- Wasatch Advisors

- Computational Finance

(Module A) – Part II

"Leverage Effect" a Leverage Effect?

! Database!Fatal!Flash!Flaws!No!One! Talks!About! !!

Document 7848212

Document 8533298

Multiple-Choice Quiz (with answer key)

More Than You Ever Wanted to Know About

monte carlo simulation in financial engineering

Monte Carlo Simulation

Money, Banking, and the Fed

Money, Banking, and Financial Markets (Econ 353)

Momentum Securities solutions

Module 8 Strategies for a flat market – Australian Securities

Modification to the Trading Hours

Modeling Asset Prices in Continuous Time

MF2458 Grain Marketing Plans for Farmers

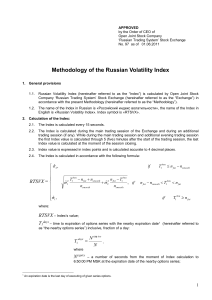

Methodology of the Volatility Index Calculation

Measurement of Market Risk