Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

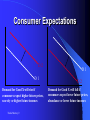

Demand and Supply Trudie Murray © Demand and Supply Game Place a value of each token Black = 50 cent Red = 20 cent Trudie Murray © Price rises when quantity supplied is scarce and demand increases Price decreases when quantity supplied increases and as a result demand increases Trudie Murray © Demand The amount consumers desire to purchase at various prices at any given time Demand does not necessarily mean a consumer WILL buy, but refers to a good or service they WOULD LIKE to buy Trudie Murray © Effective Demand • Consumers must be willing to buy AND be capable of paying the price set by the supplier Trudie Murray © Law of Demand If Price rises – Quantity demanded falls P Q If Price falls – Quantity demanded rises P Trudie Murray © Q Individual Demand Individual Demand Schedule Lists the different quantities of a good that an individual consumer is prepared to buy at each price Trudie Murray © Market Demand Market Demand Schedule Lists the different quantities of a good that all consumers in the market are prepared to buy at each price. It is derived by adding together all the individual demand schedules for the good Trudie Murray © Demand Schedule (Demand for coffee monthly) (1) Price (cent per g) (2) Chris’s demand (3) David’s demand (4) Total market demand (g) (g) (kg’s: 000s) A 20 28 16 700 B 40 15 11 500 C 60 5 9 350 D 80 1 7 200 E 100 0 6 100 Trudie Murray © Demand Curve At higher prices, consumers are generally willing to purchase less than at lower prices Demand curve is said to have a negative slope - downward sloping from left to right Trudie Murray © Point Price per g A 20 cent Market Demand 100 700 kilogrammes Price (cent per g) 80 60 40 Demand A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kilogrammes: 000s) 600 700 800 100 Point Price per g Market Demand A 20 cent 700 kilogrammes B 40 cent 500 kilogrammes Price (cent per g) 80 60 B 40 A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kilogrammes: 000s) 600 700 800 100 Point Price per g Market Demand A 20 cent 700 kilogrammes B 40 cent 500 kilogrammes C 60 cent 350 kilogrammes Price (cent per g) 80 C 60 B 40 A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kilogrammes: 000s) 600 700 800 100 D Price (cent per g) 80 60 Point Price per g Market Demand A 20 cent 700 kilogrammes B 40 cent 500 kilogrammes C 60 cent 350 kilogrammes D 80 cent 200 kilogrammes C B 40 A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kilogrammes: 000s) 600 700 800 E 100 D Price (cent per g) 80 60 Point Price per g Market Demand A 20 cent 700 kilogrammes B 40 cent 500 kilogrammes C 60 cent 350 kilogrammes D 80 cent 200 kilogrammes E 100 cent 100 kilogrammes C B 40 A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kilogrammes: 000s) 600 700 800 An Increase in Demand Price P D1 Trudie Murray © Q1 Q2 Quantity D2 A Decrease in Demand Price P D2 Trudie Murray © Q2 Q1 Quantity D1 Factors affecting the demand for a good The Demand Function Dx = f ( Px, Pog, Y, T, E, G, U) Trudie Murray © The Demand Function Dx = f ( Px, Pog, Y, T, E, G, U) Px = Goods which obey and do not obey the Law of Demand Pog = Price of Complimentary Goods and Cost of Substitute Goods Y = Income of consumer T = Consumer tastes and preferences E = Consumers expectations regarding future prices G = Government regulations U = Unplanned factors Trudie Murray © Demand for a good depends on its own price If price rises quantity demanded falls If price falls quantity demanded rises P2 P1 Q2 Trudie Murray © Q1 Quantity Demanded Demand for a good depends on the price of other goods • Complimentary Goods Goods which are used jointly. The use of one involves the use of the other - E.g. bread and butter, cars and petrol • Substitute Goods Goods which satisfy the same needs and thus can be considered as alternatives to each other – E.g. Coke and Pepsi or Tea and Coffee Trudie Murray © Complimentary Goods D1 D2 An increase in price of a complementary good causes the demand for good X to fall Trudie Murray © D2 D1 An fall in price of a complementary good causes the demand for good X to rise Substitute Goods (The Substitute Effect) D2 D1 An increase in price of a substitute good causes the demand for good X to rise Trudie Murray © D1 D2 An fall in price of a substitute good causes the demand for good X to fall Demand for a good depends on level of income (The Income Effect) • Normal Goods A normal good is a good with a positive income effect. A rise in income causes more of it to be demanded, while a fall in income causes less of it to be demanded • Inferior Goods An inferior good is a good with a negative income effect. A rise in income causes less of it to be demanded, while a fall in income causes more of it to be demanded Trudie Murray © Normal Goods D2 D1 A rise in income causes the demand for a normal good to increase from D1 to D2 Trudie Murray © D1 D2 An fall in income causes the demand for a normal good to fall from D1 to D2 Inferior Goods D1 D2 An increase in income causes the demand for an inferior good to fall from D1 to D2 Trudie Murray © D2 D1 A decrease in income causes the demand for an inferior good to rise from D1 to D2 Demand depends on Consumer Tastes If the movement in taste or preferences is in favour of the good it causes an increase in demand which shifts the demand curve to the right If the movement in taste or preferences is against the good it causes a fall in demand which shifts the demand curve to the left Trudie Murray © Movement in Taste D2 D1 A movement in taste in favour of a good causes demand to increase Trudie Murray © D1 D2 A movement in taste against a good causes demand to fall Demand for a good depends on the expectations of consumers Demand for a good will shift to the right if consumers expect: 1. 