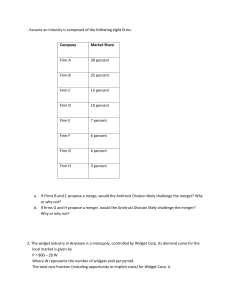

Assume an industry is composed of the following eight firms

... 2. The widget Industry in Anytown is a monopoly, controlled by Widget Corp. Its demand curve for the local market is given by P = 800 – 20 W Where W represents the number of widgets sold per period. The total cost function (including opportunity or implicit costs) for Widget Corp. is ...

... 2. The widget Industry in Anytown is a monopoly, controlled by Widget Corp. Its demand curve for the local market is given by P = 800 – 20 W Where W represents the number of widgets sold per period. The total cost function (including opportunity or implicit costs) for Widget Corp. is ...

Homework #2

... c. Calculate the cost to consumers with the price floor. Shade this area on the graph in part a.) in a different color. d. Now, using the same demand and supply schedules, draw a new graph where the government uses a price subsidy program instead of a price floor program. There is no longer a cost f ...

... c. Calculate the cost to consumers with the price floor. Shade this area on the graph in part a.) in a different color. d. Now, using the same demand and supply schedules, draw a new graph where the government uses a price subsidy program instead of a price floor program. There is no longer a cost f ...

Part 2 Economic Decisions and Systems

... Resources are owned and controlled by the people of the country Businesses & Individuals answer the 3 Q’s in the market place Marketplace is anywhere goods & services are exchanged They vote with their $$$’s ...

... Resources are owned and controlled by the people of the country Businesses & Individuals answer the 3 Q’s in the market place Marketplace is anywhere goods & services are exchanged They vote with their $$$’s ...

Monopolies MONOPOLY Pure Monopolies

... • What is the relationship: 1) between TR and MR? • 2) between P and MR? 1) TR is maximized when MR = 0 Since TR rises while P falls =====> Demand is elastic 2) MR does not equal P as it does in perfect competition MR < P always in a monopolist setting Using these 2 facts, what is the monopolists pr ...

... • What is the relationship: 1) between TR and MR? • 2) between P and MR? 1) TR is maximized when MR = 0 Since TR rises while P falls =====> Demand is elastic 2) MR does not equal P as it does in perfect competition MR < P always in a monopolist setting Using these 2 facts, what is the monopolists pr ...

Exercise on “Supply and demand” - E-Course

... Try to fill in the gaps. If you've only heard of one economics 1) c_________, it's probably supply and demand. Eventually we'll want to derive this concept 2) ________ basic assumptions about utility and cost functions, but for now I'll just go through the 2-minute version. Let's start with supply. ...

... Try to fill in the gaps. If you've only heard of one economics 1) c_________, it's probably supply and demand. Eventually we'll want to derive this concept 2) ________ basic assumptions about utility and cost functions, but for now I'll just go through the 2-minute version. Let's start with supply. ...

MARKET EQUILIBRIUM PRICE NOTES

... have been made on the government to do something about prices that are “_____ ______” or “______ ______.” The government takes action in these instances to place legal barriers on the market place that will not allow ______ to fall below certain price or to _____ above a certain price. These legal b ...

... have been made on the government to do something about prices that are “_____ ______” or “______ ______.” The government takes action in these instances to place legal barriers on the market place that will not allow ______ to fall below certain price or to _____ above a certain price. These legal b ...

4 - The Citadel

... 2. Give the laws of supply and demand, as they relate to both consumer goods and labor. (Must define relative price, ceteris paribus, households and firms, quantities supplied and demanded.) The Price System The market economic system uses private property and the process of exchange to coordinate t ...

... 2. Give the laws of supply and demand, as they relate to both consumer goods and labor. (Must define relative price, ceteris paribus, households and firms, quantities supplied and demanded.) The Price System The market economic system uses private property and the process of exchange to coordinate t ...

Shift in Demand

... Bell Work Objective: Summarize what cause Demand to shift and the effect on the price and quantity demanded. ...

... Bell Work Objective: Summarize what cause Demand to shift and the effect on the price and quantity demanded. ...

Chapter 26 1. Fly-by-night Corporation is in need of capital funds to

... Fly-by-night Corporation is in need of capital funds to expand its production capacity. It is selling short- and long-term bonds and is issuing shares. You are considering the prospect of helping finance their expansion. ...

... Fly-by-night Corporation is in need of capital funds to expand its production capacity. It is selling short- and long-term bonds and is issuing shares. You are considering the prospect of helping finance their expansion. ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.