Name: Date: ______ 1. An economy is efficient if it is: A) possible to

... 6. The primary difference between a change in supply and a change in the quantity supplied is that: A) a change in quantity supplied is a movement along the supply curve, while a change in supply is a shift in the supply curve. B) both a change in quantity supplied and a change in supply are moveme ...

... 6. The primary difference between a change in supply and a change in the quantity supplied is that: A) a change in quantity supplied is a movement along the supply curve, while a change in supply is a shift in the supply curve. B) both a change in quantity supplied and a change in supply are moveme ...

A movement along a Demand Curve - Business Studies A Level for

... shift in the demand curve changes the equilibrium position. So this increase in incomes has increased demand for coffee from 20 to 40 at a price of £4 ...

... shift in the demand curve changes the equilibrium position. So this increase in incomes has increased demand for coffee from 20 to 40 at a price of £4 ...

Principles of Economics

... Economic goods are scarce or limited in supply. Free goods like air exist in such large quantities. Thus, their market price is zero. Scarcity means that an economic good is not freely available for the taking. Efficiency refers to the use of economic resources to maximize satisfaction with the ...

... Economic goods are scarce or limited in supply. Free goods like air exist in such large quantities. Thus, their market price is zero. Scarcity means that an economic good is not freely available for the taking. Efficiency refers to the use of economic resources to maximize satisfaction with the ...

Demand, Supply and Market Equilibrium

... Law of Supply - as the price of an item rises the quantity supplied will rise; as the price of an item falls quantity supplied will fall. The higher the price of a good, the more incentive they have to sell more, so they produce more. Supply Schedule - chart showing amounts of an item sellers are wi ...

... Law of Supply - as the price of an item rises the quantity supplied will rise; as the price of an item falls quantity supplied will fall. The higher the price of a good, the more incentive they have to sell more, so they produce more. Supply Schedule - chart showing amounts of an item sellers are wi ...

Eco 301 Name

... producers would receive. With the tax, the demand curve shifts down by $5 and the amount producers receive is reduced to PP. However, the amount consumers must pay is PC, which is exactly what they would pay without the tax, P*. Hence, the burden on consumers, PC - P*, is zero, while the burden on p ...

... producers would receive. With the tax, the demand curve shifts down by $5 and the amount producers receive is reduced to PP. However, the amount consumers must pay is PC, which is exactly what they would pay without the tax, P*. Hence, the burden on consumers, PC - P*, is zero, while the burden on p ...

DOC

... Suppose labor productivity differences are the only determinants of comparative advantage and Egypt and Israel each produce only rugs and shoes. In Egypt, 10 rugs or 5 shoes can be produced in a day. In Israel, one day of labor can be used to produce either 4 rugs or 12 shoes. In the scenario above, ...

... Suppose labor productivity differences are the only determinants of comparative advantage and Egypt and Israel each produce only rugs and shoes. In Egypt, 10 rugs or 5 shoes can be produced in a day. In Israel, one day of labor can be used to produce either 4 rugs or 12 shoes. In the scenario above, ...

E3F07A

... information about the next best sector in which to enter the supply of labor. Such time is manifested in unemployment. C. If consumers injured by unsafe products are awarded damages equal to the amount required to make them indifferent to having the injury (and the compensation), it is likely that f ...

... information about the next best sector in which to enter the supply of labor. Such time is manifested in unemployment. C. If consumers injured by unsafe products are awarded damages equal to the amount required to make them indifferent to having the injury (and the compensation), it is likely that f ...

Exam Review 2 Answer key

... b. Government’s tax revenue c. Equilibrium quantity d. Price paid by consumers 15. If the world price of corn is $7 and the domestic price for the U.S. is $5 then a. The U.S. will export corn b. The U.S. will import corn c. The U.S. will import and export corn d. They will stop producing corn 16. If ...

... b. Government’s tax revenue c. Equilibrium quantity d. Price paid by consumers 15. If the world price of corn is $7 and the domestic price for the U.S. is $5 then a. The U.S. will export corn b. The U.S. will import corn c. The U.S. will import and export corn d. They will stop producing corn 16. If ...

Simultaneous Price and Quantity Adjustment in a Single Market

... nonlinear oscillations in physical systems [5, 8, 10, 11], may be of interest in own right and also for the light it sheds on possible commodity cycles, as well; on the question of market stability. It is in fact rather remarkable that these simp facts which relate to the very core of economics, sup ...

... nonlinear oscillations in physical systems [5, 8, 10, 11], may be of interest in own right and also for the light it sheds on possible commodity cycles, as well; on the question of market stability. It is in fact rather remarkable that these simp facts which relate to the very core of economics, sup ...

Pure Monopoly

... Determine the pure monopolist’s economic profit by using one of two methods: Method 1. Find profit per unit by subtracting the average total cost of the profit-maximizing output from the profit-maximizing price. Then multiply the difference by the profit-maximizing output to determine economic profi ...

... Determine the pure monopolist’s economic profit by using one of two methods: Method 1. Find profit per unit by subtracting the average total cost of the profit-maximizing output from the profit-maximizing price. Then multiply the difference by the profit-maximizing output to determine economic profi ...

Pure Monopoly - McGraw Hill Higher Education

... Determine the pure monopolist’s economic profit by using one of two methods: Method 1. Find profit per unit by subtracting the average total cost of the profit-maximizing output from the profit-maximizing price. Then multiply the difference by the profit-maximizing output to determine economic profi ...

... Determine the pure monopolist’s economic profit by using one of two methods: Method 1. Find profit per unit by subtracting the average total cost of the profit-maximizing output from the profit-maximizing price. Then multiply the difference by the profit-maximizing output to determine economic profi ...

ECO 481

... 1. The more sellers, the harder it is to form a cartel. 2. The more non-homogeneous the product, the harder it is to form a cartel. 3. The more excess capacity, the harder it is to form a cartel. ...

... 1. The more sellers, the harder it is to form a cartel. 2. The more non-homogeneous the product, the harder it is to form a cartel. 3. The more excess capacity, the harder it is to form a cartel. ...

Shifts of the Supply Curve

... that the price consumers are willing and able to pay for cell phones begins to rise. • How would this affect your production of cell phones? Would you make more or fewer cell phones? – You would want to make more. ...

... that the price consumers are willing and able to pay for cell phones begins to rise. • How would this affect your production of cell phones? Would you make more or fewer cell phones? – You would want to make more. ...

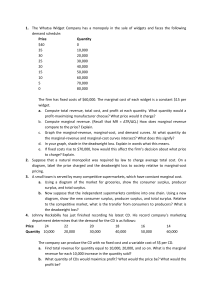

The Whatsa Widget Company has a monopoly in the sale of widgets

... c. Figure 1 shows the marginal-revenue, marginal-cost, and demand curves. The marginal revenue and marginal-cost curves cross at quantities of 20,000 and 30,000. This signifies that the firm maximizes profits in that region. d. The area of deadweight loss is marked “DWL” in the figure. Deadweight lo ...

... c. Figure 1 shows the marginal-revenue, marginal-cost, and demand curves. The marginal revenue and marginal-cost curves cross at quantities of 20,000 and 30,000. This signifies that the firm maximizes profits in that region. d. The area of deadweight loss is marked “DWL” in the figure. Deadweight lo ...

Homework #5

... lighthouses you need to vertically sum the individual demand curves. We vertically sum the demand curves because the good is nonrival: my consumption of the good does not diminish your ability to consume the good. So, the question becomes one of asking how much each of us is willing to contribute to ...

... lighthouses you need to vertically sum the individual demand curves. We vertically sum the demand curves because the good is nonrival: my consumption of the good does not diminish your ability to consume the good. So, the question becomes one of asking how much each of us is willing to contribute to ...

Economic equilibrium

In economics, economic equilibrium is a state where economic forces such as supply and demand are balanced and in the absence of external influences the (equilibrium) values of economic variables will not change. For example, in the standard text-book model of perfect competition, equilibrium occurs at the point at which quantity demanded and quantity supplied are equal. Market equilibrium in this case refers to a condition where a market price is established through competition such that the amount of goods or services sought by buyers is equal to the amount of goods or services produced by sellers. This price is often called the competitive price or market clearing price and will tend not to change unless demand or supply changes and the quantity is called ""competitive quantity"" or market clearing quantity.