Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

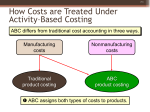

GARY COKINS.,1998, Learning to Love ABC ,Journal of Accountancy,pp.37-39 Absorption Costing: -cost allocation based on labour hours, gallons pounds or other units of output Absorption advantage: Absorption disadvantage: -Companies that use traditional indirect-cost allocations may actually lose money on certain products and customers, even though their accounting systems report them as profitable -as pricing and quotation practices usually rely on the same flawed cost, the errors are perpetuated. -rarely reflects the true cause and effect relationship between indirect and overhead costs and individual products, services, channels or customers. -too many of the costs are lumped together in some categories -the average rates selected for many costs tend to be excessively broad -often irrelevant factors are used to allocate indirect costs. e.g product inspection costs ABC: -a way to translate general ledger data into a format that helps managers make decisions. -once ABC is set up to determine true costs, cost estimating is a natural next step. It begins with forecasts of a products’ output; then, by adding the various cost driver rates for that activity, the total projected costs can be determined. -for that reason, what-if analysis and predictive planning are popular ABC applications. The Rise of ABC -In the past: considered as an expensive management project that only large organizations with extensive resources could undertake -realisation of inaccurate costing information due to the rapid changes in the cost structures during 1980s, direct labour based allocation costing was no longer sufficient -organisations became more complicated, indirect and overhead costs grew at a faster rate than sales or services and displaced the costs of the front-line worker. -expanded service lines and diversification of products as well as the customers and increase in channels -no single volume based allocation method could fairly trace indirect costs into the rich variation of products, service lines and customers. -Sharp rise of competition also contributed to the failure of the traditional methods. -unprofitable products have to be eliminated. -Key Factors to the rapid growth of ABC: decrease in the price of personal computer, more accounting data could be stored and processed. -increase in competition has forced all organizations to focus not just on their top line ~ sales or budget funding, but also their middle line- their costs. -Nowadays: with the proliferation of computers for data gathering and computing plus the recognition that most data for decision making need not be accurate to several decimal places, any organization can implement ABC. The importance for ABC costing -corrects for the limitations of traditional costing by identifying all the work activities and their costs that go into manufacturing a product, delivering a service or performing a process -a clear picture of the total cost of a process comes into view when the individual costs are added up. -distinguish the cost of servicing different customers -a practical solution for problems associated with traditional cost management Argument for ABC: -costing process is just another way to spin financial data -