2. 3. The price of good X to be higher in the future e.g. property A scarcity of good X in the future e.g. oil Their incomes to be higher in the future e.g. promotion Demand for a good will shift to the left if consumers expect: 1. 2. 3. Trudie Murray © The price of good X to be lower in the future A plentiful supply of good X in the future Their incomes will be lower in the future Consumer Expectations D2 D1 Demand for Good X will rise if consumers expect higher future prices, scarcity or higher future incomes Trudie Murray © D1 D2 Demand for Good X will fall if consumers expect lower future prices, abundance or lower future incomes Demand for a good depends on government regulations If the government implement a programme which reduces consumption of a particular product than demand for this good will be affected E.g. The smoking ban / educational campaign to reduce alcohol consumption. Trudie Murray © Government Regulations Example: The Smoking Ban D1 D2 If the government implement a policy to restrict consumption demand for Good X will fall Trudie Murray © Demand for a good depends on unplanned factors If there is a sudden heat wave – an unplanned factor – this may result in an increase in demand for sunscreen and a decrease in the demand of home oil If flash floods occur across the country – an unplanned factor – this may result in an increase in the demand for Wellingtons. Trudie Murray © Unplanned Factors D2 D1 Trudie Murray © Factors such as weather can effect the demand for goods – e.g. a sudden heat wave would increase the demand for sunscreen Exceptions to the Law of Demand P D • • Giffen Goods Goods of ostentatious consumption (snob goods) • • Goods affected by consumers’ expectations Addictive Goods Trudie Murray © Supply The quantity of a good that firms are willing to make available over a particular period of time The supplier determines the level of output it is willing to supply at the prevailing market price Trudie Murray © Individual Supply Individual Supply Schedule Lists the different quantities of a good that an individual firm is willing to make available at each price Trudie Murray © Market Supply Market Supply Schedule Lists the total quantities of a good that all firms in the market are willing to make available at each price. It is derived by adding together all the individual supply schedules for the good Trudie Murray © Supply Schedule (supply of coffee monthly) Price of Coffee (cent per g) Bean Grower X's supply (kg’s) Total Market supply (kg’s: 000s) A 20 50 100 B 40 70 200 C 60 100 350 D 80 120 530 E 100 130 700 Trudie Murray © Supply Curve At higher prices, suppliers are willing to produce more of a good or service and supply it to the market Supply curve is said to have a positive slope – upwards from left to right indicating a positive relationship between supply and price Trudie Murray © 100 A P Q 20 100 80 Price (cents per g) 60 40 20 A Supply 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kg’s: 000s) 600 700 800 P Q A 20 100 B 40 200 100 Price (cents per g) 80 60 40 B A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kg’s: 000s) 600 700 800 P Q A 20 100 B 40 200 C 60 350 100 Price (cents per g) 80 60 C 40 B A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kg’s: 000s) 600 700 800 P Q A 20 100 B 40 200 C 60 350 D 80 530 100 Price (cents per g) 80 D 60 C 40 B A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kg’s: 000s) 600 700 800 80 Price (cents per g) P Q A 20 100 B 40 200 C 60 350 D 80 530 E 100 700 E 100 D 60 C 40 B A 20 0 0 100 Trudie Murray © 200 300 400 500 Quantity (kg’s: 000s) 600 700 800 Increase in Supply P Sx S1 Increase Q Trudie Murray © Increase/Decrease in Supply P S2 Decrease SX S1 Increase Q Trudie Murray © Factors effecting the supply of a good The Supply Function Sy = f ( Py, Pr, C, Tch, Tx, N, U) Trudie Murray © The Supply Function Sy = f ( Py, Pr, C, Tch, Tx, N, U) Py = Price of Good Y Pr = Price of related goods C = Cost of Production Tch = State of Technology Tx – Taxation / Subsidy N – number of sellers in the industry U = Factors outside the control of the firm Trudie Murray © Supply of a good depends on its own price If price rises quantity supplied rises If price falls quantity supplied falls P2 P1 Q1 Trudie Murray © Q2 Quantity Supplied Supply of a good depends on prices of related goods S1 S2 S1 An increase in price of a related good will cause a fall in the supply of Good Y Trudie Murray © S2 An fall in price of a related good will cause an increase in the supply of Good Y Supply of a good depends on the cost of production Causes of an increase in the cost of production: A rise in labour costs A rise in the cost of raw materials An increase in taxes A reduction in subsidies Causes of a decrease in the cost of production: A fall in labour costs A fall in the cost of raw materials A reduction in taxes An increase in subsidies Trudie Murray © Supply of a good depends on cost of production S1 S2 S1 An increase in the cost of production will cause a fall in the supply of Good Y Trudie Murray © S2 An fall in the cost of production will cause an increase in the supply of Good Y Supply of a good depends on the state of technology S1 S2 We do not generally discuss a ‘fall’ in technology – we assume any new method of production is an option for a firm An improvement in the state of technology will cause an increase in the supply of Good Y Trudie Murray © Supply of a good depends on the rates of taxation / granting of subsidies A reduction in taxes will result in a reduction in the cost of raw materials / production and supply will increase. An increase in subsidies granted to a firm for raw materials / labour employed will result in a reduction in costs and supply will increase Trudie Murray © Supply of a good depends on the rates of taxation / granting of subsidies S1 S2 S1 S2 An fall in the level of taxation / An increase in the level of taxation / decrease in subsidies will cause a fall in increase in subsidies will cause an increase in the supply of Good Y the supply of Good Y Trudie Murray © Supply of a good depends on the number of sellers in the industry If the number of sellers in the industry decrease (due to rationalisation) than overall quantity supplied will also decrease If the number of sellers in the industry increase than overall quantity supplied will also increase Trudie Murray © Supply of a good depends on the number of sellers in the industry S1 S2 S1 A decrease in the number of sellers in industry will cause a fall in the supply of Good Y Trudie Murray © S2 An increase in the number of sellers in industry will cause a rise in the supply of Good Y Supply of a good depends on factors outside the control of a firm / unforseen circumstances Favourable or unfavourable unplanned factors: Weather conditions e.g. floods or sunshine Strikes Shortage of raw materials Transport failure Trudie Murray © Supply of a good depends on factors outside the control of a firm S2 S1 S2 Favourable unplanned factors will cause an increase in supply and a shift to the right Trudie Murray © S1 Unfavourable unplanned factors will cause a decrease in supply and a shift to the left Methodology Students will be asked to think of three items on their desks and to secretly set a price for each one of them on the index card that will be handed out. They will then fold their index cards so it can stand upright on their desks Trudie Murray © Students will then be instructed to place their items by their price list Students will then be invited to go ‘shopping’ and check out all the prices in the ‘shop’ Trudie Murray © Lead the students into discussion asking questions such as the following: Now that you can see how other merchants priced their items, how will it effect your pricing of the same item? Were there some items that would be in high demand because of their low supply? How might that effect pricing? Trudie Murray © • Students may want to stock their ‘shelves’ differently after doing some comparisonshopping and seeing the availability of certain items. • Give the students the opportunity to price another 3 items of their choice and discuss their changes and why they were made. Trudie Murray © Market Equilibrium If no interference in the market occurs (by government or other agency) price will eventually settle at the level where quantity demanded equals quantity supplied. This position is called the market equilibrium Trudie Murray © Market Equilibrium Price 100 80 60 40 20 D1 S2 0 quantity 0 100 Trudie Murray © 200 300 400 500 600 700 800 Market Equilibrium and Price If the price on the market is above the equilibrium price, there will be a downward pressure on the price Quantity supplied will exceed quantity demanded and producers will lower the price to get rid of surplus stock P Trudie Murray © Market Equilibrium and Price If the price on the market is below the equilibrium price, there will be a upward pressure on the price Quantity demanded will exceed quantity supplied. Scarcity would exist and price would increase P Trudie Murray © An Increase in Demand Causes: A decrease in the price of the good itself An increase in the price of a substitute good A fall in the price of a complimentary good An increase in income (if the good is normal) A change in taste in favour of the good Expectations of higher prices in future or scarcity Favourable unplanned factors Trudie Murray © Q2 > Q1 and P2 > P1 Price S1 P2 P1 D2 D1 Q1 Trudie Murray © Q2 Quantity A Decrease in Demand Causes: An increase in the price of the good itself An fall in the price of a substitute good A increase in the price of a complimentary good An fall in income (if the good is normal) A change in taste away from the good Expectations of lower prices in future or greater supplies Implementation of government regulations Trudie Murray © Q2 < Q1 and P2 < P1 Price S1 P1 P2 D1 D2 Q2 Trudie Murray © Q1 Quantity An Increase in Supply Causes: A fall in the price of a related good A fall in the cost of production An improvement in technology Favourable unplanned factors A reduction in taxation / granting of subsidy Increase in the number of sellers in the industry Trudie Murray © Q2 > Q1 and P2 < P1 Price S1 S2 P1 P2 D1 Q1 Q2 Trudie Murray © Quantity A Fall in Supply Causes: A rise in the price of a related good A rise in the cost of production Unfavourable unplanned factors An increase in taxation / decrease in subsidies A decrease in the number of sellers in the industry Trudie Murray © Q2 < Q1 and P2 > P1 Price S2 S1 P2 P1 D1 Q2 Q1 Trudie Murray © Quantity Watch the following clip http://www.learner.org/resources/series79.html?pop=yes &vodid=561786&pid=353# Demand and Supply video Trudie Murray © Look at the following website and complete the Economics Challenge http://www.business2000.ie/resources/Revision_Quizzes.html# Trudie Murray © Contact Me [email protected] