Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Copyright 1996 Lawrence C. Marsh

PowerPoint Slides

for

Undergraduate Econometrics

by

Lawrence C. Marsh

To accompany: Undergraduate Econometrics

by R. Carter Hill, William E. Griffiths and George G. Judge

Publisher: John Wiley & Sons, 1997

Copyright 1996 Lawrence C. Marsh

Chapter 1

1.1

The Role of

Econometrics

in Economic Analysis

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

The Role of Econometrics

Using Information:

1. Information from economic theory.

2. Information from economic data.

1.2

Copyright 1996 Lawrence C. Marsh

Understanding Economic Relationships:

money supply

Dow-Jones

Stock Index

federal

budget

short term

treasury bills

inflation

trade

deficit

unemployment

power of

labor unions

Federal Reserve

Discount Rate

capital gains tax

crime rate

rent

control

laws

1.3

Copyright 1996 Lawrence C. Marsh

Economic Decisions

To use information effectively:

economic theory

economic data

}

economic

decisions

*Econometrics* helps us combine

economic theory and economic data .

1.4

Copyright 1996 Lawrence C. Marsh

The Consumption Function

1.5

Consumption, c, is some function of income, i :

c = f(i)

For applied econometric analysis

this consumption function must be

specified more precisely.

Copyright 1996 Lawrence C. Marsh

demand, qd, for an individual commodity:

qd = f( p, pc, ps, i )

1.6

demand

p = own price; pc = price of complements;

ps = price of substitutes; i = income

supply, qs, of an individual commodity:

qs = f( p, pc, pf )

supply

p = own price; pc = price of competitive products;

ps = price of substitutes; pf = price of factor inputs

Copyright 1996 Lawrence C. Marsh

How much ?

Listing the variables in an economic relationship is not enough.

For effective policy we must know the amount of change

needed for a policy instrument to bring about the desired

effect:

• By how much should the Federal Reserve

raise interest rates to prevent inflation?

• By how much can the price of football tickets

be increased and still fill the stadium?

1.7

Copyright 1996 Lawrence C. Marsh

Answering the How Much? question

Need to estimate parameters

that are both:

1. unknown

and

2. unobservable

1.8

Copyright 1996 Lawrence C. Marsh

The Statistical Model

Average or systematic behavior

over many individuals or many firms.

Not a single individual or single firm.

Economists are concerned with the

unemployment rate and not whether

a particular individual gets a job.

1.9

Copyright 1996 Lawrence C. Marsh

1.10

The Statistical Model

Actual vs. Predicted Consumption:

Actual = systematic part + random error

Consumption, c, is function, f, of income, i, with error, e:

c = f(i) + e

Systematic part provides prediction, f(i),

but actual will miss by random error, e.

Copyright 1996 Lawrence C. Marsh

The Consumption Function

c = f(i) + e

Need to define f(i) in some way.

To make consumption, c,

a linear function of income, i :

f(i) = b1 + b2 i

The statistical model then becomes:

c = b1 + b2 i + e

1.11

Copyright 1996 Lawrence C. Marsh

1.12

The Econometric Model

y = b 1 + b 2 X2 + b 3 X 3 + e

• Dependent variable, y, is focus of study

(predict or explain changes in dependent variable).

• Explanatory variables, X2 and X3, help us explain

observed changes in the dependent variable.

Copyright 1996 Lawrence C. Marsh

1.13

Statistical Models

Controlled (experimental)

vs.

Uncontrolled (observational)

Controlled experiment (“pure” science) explaining mass, y :

pressure, X2, held constant when varying temperature, X3,

and vice versa.

Uncontrolled experiment (econometrics) explaining consumption, y : price, X2, and income, X3, vary at the same time.

Copyright 1996 Lawrence C. Marsh

1.14

Econometric model

• economic model

economic variables and parameters.

• statistical model

sampling process with its parameters.

• data

observed values of the variables.

Copyright 1996 Lawrence C. Marsh

1.15

The Practice of Econometrics

•

•

•

•

•

•

•

•

•

Uncertainty regarding an outcome.

Relationships suggested by economic theory.

Assumptions and hypotheses to be specified.

Sampling process including functional form.

Obtaining data for the analysis.

Estimation rule with good statistical properties.

Fit and test model using software package.

Analyze and evaluate implications of the results.

Problems suggest approaches for further research.

Copyright 1996 Lawrence C. Marsh

1.16

Note: the textbook uses the following symbol

to mark sections with advanced material:

“Skippy”

Copyright 1996 Lawrence C. Marsh

Chapter 2

2.1

Some Basic

Probability

Concepts

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

Random Variable

random variable:

A variable whose value is unknown until it is observed.

The value of a random variable results from an experiment.

The term random variable implies the existence of some

known or unknown probability distribution defined over

the set of all possible values of that variable.

In contrast, an arbitrary variable does not have a

probability distribution associated with its values.

2.2

Copyright 1996 Lawrence C. Marsh

Controlled experiment values

of explanatory variables are chosen

with great care in accordance with

an appropriate experimental design.

Uncontrolled experiment values

of explanatory variables consist of

nonexperimental observations over

which the analyst has no control.

2.3

Copyright 1996 Lawrence C. Marsh

Discrete Random Variable

discrete random variable:

A discrete random variable can take only a finite

number of values, that can be counted by using

the positive integers.

Example: Prize money from the following

lottery is a discrete random variable:

first prize: $1,000

second prize: $50

third prize: $5.75

since it has only four (a finite number)

(count: 1,2,3,4) of possible outcomes:

$0.00; $5.75; $50.00; $1,000.00

2.4

Copyright 1996 Lawrence C. Marsh

Continuous Random Variable

continuous random variable:

A continuous random variable can take

any real value (not just whole numbers)

in at least one interval on the real line.

Examples:

Gross national product (GNP)

money supply

interest rates

price of eggs

household income

expenditure on clothing

2.5

Copyright 1996 Lawrence C. Marsh

Dummy Variable

A discrete random variable that is restricted

to two possible values (usually 0 and 1) is

called a dummy variable (also, binary or

indicator variable).

Dummy variables account for qualitative differences:

gender (0=male, 1=female),

race (0=white, 1=nonwhite),

citizenship (0=U.S., 1=not U.S.),

income class (0=poor, 1=rich).

2.6

Copyright 1996 Lawrence C. Marsh

2.7

A list of all of the possible values taken

by a discrete random variable along with

their chances of occurring is called a probability

function or probability density function (pdf).

die

one dot

two dots

three dots

four dots

five dots

six dots

x

1

2

3

4

5

6

f(x)

1/6

1/6

1/6

1/6

1/6

1/6

Copyright 1996 Lawrence C. Marsh

A discrete random variable X

has pdf, f(x), which is the probability

that X takes on the value x.

f(x) = P(X=x)

Therefore,

0 < f(x) < 1

If X takes on the n values: x1, x2, . . . , xn,

then f(x1) + f(x2)+. . .+f(xn) = 1.

2.8

Copyright 1996 Lawrence C. Marsh

Probability, f(x), for a discrete random

variable, X, can be represented by height:

0.4

0.3

f(x)

0.2

0.1

0

1

2

3

X

number, X, on Dean’s List of three roommates

2.9

Copyright 1996 Lawrence C. Marsh

2.10

A continuous random variable uses

area under a curve rather than the

height, f(x), to represent probability:

f(x)

red area

0.1324

green area

0.8676

.

.

$34,000

$55,000

per capita income, X, in the United States

X

Copyright 1996 Lawrence C. Marsh

2.11

Since a continuous random variable has an

uncountably infinite number of values,

the probability of one occurring is zero.

P[X=a] = P[a<X<a]=0

Probability is represented by area.

Height alone has no area.

An interval for X is needed to get

an area under the curve.

Copyright 1996 Lawrence C. Marsh

2.12

The area under a curve is the integral of

the equation that generates the curve:

b

P[a<X<b]=

ٍ

a

f(x) dx

For continuous random variables it is the

integral of f(x), and not f(x) itself, which

defines the area and, therefore, the probability.

Copyright 1996 Lawrence C. Marsh

Rules of Summation

n

Rule 1:

Rule 2:

xi = x1 + x2 + . . . + xn

S

i=1

n

n

i=1

i=1

S axi = a S xi

n

Rule 3:

n

n

i=1

i=1

(xi + yi) = S xi + S yi

S

i=1

Note that summation is a linear operator

which means it operates term by term.

2.13

Copyright 1996 Lawrence C. Marsh

2.14

Rules of Summation (continued)

n

Rule 4:

Rule 5:

n

n

i=1

i=1

(axi + byi) = a S xi + b S yi

S

i=1

x

n

= n S xi =

i=1

1

x1 + x2 + . . . + xn

n

The definition of x as given in Rule 5 implies

the following important fact:

n

(xi - x) = 0

S

i=1

Copyright 1996 Lawrence C. Marsh

2.15

Rules of Summation (continued)

n

Rule 6:

f(xi) = f(x1) + f(x2) + . . . + f(xn)

S

i=1

Notation:

n m

Rule 7:

n

Sx f(xi) = Si f(xi) = i =S1 f(xi)

n

[ f(xi,y1) + f(xi,y2)+. . .+ f(xi,ym)]

S S f(xi,yj) = i S

=1

i=1 j=1

The order of summation does not matter :

n m

m n

f(xi,yj)

S S f(xi,yj) =j =S1 i S

=1

i=1 j=1

Copyright 1996 Lawrence C. Marsh

2.16

The Mean of a Random Variable

The mean or arithmetic average of a

random variable is its mathematical

expectation or expected value, EX.

Copyright 1996 Lawrence C. Marsh

Expected Value

2.17

There are two entirely different, but mathematically

equivalent, ways of determining the expected value:

1. Empirically:

The expected value of a random variable, X,

is the average value of the random variable in an

infinite number of repetitions of the experiment.

In other words, draw an infinite number of samples,

and average the values of X that you get.

Copyright 1996 Lawrence C. Marsh

Expected Value

2.18

2. Analytically:

The expected value of a discrete random

variable, X, is determined by weighting all

the possible values of X by the corresponding

probability density function values, f(x), and

summing them up.

In other words:

E[X] = x1f(x1) + x2f(x2) + . . . + xnf(xn)

Copyright 1996 Lawrence C. Marsh

Empirical vs. Analytical

As sample size goes to infinity, the

empirical and analytical methods

will produce the same value.

In the empirical case when the

sample goes to infinity the values

of X occur with a frequency

equal to the corresponding f(x)

in the analytical expression.

2.19

Copyright 1996 Lawrence C. Marsh

2.20

Empirical (sample) mean:

n

x = S xi

i=1

where n is the number of sample observations.

Analytical mean:

n

E[X] = S xi f(xi)

i=1

where n is the number of possible values of xi.

Notice how the meaning of n changes.

Copyright 1996 Lawrence C. Marsh

2.21

The expected value of X:

n

EX =

S

xi f(xi)

i=1

The expected value of X-squared:

2

EX =

n

S

i=1

2

xi f(xi)

It is important to notice that f(xi) does not change!

The expected value of X-cubed:

3

EX =

n

S

i=1

3

xi f(xi)

Copyright 1996 Lawrence C. Marsh

2.22

EX

= 0 (.1) + 1 (.3) + 2 (.3) + 3 (.2) + 4 (.1)

= 1.9

2

2

2

2

2

2

EX = 0 (.1) + 1 (.3) + 2 (.3) + 3 (.2) + 4 (.1)

= 0 + .3 + 1.2 + 1.8 + 1.6

= 4.9

3

3

3

3

3

3

EX = 0 (.1) + 1 (.3) + 2 (.3) + 3 (.2) +4 (.1)

= 0 + .3 + 2.4 + 5.4 + 6.4

= 14.5

Copyright 1996 Lawrence C. Marsh

2.23

n

E[g(X)] =

S

g(xi)

i=1

f(xi)

g(X) = g1(X) + g2(X)

n

E[g(X)] =

S

[

g1(xi) + g2(xi)] f(xi)

i=1

n

E[g(X)] =

n

S

g1(xi) f(xi) +i S

g

(x

)

f(x

)

2

i

i

=1

i=1

E[g(X)] = E[g1(X)] + E[g2(X)]

Copyright 1996 Lawrence C. Marsh

Adding and Subtracting

Random Variables

2.24

E(X+Y) = E(X) + E(Y)

E(X-Y) = E(X) - E(Y)

Copyright 1996 Lawrence C. Marsh

2.25

Adding a constant to a variable will

add a constant to its expected value:

E(X+a) = E(X) + a

Multiplying by constant will multiply

its expected value by that constant:

E(bX) = b E(X)

Copyright 1996 Lawrence C. Marsh

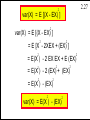

2.26

Variance

var(X) = average squared deviations

around the mean of X.

var(X) = expected value of the squared deviations

around the expected value of X.

2

var(X) = E [(X - EX) ]

Copyright 1996 Lawrence C. Marsh

2.27

2

var(X) = E [(X - EX) ]

2

var(X) = E [(X - EX) ]

2

2

= E [X - 2XEX + (EX) ]

2

2

= E(X ) - 2 EX EX + E (EX)

2

2

2

= E(X ) - 2 (EX) + (EX)

2

2

= E(X ) - (EX)

2

2

var(X) = E(X ) - (EX)

Copyright 1996 Lawrence C. Marsh

2.28

variance of a discrete

random variable, X:

n

var (X) =

ه

2

(xi - EX ) f (xi )

i=1

standard deviation is square root of variance

Copyright 1996 Lawrence C. Marsh

2.29

calculate the variance for a

discrete random variable, X:

2

xi

f(xi)

(xi - EX)

(xi - EX) f(xi)

2

3

4

5

6

.1

.3

.1

.2

.3

2 - 4.3 = -2.3

3 - 4.3 = -1.3

4 - 4.3 = - .3

5 - 4.3 = .7

6 - 4.3 = 1.7

5.29 (.1) =

1.69 (.3) =

.09 (.1) =

.49 (.2) =

2.89 (.3) =

.529

.507

.009

.098

.867

n

S xi f(xi) = .2 + .9 + .4 + 1.0 + 1.8 = 4.3

i=1

n

2

S (xi - EX) f(xi) = .529 + .507 + .009 + .098 + .867

= 2.01

i=1

Copyright 1996 Lawrence C. Marsh

2.30

Z = a + cX

var(Z) = var(a + cX)

2

= E [(a+cX) - E(a+cX)]

2

= c var(X)

2

var(a + cX) = c var(X)

Copyright 1996 Lawrence C. Marsh

Joint pdf

2.31

A joint probability density function,

f(x,y), provides the probabilities

associated with the joint occurrence

of all of the possible pairs of X and Y.

Copyright 1996 Lawrence C. Marsh

Survey of College City, NY

joint pdf

f(x,y)

vacation X = 0

homes

owned

X=1

college grads

in household

Y=2

Y=1

f(0,1)

.45

f(0,2)

.15

.05

f(1,1)

.35

f(1,2)

2.32

Copyright 1996 Lawrence C. Marsh

2.33

Calculating the expected value of

functions of two random variables.

E[g(X,Y)] = S S g(xi,yj) f(xi,yj)

i

j

E(XY) = S S xi yj f(xi,yj)

i

j

E(XY) = (0)(1)(.45)+(0)(2)(.15)+(1)(1)(.05)+(1)(2)(.35)=.75

Copyright 1996 Lawrence C. Marsh

2.34

Marginal pdf

The marginal probability density functions,

f(x) and f(y), for discrete random variables,

can be obtained by summing over the f(x,y)

with respect to the values of Y to obtain f(x)

with respect to the values of X to obtain f(y).

f(xi) = S f(xi,yj)

j

f(yj) = S f(xi,yj)

i

Copyright 1996 Lawrence C. Marsh

marginal

Y=1

Y=2

2.35

marginal

pdf for X:

X=0

.45

.15

.60 f(X = 0)

X=1

.05

.35

.40 f(X = 1)

.50

.50

f(Y = 2)

marginal

pdf for Y:

f(Y = 1)

Copyright 1996 Lawrence C. Marsh

Conditional pdf

2.36

The conditional probability density

functions of X given Y=y , f(x|y),

and of Y given X=x , f(y|x),

are obtained by dividing f(x,y) by f(y)

to get f(x|y) and by f(x) to get f(y|x).

f(x,y)

f(x|y) =

f(y)

f(x,y)

f(y|x) =

f(x)

Copyright 1996 Lawrence C. Marsh

2.37

conditonal

f(Y=1|X = 0)=.75

Y=1

.75

X=0

f(X=0|Y=1)=.90 .90

f(X=1|Y=1)=.10 .10

X=1

.45

Y=2

f(Y=2|X= 0)=.25

.25

.60

.15

.05 .35

.30

.70

f(X=0|Y=2)=.30

f(X=1|Y=2)=.70

.40

.125 .875

f(Y=1|X = 1)=.125

.50

.50 f(Y=2|X = 1)=.875

Copyright 1996 Lawrence C. Marsh

Independence

X and Y are independent random

variables if their joint pdf, f(x,y),

is the product of their respective

marginal pdfs, f(x) and f(y) .

f(xi,yj) = f(xi) f(yj)

for independence this must hold for all pairs of i and j

2.38

Copyright 1996 Lawrence C. Marsh

not independent

Y=1

Y=2

.50x.60=.30

.50x.60=.30

2.39

marginal

pdf for X:

X=0

.45

.15

.60 f(X = 0)

X=1

.05

.35

.40 f(X = 1)

.50x.40=.20

marginal

pdf for Y:

.50

f(Y = 1)

.50x.40=.20

.50

f(Y = 2)

The calculations

in the boxes show

the numbers

required to have

independence.

Copyright 1996 Lawrence C. Marsh

2.40

Covariance

The covariance between two random

variables, X and Y, measures the

linear association between them.

cov(X,Y) = E[(X - EX)(Y-EY)]

Note that variance is a special case of covariance.

2

cov(X,X) = var(X) = E[(X - EX) ]

Copyright 1996 Lawrence C. Marsh

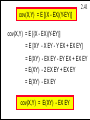

2.41

cov(X,Y) = E [(X - EX)(Y-EY)]

cov(X,Y) = E [(X - EX)(Y-EY)]

= E [XY - X EY - Y EX + EX EY]

= E(XY) - EX EY - EY EX + EX EY

= E(XY) - 2 EX EY + EX EY

= E(XY) - EX EY

cov(X,Y) = E(XY) - EX EY

Y=1

X=0

.45

Copyright 1996 Lawrence C. Marsh

2.42

Y=2

.15

.60

EX=0(.60)+1(.40)=.40

X=1

.05

.50

.35

.50

EY=1(.50)+2(.50)=1.50

EX EY = (.40)(1.50) = .60

.40

covariance

cov(X,Y) = E(XY) - EX EY

= .75 - (.40)(1.50)

= .75 - .60

= .15

E(XY) = (0)(1)(.45)+(0)(2)(.15)+(1)(1)(.05)+(1)(2)(.35)=.75

Copyright 1996 Lawrence C. Marsh

Correlation

2.43

The correlation between two random

variables X and Y is their covariance

divided by the square roots of their

respective variances.

r(X,Y) =

cov(X,Y)

var(X) var(Y)

Correlation is a pure number falling between -1 and 1.

Y=1

Copyright 1996 Lawrence C. Marsh

Y=2

2.44

EX=.40

2

2

2

EX=0(.60)+1(.40)=.40

X=0

.45

.05

X=1

.15

.35

.60

2

var(X) = E(X ) - (EX)

2

= .40 - (.40)

= .24

.40

cov(X,Y) = .15

.50

EY=1.50

2 2

2

.50

EY=1(.50)+2(.50)

2

2

var(Y) = E(Y ) - (EY)

= .50 + 2.0

= 2.50 - (1.50)2

= 2.50

= .25

correlation

r(X,Y) =

cov(X,Y)

var(X) var(Y)

r(X,Y) = .61

2

Copyright 1996 Lawrence C. Marsh

2.45

Zero Covariance & Correlation

Independent random variables

have zero covariance and,

therefore, zero correlation.

The converse is not true.

Copyright 1996 Lawrence C. Marsh

2.46

Since expectation is a linear operator,

it can be applied term by term.

The expected value of the weighted sum

of random variables is the sum of the

expectations of the individual terms.

E[c1X + c2Y] = c1EX + c2EY

In general, for random variables X1, . . . , Xn :

E[c1X1+...+ cnXn] = c1EX1+...+ cnEXn

Copyright 1996 Lawrence C. Marsh

2.47

The variance of a weighted sum of random

variables is the sum of the variances, each times

the square of the weight, plus twice the covariances

of all the random variables times the products of

their weights.

Weighted sum of random variables:

2

2

var(c1X + c2Y)=c1 var(X)+c2 var(Y) + 2c1c2cov(X,Y)

Weighted difference of random variables:

var(c1X - c2Y) = c21 var(X)+c22var(Y) - 2c1c2cov(X,Y)

Copyright 1996 Lawrence C. Marsh

The Normal Distribution

Y~

f(y) =

2.48

2

N(b,s )

(y - b)2

exp

2

1

2s

2 p s2

f(y)

b

y

Copyright 1996 Lawrence C. Marsh

The Standardized Normal

Z = (y - b)/s

Z ~ N(0,1)

f(z) =

1

2p

exp

- z2

2

2.49

Copyright 1996 Lawrence C. Marsh

Y~

2.50

N(b,s2)

f(y)

b

P[Y>a]

= P

Y-b

s

>

a

a-b

s

= P Z >

y

a-b

s

Copyright 1996 Lawrence C. Marsh

Y~

N(b,s2)

2.51

b

y

f(y)

a

P[a<Y<b] = P

=

P

a-b

s

a-b

s

b

<

Y-b

s

<Z<

<

b-b

b-b

s

s

Copyright 1996 Lawrence C. Marsh

2.52

Linear combinations of jointly

normally distributed random variables

are themselves normally distributed.

Y1 ~ N(b1,s12), Y2 ~ N(b2,s22), . . . , Yn ~ N(bn,sn2)

W = c1Y1 + c2Y2 + . . . + cnYn

W ~ N[ E(W), var(W) ]

Copyright 1996 Lawrence C. Marsh

Chi-Square

2.53

If Z1, Z2, . . . , Zm denote m independent

N(0,1) random variables, and

2

2

2

2

V = Z1 + Z2 + . . . + Zm, then V ~ c(m)

V is chi-square with m degrees of freedom.

mean:

E[V] = E[ c(m) ] = m

variance:

2

var[V] = var[ c(m) ] = 2m

2

Copyright 1996 Lawrence C. Marsh

2.54

Student - t

If Z ~ N(0,1) and V ~ c(m) and if Z and V

are independent then,

Z

2

t=

V

~ t(m)

m

t is student-t with m degrees of freedom.

mean:

E[t] = E[t(m) ] = 0 symmetric about zero

variance:

var[t] = var[t(m) ] = m / (m-2)

Copyright 1996 Lawrence C. Marsh

2.55

F Statistic

If V1 ~ c(m ) and V2 ~ c(m ) and if V1 and V2

1

2

are independent, then

V1

2

2

F=

m1

V2

~ F(m1,m2)

m2

F is an F statistic with m1 numerator

degrees of freedom and m2 denominator

degrees of freedom.

Copyright 1996 Lawrence C. Marsh

Chapter 3

3.1

The Simple Linear

Regression

Model

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

3.2

Purpose of Regression Analysis

1. Estimate a relationship among

economic

variables, such as y = f(x).

2. Forecast or predict the value of one

variable, y, based on the value of

another variable, x.

Copyright 1996 Lawrence C. Marsh

Weekly Food Expenditures

y = dollars spent each week on food items.

x = consumer’s weekly income.

The relationship between x and the expected

value of y , given x, might be linear:

E(y|x) = b1 + b2 x

3.3

Copyright 1996 Lawrence C. Marsh

f(y|x=480)

f(y|x=480)

my|x=480

y

Figure 3.1a Probability Distribution f(y|x=480)

of Food Expenditures if given income x=$480.

3.4

Copyright 1996 Lawrence C. Marsh

f(y|x)

f(y|x=480)

f(y|x=800)

my|x=480

my|x=800

Figure 3.1b Probability Distribution of Food

Expenditures if given income x=$480 and x=$800.

3.5

y

Copyright 1996 Lawrence C. Marsh

Average

Expenditure

E(y|x)

3.6

E(y|x)=b1+b2x

DE(y|x)

Dx

b 2=

DE(y|x)

Dx

b1{

x (income)

Figure 3.2 The Economic Model: a linear relationship

between avearage expenditure on food and income.

Copyright 1996 Lawrence C. Marsh

Homoskedastic Case

f(yt)

.

.

x1=480

x2=800

income

xt

Figure 3.3. The probability density function

for yt at two levels of household income, x t

3.7

Copyright 1996 Lawrence C. Marsh

Heteroskedastic Case

f(yt)

.

.

x1

x2

x3

.

income

Figure 3.3+. The variance of yt increases

as household income, x t , increases.

xt

3.8

Copyright 1996 Lawrence C. Marsh

Assumptions of the Simple Linear

Regression Model - I

1. The average value of y, given x, is given by

the linear regression:

E(y) = b1 + b2x

2. For each value of x, the values of y are

distributed around their mean with variance:

var(y) = s2

3. The values of y are uncorrelated, having zero

covariance and thus no linear relationship:

cov(yi ,yj) = 0

4. The variable x must take at least two different

values, so that x ° c, where c is a constant.

3.9

Copyright 1996 Lawrence C. Marsh

3.10

One more assumption that is often used in

practice but is not required for least squares:

5. (optional) The values of y are normally

distributed about their mean for each

value of x:

y ~ N [(b1+b2x), s2 ]

Copyright 1996 Lawrence C. Marsh

The Error Term

3.11

y is a random variable composed of two parts:

I. Systematic component:

This is the mean of y.

E(y) = b1 + b2x

II. Random component:

e = y - E(y)

= y - b 1 - b 2x

This is called the random error.

Together

E(y) and e form the model:

y = b1 + b2x + e

Copyright 1996 Lawrence C. Marsh

3.12

y

.

y4

e4 {

y3

y2

y1

e2 {.

E(y) = b1 + b2x

.} e3

e1

}

.

x1

x2

x3

x4

Figure 3.5 The relationship among y, e and

the true regression line.

x

Copyright 1996 Lawrence C. Marsh

3.13

y

y^3

y2

^e {.

2 .

y^1.

y4

.

^e {

4

.y^

^y = b + b x

1

2

x4

x

4

.} ^e3

.

y

3

y^2

^

} e1

.

y

1

x1

x2

x3

Figure 3.7a The relationship among y, e^ and

the fitted regression line.

Copyright 1996 Lawrence C. Marsh

3.14

y

. y4

y^*1.

{

y^*2

.

^e* { y

2 . 2

y^*3

.

^e* {

3

.

y

{.

^e*

4

y^*4

^y = b + b x

1

2

^y*= b* + b* x

1

2

3

^e*

1

.

y

1

x1

x2

x3

x4

Figure 3.7b The sum of squared residuals

from any other line will be larger.

x

f(.)

Copyright 1996 Lawrence C. Marsh

f(e)

f(y)

0

b1+b2x

3.15

Figure 3.4 Probability density function for e and y

Copyright 1996 Lawrence C. Marsh

The Error Term Assumptions

3.16

1. The value of y, for each value of x, is

y = b1 + b2x + e

2. The average value of the random error e is:

E(e) = 0

3. The variance of the random error e is:

var(e) = s2 = var(y)

4. The covariance between any pair of e’s is:

cov(ei ,ej) = cov(yi ,yj) = 0

5. x must take at least two different values so that

x ° c, where c is a constant.

6. e is normally distributed with mean 0, var(e)=s2

(optional)

e ~ N(0,s2)

Copyright 1996 Lawrence C. Marsh

Unobservable Nature

of the Error Term

3.17

1. Unspecified factors / explanatory variables,

not in the model, may be in the error term.

2. Approximation error is in the error term if

relationship between y and x is not

exactly

a perfectly linear relationship.

3. Strictly unpredictable random behavior that

may be unique to that observation is in error.

Copyright 1996 Lawrence C. Marsh

Population regression values:

y t = b1 + b2x t + e t

Population regression line:

E(y t|x t) = b1 + b2x t

Sample regression values:

y t = b1 + b2x t + ^e t

Sample regression line:

y^ t = b1 + b2x t

3.18

Copyright 1996 Lawrence C. Marsh

3.19

y t = b1 + b2x t + e t

e t = y t - b1 - b2x t

Minimize error sum of squared deviations:

S(b1,b2) =

T

S(y t

t=1

- b1 - b2x t )2

(3.3.4)

Copyright 1996 Lawrence C. Marsh

Minimize w.r.t. b1 and b2:

S(b1,b2) =

S(.)

b1

S(.)

b2

T

S(y t

t =1

- b1 - b2x t )2

= - 2 S (y t

= -2S

3.20

(3.3.4)

- b1 - b2x t )

x t (y t - b 1 - b 2 x t )

Set each of these two derivatives equal to zero and

solve these two equations for the two unknowns:

b1 b2

Copyright 1996 Lawrence C. Marsh

Minimize w.r.t. b1 and b2:

S(.) =

S(.)

T

S

t =1

(y t

3.21

- b1 - b2x t )2

S(.)

.

S(.) <

0

bi

S(.) =

0

bi

.

bi

.S(.)

bi

>0

bi

Copyright 1996 Lawrence C. Marsh

To minimize S(.), you set the two

derivatives equal to zero to get:

S(.)

b1

S(.)

b2

= - 2 S (y t

= -2S

3.22

- b1 - b2x t ) = 0

x t (y t - b1 - b2x t ) = 0

When these two terms are set to zero,

b1 and b2 become b1 and b2 because they no longer

represent just any value of b1 and b2 but the special

values that correspond to the minimum of S(.) .

Copyright 1996 Lawrence C. Marsh

- 2 S (y t

-2S

- b1 - b2x t ) = 0

x t (y t - b1 - b2x t ) = 0

S y t - Tb1 - b2 S x t

= 0

S x t y t - b1 S x t - b2 S xt

2

= 0

Tb1 + b2 S x t = S y t

2

b1 S x t + b2 S xt = S x t y t

3.23

Copyright 1996 Lawrence C. Marsh

Tb1 + b2 S x t = S y t

2

b1 S x t + b2 S xt = S x t y t

Solve for b1 and b2 using definitions of

b2 =

x and y

T S x t yt - S x t S y t

T S x t - (S x t )

2

b1 = y - b2 x

2

3.24

Copyright 1996 Lawrence C. Marsh

elasticities

Dy x

Dy/y

percentage change in y

h =

=

=

Dx y

percentage change in x

Dx/x

Using calculus, we can get the elasticity at a point:

h = lim

Dx 0

Dy x

y x

=

Dx y

x y

3.25

Copyright 1996 Lawrence C. Marsh

applying elasticities

E(y) = b1 + b2 x

E(y)

x

=

b2

E(y) x

x

= b2

h =

x E(y)

E(y)

3.26

Copyright 1996 Lawrence C. Marsh

estimating elasticities

y x

h =

x y

^

^

y

t

3.27

x

= b2

y

= b1 + b2 x t = 4 + 1.5 x t

x = 8 = average number of years of experience

y = $10 = average wage rate

x

h = b2

y

^

8

= 1.5

= 1.2

10

Copyright 1996 Lawrence C. Marsh

Prediction

3.28

Estimated regression equation:

^

y

t

= 4 + 1.5 x t

x t = years of experience

^

yt = predicted wage rate

^

If x t = 2 years, then yt = $7.00 per hour.

^

If x t = 3 years, then yt = $8.50 per hour.

Copyright 1996 Lawrence C. Marsh

log-log models

ln(y) = b1 + b2 ln(x)

ln(y)

=

x

1 y

y x

=

b2

ln(x)

x

b2

1 x

x x

3.29

1 y

y x

Copyright 1996 Lawrence C. Marsh

x y

y x

= b2

=

3.30

1 x

x x

b2

elasticity of y with respect to x:

h =

x y

y x

=

b2

Copyright 1996 Lawrence C. Marsh

Chapter 4

4.1

Properties of

Least Squares

Estimators

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

Simple Linear Regression Model

4.2

y t = b1 + b2 x t + e t

yt = household weekly food expenditures

x t = household weekly income

For a given level of x t, the expected

level of food expenditures will be:

E(yt|x t) =

b1 + b 2 x t

Copyright 1996 Lawrence C. Marsh

Assumptions of the Simple

Linear Regression Model

4.3

1. yt = b1 + b2x t + e t

2. E(e t) = 0 <=> E(yt) = b1 + b2x t

3. var(e t) =

s 2 = var(yt)

4. cov(e i,e j) = cov(yi,yj) = 0

5.

x t ° c for every observation

6.

e t~N(0,s 2) <=> yt~N(b1+ b2x t,s 2)

Copyright 1996 Lawrence C. Marsh

The population parameters b1 and b2

are unknown population constants.

The formulas that produce the

sample estimates b1 and b2 are

called the estimators of b1 and

b2.

When b0 and b1 are used to represent

the formulas rather than specific values,

they are called estimators of b1 and b2

which are random variables because

they are different from sample to sample.

4.4

Copyright 1996 Lawrence C. Marsh

4.5

Estimators are Random Variables

( estimates are not )

• If the least squares estimators b0 and b1

are random variables, then what are their

their means, variances, covariances and

probability distributions?

• Compare the properties of alternative

estimators to the properties of the

least squares estimators.

Copyright 1996 Lawrence C. Marsh

4.6

The Expected Values of b1 and b2

The least squares formulas (estimators)

in the simple regression case:

b2 =

TSxtyt - Sxt Syt

TSxt -(Sxt)

2

b1 = y - b2x

where

2

(3.3.8a)

(3.3.8b)

y = Syt / T and x = Sx t / T

Substitute in

to get:

yt = b1 + b2x t + e t

Copyright 1996 Lawrence C. Marsh

TSxtet - Sxt Set

b2 = b2 +

2

2

TSxt -(Sxt)

The mean of b2 is:

TSxtEet - Sxt SEet

Eb2 = b2 +

2

2

TSxt -(Sxt)

Since

Eet = 0, then Eb2 = b2 .

4.7

Copyright 1996 Lawrence C. Marsh

An Unbiased Estimator

The result Eb2 = b2 means that

the distribution of b2 is centered at b2.

Since the distribution of b2

is centered at b2 ,we say that

b2 is an unbiased estimator of b2.

4.8

Copyright 1996 Lawrence C. Marsh

Wrong Model Specification

The unbiasedness result on the

previous slide assumes that we

are using the correct model.

If the model is of the wrong form

or is missing important variables,

then Eet ° 0, then Eb2 ° b2 .

4.9

Copyright 1996 Lawrence C. Marsh

4.10

Unbiased Estimator of the Intercept

In a similar manner, the estimator b1

of the intercept or constant term can be

shown to be an unbiased estimator of b1

when the model is correctly specified.

Eb1 = b1

Copyright 1996 Lawrence C. Marsh

4.11

Equivalent expressions for b2:

S(xt - x )(yt - y )

b2 =

2

S(xt - x )

(4.2.6)

Expand and multiply top and bottom by T:

b2 =

TSxtyt - Sxt Syt

TSxt -(Sxt)

2

2

(3.3.8a)

Copyright 1996 Lawrence C. Marsh

4.12

Variance of b2

Given that both yt and et have variance s 2,

the variance of the estimator b2 is:

var(b2) =

s2

S(x t - x)

2

b2 is a function of the yt values but

var(b2) does not involve yt directly.

Copyright 1996 Lawrence C. Marsh

4.13

Variance of b1

Given

b1 = y - b2x

the variance of the estimator b1 is:

Sx t

var(b1) = s 2

2

T S(x t - x)

2

Copyright 1996 Lawrence C. Marsh

Covariance of b1 and b2

cov(b1,b2) = s2

4.14

-x

S(x t - x)

2

If x = 0, slope can change without affecting

the variance.

Copyright 1996 Lawrence C. Marsh

What factors determine

variance and covariance ?

4.15

1. s 2: uncertainty about yt values uncertainty about

b1, b2 and their relationship.

2. The more spread out the xt values are then the more

confidence we have in b1, b2, etc.

3. The larger the sample size, T, the smaller the

variances and covariances.

4. The variance b1 is large when the (squared) xt values

are far from zero (in either direction).

5. Changing the slope, b2, has no effect on the intercept,

b1, when the sample mean is zero. But if sample

mean is positive, the covariance between b1 and

b2 will be negative, and vice versa.

Copyright 1996 Lawrence C. Marsh

Gauss-Markov Theorm

4.16

Under the first five assumptions of the

simple, linear regression model, the

ordinary least squares estimators b1

and b2 have the smallest variance of

all linear and unbiased estimators of

b1 and b2. This means that b1and b2

are the Best Linear Unbiased Estimators

(BLUE) of b1 and b2.

Copyright 1996 Lawrence C. Marsh

4.17

implications of Gauss-Markov

1. b1 and b2 are “best” within the

class

of linear and

unbiased estimators.

2. “Best” means smallest variance

within the class of linear/unbiased.

3. All of the first five assumptions must

hold to satisfy Gauss-Markov.

4. Gauss-Markov does not require

assumption six: normality.

5. G-Markov is not based on the

Copyright 1996 Lawrence C. Marsh

4.18

G-Markov implications (continued)

6. If we are not satisfied with restricting

our estimation to the class of linear and

unbiased estimators, we should ignore

the Gauss-Markov Theorem and use

some nonlinear and/or biased estimator

instead. (Note: a biased or nonlinear

estimator could have smaller variance

than those satisfying Gauss-Markov.)

7. Gauss-Markov applies to the b1 and b2

estimators and not to particular sample

values (estimates) of b1 and b2.

Copyright 1996 Lawrence C. Marsh

Probability Distribution

of Least Squares Estimators

b1 ~ N b 1 ,

s2

Sx t

2

T S(x t - x) 2

b2 ~ N b 2 ,

s2

S(x t - x)

2

4.19

Copyright 1996 Lawrence C. Marsh

yt and e t normally distributed

4.20

The least squares estimator of b2 can be

expressed as a linear combination of yt’s:

b2 = S wt yt

(x t - x)

where wt =

2

S(x t - x)

b1 = y - b2x

This means that b1and b2 are normal since

linear combinations of normals are normal.

Copyright 1996 Lawrence C. Marsh

normally distributed under

The Central Limit Theorem

4.21

If the first five Gauss-Markov assumptions

hold, and sample size, T, is sufficiently large,

then the least squares estimators, b1 and b2,

have a distribution that approximates the

normal distribution with greater accuracy

the larger the value of sample size, T.

Copyright 1996 Lawrence C. Marsh

Consistency

4.22

We would like our estimators, b1 and b2, to collapse

onto the true population values, b1 and b2, as

sample size, T, goes to infinity.

One way to achieve this consistency property is

for the variances of b1 and b2 to go to zero as T

goes to infinity.

Since the formulas for the variances of the least

squares estimators b1 and b2 show that their

variances do, in fact, go to zero, then b1 and b2,

are consistent estimators of b1 and b2.

Copyright 1996 Lawrence C. Marsh

Estimating the variance

of the error term, s 2

^e

t

= yt - b1 - b2 x t

T

^2

s =

Set

^2

t =1

T- 2

2

^

s is an unbiased estimator of s 2

4.23

Copyright 1996 Lawrence C. Marsh

4.24

The Least Squares

Predictor, y^o

Given a value of the explanatory

variable, Xo, we would like to predict

a value of the dependent variable, yo.

The least squares predictor is:

^y = b + b x

o

1

2 o

(4.7.2)

Copyright 1996 Lawrence C. Marsh

Chapter 5

5.1

Inference

in the Simple

Regression Model

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

Assumptions of the Simple

Linear Regression Model

1. yt = b1 + b2x t + e t

2. E(e t) = 0 <=> E(yt) = b1 + b2x t

3. var(e t) =

s 2 = var(yt)

4. cov(e i,e j) = cov(yi,yj) = 0

5. x t ° c for every observation

6.

e t~N(0,s 2) <=> yt~N(b1+ b2x t,s 2)

5.2

Copyright 1996 Lawrence C. Marsh

Probability Distribution

of Least Squares Estimators

b1 ~ N b 1 ,

s2

Sx t

2

T S(x t - x) 2

b2 ~ N b 2 ,

s2

S(x t - x)

2

5.3

Copyright 1996 Lawrence C. Marsh

Error Variance Estimation

5.4

Unbiased estimator of the error variance:

^2 =

s

S

2

^

e

t

T-2

Transform to a chi-square distribution:

^2

(T - 2) s

s

2

~

c

T-2

Copyright 1996 Lawrence C. Marsh

We make a correct decision if:

5.5

• The null hypothesis is false and we decide to reject it.

• The null hypothesis is true and we decide not to reject it.

Our decision is incorrect if:

• The null hypothesis is true and we decide to reject it.

This is a type I error.

• The null hypothesis is false and we decide not to reject it.

This is a type II error.

Copyright 1996 Lawrence C. Marsh

b2 ~ N b 2 ,

s2

S(x t - x)

2

Create a standardized normal random variable, Z,

by subtracting the mean of b2 and dividing by its

standard deviation:

Z =

b2 - b2

var(b2)

~ N(0,1)

5.6

Copyright 1996 Lawrence C. Marsh

Simple Linear Regression

yt = b1 + b2x t + e t

where E e t = 0

yt ~ N(b1+ b2x t , s 2)

since Eyt = b1 + b2x t

e t = yt - b1 - b2x t

Therefore,

e t ~ N(0,s 2) .

5.7

Copyright 1996 Lawrence C. Marsh

5.8

Create a Chi-Square

e t ~ N(0,s 2) but want N(0,1) .

(e t /s) ~ N(0,1) Standard Normal .

(e t

2

/s)

~ c2(1)

Chi-Square .

Copyright 1996 Lawrence C. Marsh

5.9

Sum of Chi-Squares

St =1(e t /s)2 =

(e1 /s)2 + (e 2 /s)2 +. . .+ (e T /s)2

c2(1) + c2(1) +. . .+c2(1)

Therefore,

=

c2(T)

St =1(e t /s)2 ~ c2(T)

Copyright 1996 Lawrence C. Marsh

Chi-Square degrees of freedom

5.10

Since the errors e t = yt - b1 - b2x t

are not observable, we estimate them with

the sample residuals e t = yt - b1 - b2x t.

Unlike the errors, the sample residuals are

not independent since they use up two degrees

of freedom by using b1 and b2 to estimate b1 and b2.

We get only T-2 degrees of freedom instead of T.

Copyright 1996 Lawrence C. Marsh

5.11

Student-t Distribution

t=

Z

~ t(m)

V/m

where Z ~ N(0,1)

and V ~

c

2

(m)

Copyright 1996 Lawrence C. Marsh

t =

Z

5.12

~ t(m)

V / (T- 2)

where Z =

(b2 - b2)

var(b2)

and var(b2) =

s2

S( xi - x )2

Copyright 1996 Lawrence C. Marsh

5.13

Z

t =

V / (T-2)

V =

(b2 - b2)

t =

var(b2)

2

^

(T-2) s

(T2)

s2

(T-2)

2

s

^2

s

s

Copyright 1996 Lawrence C. Marsh

2

5.14

var(b2) =

S( xi - x )2

(b2 - b2)

s2

notice the

cancellations

S( xi - x )2

t =

=

^

(T-2) s 2

(T2)

s2

(b2 - b2)

^2

s

S( xi - x )2

Copyright 1996 Lawrence C. Marsh

5.15

t =

(b2 - b2)

=

^2

s

S( xi - x )2

t =

(b2 - b2)

se(b2)

(b2 - b2)

^

var(b2)

Copyright 1996 Lawrence C. Marsh

5.16

Student’s

t =

t - statistic

(b2 - b2)

se(b2)

~ t (T-2)

t has a Student-t Distribution

with T- 2 degrees of freedom.

Copyright 1996 Lawrence C. Marsh

5.17

Figure 5.1 Student-t Distribution

f(t)

(1-a)

a/2

-tc

0

a/2

tc

t

red area = rejection region for 2-sided test

Copyright 1996 Lawrence C. Marsh

5.18

probability statements

P( t < -tc ) = P( t > tc ) = a/2

P(-tc ٹt ٹtc) = 1 - a

P(-tc ٹ

(b2 - b2)

se(b2)

ٹtc) = 1 - a

Copyright 1996 Lawrence C. Marsh

5.19

Confidence Intervals

Two-sided (1-a)x100% C.I. for b1:

b1 - ta/2[se(b1)], b1 + ta/2[se(b1)]

Two-sided (1-a)x100% C.I. for b2:

b2 - ta/2[se(b2)], b2 + ta/2[se(b2)]

Copyright 1996 Lawrence C. Marsh

5.20

Student-t vs. Normal Distribution

1. Both are symmetric bell-shaped distributions.

2. Student-t distribution has fatter tails than the normal.

3. Student-t converges to the normal for infinite sample.

4. Student-t conditional on degrees of freedom (df).

5. Normal is a good approximation of Student-t for the first few

decimal places when df > 30 or so.

Copyright 1996 Lawrence C. Marsh

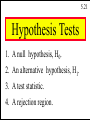

5.21

Hypothesis Tests

1. A null hypothesis, H0.

2. An alternative hypothesis, H1.

3. A test statistic.

4. A rejection region.

Copyright 1996 Lawrence C. Marsh

Rejection Rules

5.22

1. Two-Sided Test:

If the value of the test statistic falls in the critical region in either

tail of the t-distribution, then we reject the null hypothesis in favor

of the alternative.

2. Left-Tail Test:

If the value of the test statistic falls in the critical region which lies

in the left tail of the t-distribution, then we reject the null

hypothesis in favor of the alternative.

2. Right-Tail Test:

If the value of the test statistic falls in the critical region which lies

in the right tail of the t-distribution, then we reject the null

hypothesis in favor of the alternative.

Copyright 1996 Lawrence C. Marsh

5.23

Format for Hypothesis Testing

1. Determine null and alternative hypotheses.

2. Specify the test statistic and its distribution

as if the null hypothesis were true.

3. Select a and determine the rejection region.

4. Calculate the sample value of test statistic.

5. State your conclusion.

Copyright 1996 Lawrence C. Marsh

practical vs. statistical

significance in economics

5.24

Practically but not statistically significant:

When sample size is very small, a large average gap between

the salaries of men and women might not be statistically

significant.

Statistically but not practically significant:

When sample size is very large, a small correlation (say, r =

0.00000001) between the winning numbers in the PowerBall

Lottery and the Dow-Jones Stock Market Index might be

statistically significant.

Copyright 1996 Lawrence C. Marsh

Type I and Type II errors

5.25

Type I error:

We make the mistake of rejecting the null

hypothesis when it is true.

a = P(rejecting H0 when it is true).

Type II error:

We make the mistake of failing to reject the null

hypothesis when it is false.

b = P(failing to reject H0 when it is false).

Copyright 1996 Lawrence C. Marsh

5.26

Prediction Intervals

A (1-a)x100% prediction interval for yo is:

^

yo ± tc se( f )

f = y^ o - yo

se( f ) =

^

var( f )

2

(

x

x

)

1

o

^

^

2

var( f ) = s 1 +

+

T

S(x t - x)2

Copyright 1996 Lawrence C. Marsh

Chapter 6

6.1

The Simple Linear

Regression Model

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

Explaining Variation in yt

6.2

Predicting yt without any explanatory variables:

yt = b1 + et

T

S(yt - b1) = 0

t=1

T

S

T

S

2

et = (yt

t=1

t=1

T

- b1)

2

T

S

b1

2

e

t=1 t

T

= -2 tS

(y

b

)

=

0

t

1

=1

Syt - Tb1 = 0

t=1

b1 = y

Why not y?

Copyright 1996 Lawrence C. Marsh

Explaining Variation in yt

6.3

^

yt = b1 + b2xt + et

^

Explained variation: yt = b1 + b2xt

Unexplained variation:

^e = y - ^y = y - b - b x

t

t

t

t

1

2 t

Copyright 1996 Lawrence C. Marsh

Explaining Variation in yt

^

^

yt = yt + et

6.4

using y as baseline

^

^

yt - y = yt - y + et Why not y?

T

T

cross

^2 product

t=1 t

term

drops

out

T

2

^

S(yt-y) = S(yt-y) +Se

t=1

2

t=1

SST = SSR + SSE

Copyright 1996 Lawrence C. Marsh

Total Variation in yt

SST = total sum of squares

SST measures variation of yt around y

T

SST

= S(yt - y)

t=1

2

6.5

Copyright 1996 Lawrence C. Marsh

Explained Variation in yt

SSR = regression sum of squares

^

yt = b1 + b2xt

^

Fitted yt values:

^

SSR measures variation of yt around y

T

SSR

= S(yt - y)

t=1

^

2

6.6

Copyright 1996 Lawrence C. Marsh

Unexplained Variation in yt

SSE = error sum of squares

^

^

et = yt-yt = yt - b1 - b2xt

^

SSE measures variation of yt around yt

T

SSE

T

= S(yt - yt) = S

t=1

^ 2

t=1

^e 2

t

6.7

Copyright 1996 Lawrence C. Marsh

Analysis of Variance Table

Table 6.1 Analysis of Variance Table

Source of

Sum of

Mean

Variation

DF

Squares

Square

Explained

1

SSR

SSR/1

Unexplained T-2

SSE SSE/(T-2)

^ 2]

[= s

Total

T-1

SST

6.8

Copyright 1996 Lawrence C. Marsh

Coefficient of Determination

What proportion of the variation

in yt is explained?

0 ٹR 1ٹ

2

2

R =

SSR

SST

6.9

Copyright 1996 Lawrence C. Marsh

Coefficient of Determination

SST = SSR + SSE

SST

SST

Dividing

by SST

=

SSR SSE

+

SST SST

1 =

2

R =

SSR

SST

SSR + SSE

SST SST

= 1-

SSE

SST

6.10

Copyright 1996 Lawrence C. Marsh

Coefficient of Determination

6.11

R2 is only a descriptive measure.

2

R

does not measure the quality

of the regression model.

Focusing solely on maximizing

R2 is not a good idea.

Copyright 1996 Lawrence C. Marsh

Correlation Analysis

Population:

r=

Sample:

r=

6.12

cov(X,Y)

var(X) var(Y)

^

cov(X,Y)

^

var(X)

^

var(Y)

Copyright 1996 Lawrence C. Marsh

Correlation Analysis

T

6.13

^ =S

var(X)

(x

x)

(

T-1)

/

t

t=1

2

T

2

^

var(Y) = S(yt - y) /(T-1)

t=1

T

^

cov(X,Y)

= S(xt - x)(yt - y)/(T-1)

t=1

Copyright 1996 Lawrence C. Marsh

6.14

Correlation Analysis

Sample Correlation Coefficient

S(xt - x)(yt - y)

T

r=

t=1

T

S(xt - x) S(yt - y)

T

t=1

2

t=1

2

Copyright 1996 Lawrence C. Marsh

Correlation Analysis and R

2

6.15

For simple linear regression analysis:

2

r = R

2

2

R is also the correlation

^

between yt and yt

measuring “goodness of fit”.

Copyright 1996 Lawrence C. Marsh

Regression Computer Output

6.16

Typical computer output of regression estimates:

Table 6.2 Computer Generated Least Squares Results

(1)

(2)

(3)

(4)

(5)

Parameter Standard T for H0:

Variable

Estimate

Error Parameter=0 Prob>|T|

INTERCEPT 40.7676 22.1387

1.841

0.0734

X

0.1283

0.0305

4.201

0.0002

Copyright 1996 Lawrence C. Marsh

Regression Computer Output

b1 = 40.7676

b2 = 0.1283

se(b1) =

^ 1) = 490.12

var(b

se(b2) =

^ 2) = 0.0009326 = 0.0305

var(b

t =

t =

= 22.1287

=

40.7676

22.1287

= 1.84

b2

=

se(b2)

0.1283

0.0305

= 4.20

b1

se(b1)

6.17

Copyright 1996 Lawrence C. Marsh

Regression Computer Output

6.18

Sources of variation in the dependent variable:

Table 6.3 Analysis of Variance Table

Sum of

Mean

Source

DF

Squares

Square

Explained

1 25221.2229 25221.2229

Unexplained 38 54311.3314 1429.2455

Total

39 79532.5544

R-square: 0.3171

Copyright 1996 Lawrence C. Marsh

Regression Computer Output

SST = S(yt-y) = 79532

2

^

SSR = S(yt-y) = 25221

2

^

SSE = e = 54311

2

S

t

SSE /(T-2) = s^2

2

R =

SSR

SST

= 1429.2455

= 1-

SSE

SST

= 0.317

6.19

Copyright 1996 Lawrence C. Marsh

Reporting Regression Results

6.20

yt = 40.7676 + 0.1283xt

(s.e.) (22.1387) (0.0305)

yt = 40.7676 + 0.1283xt

(t) (1.84) (4.20)

Copyright 1996 Lawrence C. Marsh

Reporting Regression Results

6.21

2

R = 0.317

2

This R value may seem low but it is

typical in studies involving cross-sectional

data analyzed at the individual or micro level.

2

A considerably higher R value would be

expected in studies involving time-series data

analyzed at an aggregate or macro level.

Copyright 1996 Lawrence C. Marsh

Effects of Scaling the Data

6.22

Changing the scale of x

The estimated

coefficient and

standard error

change but the

other statistics

are unchanged.

yt = b1 + b2xt + et

yt = b1 + (cb2)(xt/c) + et

yt = b1 + b*2x*t + et

where

*

b =

2

cb2 and x*t = xt/c

Copyright 1996 Lawrence C. Marsh

Effects of Scaling the Data

6.23

Changing the scale of y

yt = b1 + b2xt + et

yt/c = (b1/c) + (b2/c)xt + et/c

All statistics

are changed

except for

the t-statistics

2

and R value.

*

*

*

y =b +b x

t

1

2

*

+

e

t

t

where y*t = yt/c

b* = b /c and

1

1

e*t = et/c

b*2 = b2/c

Copyright 1996 Lawrence C. Marsh

Effects of Scaling the Data

6.24

Changing the scale of x and y

yt = b1 + b2xt + et

No change in

the R2 or the

t-statistics or

in regression

results for b2

but all other

stats change.

yt/c = (b1/c) + (cb2/c)xt/c + et/c

*

*

y =b +

t

1

b2x*t + e*t

where y*t = yt/c

b* = b /c and

1

1

e*t = et/c

x*t = xt/c

Copyright 1996 Lawrence C. Marsh

Functional Forms

6.25

The term linear in a simple

regression model does not mean

a linear relationship between

variables, but a model in which

the parameters enter the model

in a linear way.

Copyright 1996 Lawrence C. Marsh

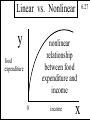

Linear vs. Nonlinear

6.27

Linear Statistical Models:

yt = b1 + b2xt + et

yt = b1 + b2 ln(xt) + et

ln(yt) = b1 + b2xt + et

yt = b1 +

2

b2xt +

et

Nonlinear Statistical Models:

yt = b1 +

b3

b2xt +

et

b3

yt

yt = b1 + b2xt + exp(b3xt) + et

= b1 + b2xt + et

Copyright 1996 Lawrence C. Marsh

6.27

Linear vs. Nonlinear

y

nonlinear

relationship

between food

expenditure and

income

food

expenditure

0

income

x

Copyright 1996 Lawrence C. Marsh

Useful Functional Forms

Look at

each form

and its

slope and

elasticity

1.

2.

3.

4.

5.

6.

Linear

Reciprocal

Log-Log

Log-Linear

Linear-Log

Log-Inverse

6.28

Copyright 1996 Lawrence C. Marsh

Useful Functional Forms

6.29

Linear

yt = b1 + b2xt + et

slope: b2

xt

elasticity: b2 y

t

Copyright 1996 Lawrence C. Marsh

6.30

Useful Functional Forms

Reciprocal

yt = b1 + b2 xt + et

1

slope:

1

- b2 2

xt

elasticity:

1

- b2 x y

t

t

Copyright 1996 Lawrence C. Marsh

Useful Functional Forms

Log-Log

ln(yt)= b1 + b2ln(xt) + et

yt

slope: b2 x

t

elasticity: b2

6.31

Copyright 1996 Lawrence C. Marsh

Useful Functional Forms

Log-Linear

ln(yt)= b1 + b2xt + et

slope: b2 yt

elasticity: b2xt

6.32

Copyright 1996 Lawrence C. Marsh

6.33

Useful Functional Forms

Linear-Log

yt= b1 + b2ln(xt) + et

slope:

1

_

b2

xt

elasticity:

1

_

b2

yt

Copyright 1996 Lawrence C. Marsh

Useful Functional Forms

Log-Inverse

ln(yt) = b1 - b2 x + et

1

t

yt

slope: b2 2

xt

1

elasticity: b2 x

t

6.34

Copyright 1996 Lawrence C. Marsh

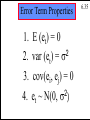

Error Term Properties

1.

2.

3.

4.

E (et) = 0

2

var (et) = s

cov(ei, ej) = 0

2

et ~ N(0, s )

6.35

Copyright 1996 Lawrence C. Marsh

Economic Models

1.

2.

3.

4.

5.

Demand Models

Supply Models

Production Functions

Cost Functions

Phillips Curve

6.36

Copyright 1996 Lawrence C. Marsh

Economic Models

6.37

1. Demand Models

* quality demanded (yd) and price (x)

* constant elasticity

ln(yt )= b1 + b2ln(x)t + et

d

Copyright 1996 Lawrence C. Marsh

Economic Models

6.38

2. Supply Models

* quality supplied (ys) and price (x)

* constant elasticity

ln(yt )= b1 + b2ln(xt) + et

s

Copyright 1996 Lawrence C. Marsh

Economic Models

6.39

3. Production Functions

* output (y) and input (x)

* constant elasticity

Cobb-Douglas Production Function:

ln(yt)= b1 + b2ln(xt) + et

Copyright 1996 Lawrence C. Marsh

Economic Models

4a. Cost Functions

* total cost (y) and output (x)

yt = b1 + b2

2

x

+

e

t

t

6.40

Copyright 1996 Lawrence C. Marsh

Economic Models

6.41

4b. Cost Functions

* average cost (x/y) and output (x)

(yt/xt) = b1/xt + b2xt + et/xt

Copyright 1996 Lawrence C. Marsh

Economic Models

6.42

5. Phillips Curve

nonlinear in both variables and parameters

* wage rate (wt) and time (t)

wt - wt-1

1

% Dwt = w

= ga + gh u

t-1

t

unemployment rate, ut

Copyright 1996 Lawrence C. Marsh

Chapter 7

7.1

The Multiple

Regression Model

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

Two Explanatory Variables

yt = b1 + b2xt2 + b3xt3 + et

xt‘s affect yt

separately

yt

= b2

xt2

yt

= b3

xt3

But least squares estimation of b2

now depends upon both xt2 and xt3 .

7.2

Copyright 1996 Lawrence C. Marsh

Correlated Variables

yt = b1 + b2xt2 + b3xt3 + et

yt = output

xt2 = capital

xt3 = labor

Always 5 workers per machine.

If number of workers per machine

is never varied, it becomes impossible

to tell if the machines or the workers

are responsible for changes in output.

7.3

Copyright 1996 Lawrence C. Marsh

The General Model

7.4

yt = b1 + b2xt2 + b3xt3 +. . .+ bKxtK + et

The parameter b1 is the intercept (constant) term.

The “variable” attached to b1 is xt1= 1.

Usually, the number of explanatory variables

is said to be K-1 (ignoring xt1= 1), while the

number of parameters is K. (Namely: b1 . . . bK).

Copyright 1996 Lawrence C. Marsh

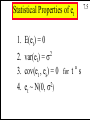

Statistical Properties of et

1. E(et) = 0

2

s

2. var(et) =

3. cov(et , es) = 0 for t ° s

4. et ~ N(0,

2

s)

7.5

Copyright 1996 Lawrence C. Marsh

Statistical Properties of yt

7.6

1. E (yt) = b1 + b2xt2 +. . .+ bKxtK

2. var(yt) = var(et) = s2

3. cov(yt ,ys) = cov(et , es) = 0 t°s

4. yt ~ N(b1+b2xt2 +. . .+bKxtK, s2)

Copyright 1996 Lawrence C. Marsh

Assumptions

7.7

1. yt = b1 + b2xt2 +. . .+ bKxtK + et

2. E (yt) = b1 + b2xt2 +. . .+ bKxtK

2

s

3. var(yt) = var(et) =

4. cov(yt ,ys) = cov(et ,es) = 0

t°s

5. The values of xtk are not random

6. yt ~ N(b1+b2xt2 +. . .+bKxtK, s2)

Copyright 1996 Lawrence C. Marsh

Least Squares Estimation

7.8

yt = b1 + b2xt2 + b3xt3 + et

T

S ؛S(b1, b2, b3) = tS= 1(yt - b1 - b2xt2 - b3xt3)

Define:

y*t = yt - y

x*t2 = xt2 - x2

x*t3 = xt3 - x3

2

Copyright 1996 Lawrence C. Marsh

Least Squares Estimators

b1 = y - b1 - b2x2 - b3x3

b2 =

b3 =

(S

2

*

t2)(Sxt3

y*x*

t

(S

(S

2

*

x

t2

)

- (Sy*t x*t3)(Sx*t2x*t3)

2

*

)(Sx )

t3

2

*

-

2

*

*

(Sx x )

t2 t3

)(Sxt2 ) - (S t t2)(S t3 t2)

2

2

2

*

*

*

*

(Sxt2 )(Sxt3 ) - (Sxt2xt3)

*

y x*

t t3

*

*

yx

*

*

x x

7.9

Copyright 1996 Lawrence C. Marsh

Dangers of Extrapolation

7.10

Statistical models generally are good only

“within the relevant range”. This means

that extending them to extreme data values

outside the range of the original data often

leads to poor and sometimes ridiculous results.

If height is normally distributed and the

normal ranges from minus infinity to plus

infinity, pity the man minus three feet tall.

Copyright 1996 Lawrence C. Marsh

Error Variance Estimation

7.11

Unbiased estimator of the error variance:

^2 =

s

S

2

^

e

t

T-K

Transform to a chi-square distribution:

^2

(T - K) s

s

2

~

c

T-K

Copyright 1996 Lawrence C. Marsh

Gauss-Markov Theorem

7.12

Under the assumptions of the

multiple regression model, the

ordinary least squares estimators

have the smallest variance of

all linear and unbiased estimators.

This means that the least squares

estimators are the Best Linear

Unbiased Estimators (BLUE).

Copyright 1996 Lawrence C. Marsh

7.13

Variances

yt = b1 + b2xt2 + b3xt3 + et

var(b2) =

var(b3) =

s

2

(1- r23)

2

S(xt2 - x2)

s

2

(1- r23)

2

2

S(xt3 - x3)

where r23 =

When r23 = 0

these reduce

to the simple

regression

formulas.

2

S(xt2 - x2)(xt3 - x3)

S(xt2 - x2) S(xt3 - x3)

2

2

Copyright 1996 Lawrence C. Marsh

7.14

Variance Decomposition

The variance of an estimator is smaller when:

1. The error variance, s , is smaller: s

2

2. The sample size, T, is larger:

T

2

(xt2 - x2)

S

t=1

0.

2

.

3. The variable’s values are more spread out:

(xt2 - x2) .

2

4. The correlation is close to zero: r23

0.

2

Copyright 1996 Lawrence C. Marsh

7.15

Covariances

yt = b1 + b2xt2 + b3xt3 + et

cov(b2,b3) =

- r23 s

2

(1- r23)

where r23 =

2

S(xt2 - x2) S(xt3 - x3)

2

2

S(xt2 - x2)(xt3 - x3)

S(xt2 - x2) S(xt3 - x3)

2

2

Copyright 1996 Lawrence C. Marsh

Covariance Decomposition

7.16

The covariance between any two estimators

is larger in absolute value when:

1. The error variance, s , is larger.

2

2. The sample size, T, is smaller.

3. The values of the variables are less spread out.

4. The correlation, r23, is high.

Copyright 1996 Lawrence C. Marsh

Var-Cov Matrix

7.17

yt = b1 + b2xt2 + b3xt3 + et

The least squares estimators b1, b2, and b3

have covariance matrix:

var(b1) cov(b1,b2) cov(b1,b3)

cov(b1,b2,b3) = cov(b1,b2) var(b2) cov(b2,b3)

cov(b1,b3) cov(b2,b3) var(b3)

Copyright 1996 Lawrence C. Marsh

7.18

Normal

yt = b1 + b2x2t + b3x3t +. . .+ bKxKt + et

yt ~N (b1 + b2x2t + b3x3t +. . .+ bKxKt), s 2

This implies and is implied by: et ~ N(0, s )

2

Since bk is a linear

function of the yt’s:

bk ~ N bk, var(bk)

bk - bk

z =

~ N(0,1)

var(bk)

for k = 1,2,...,K

Copyright 1996 Lawrence C. Marsh

Student-t

7.19

Since generally the population variance

of bk , var(bk) , is unknown, we estimate

^ k) which uses s

^ 2 instead of s 2.

it with var(b

t =

bk - b k

^ k)

var(b

bk - b k

=

se(bk)

t has a Student-t distribution with df=(T-K).

Copyright 1996 Lawrence C. Marsh

Interval Estimation

7.20

bk - bk

P -tc ٹ

ٹtc = 1 - a

se(bk)

tc is critical value for (T-K) degrees of freedom

such that P(t چtc) = a /2.

P bk - tc se(bk) ٹbk ٹbk + tc se(bk)

Interval endpoints:

= 1-a

bk - tc se(bk) , bk + tc se(bk)

Copyright 1996 Lawrence C. Marsh

Chapter 8

8.1

Hypothesis Testing

and

Nonsample Information

Copyright © 1997 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond

that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information should be addressed to the Permissions Department,

John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution

or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.

Copyright 1996 Lawrence C. Marsh

Chapter 8: Overview

1.

2.

3.

4.

5.

6.

7.

Student-t Tests

Goodness-of-Fit

F-Tests

ANOVA Table

Nonsample Information

Collinearity

Prediction

8.2

Copyright 1996 Lawrence C. Marsh

Student - t Test

8.3

yt = b1 + b2Xt2 + b3Xt3 + b4Xt4 + et

Student-t tests can be used to test any linear

combination of the regression coefficients:

H0: b1 = 0

H0: b2 + b3 + b4 = 1

H0: 3b2 - 7b3 = 21 H0: b2 - b3 5 ٹ

Every such t-test has exactly T-K degrees of freedom

where K=#coefficients estimated(including the intercept).

Copyright 1996 Lawrence C. Marsh

One Tail Test

8.4

yt = b1 + b2Xt2 + b3Xt3 + b4Xt4 + et

H0: b3 0 ٹ

H1: b3 > 0

b3

~ t (T-K)

t=

se(b3)

df = T- K

= T- 4

a

(1 - a)

0

tc

Copyright 1996 Lawrence C. Marsh

Two Tail Test

8.5

yt = b1 + b2Xt2 + b3Xt3 + b4Xt4 + et

H0: b2 = 0

H1: b2 ° 0

b2

~ t (T-K)

t=

se(b2)

df = T- K

= T- 4

a/2

(1 - a)

a/2

-tc

0

tc

Copyright 1996 Lawrence C. Marsh

Goodness - of - Fit

Coefficient of Determination

T

2

R =

SSR

=

SST

0 ٹR 1ٹ

2

S(yt - y)

^

2

t=1

T

S(yt - y)

t=1

2

8.6

Copyright 1996 Lawrence C. Marsh

Adjusted R-Squared

8.7

Adjusted Coefficient of Determination

Original:

2

R =

SSR

SST

= 1-

SSE

SST

Adjusted:

R = 12

SSE/(T-K)

SST/(T-1)

Copyright 1996 Lawrence C. Marsh

Computer Output

Table 8.2 Summary of Least Squares Results

Variable Coefficient Std Error t-value p-value

constant

104.79

6.48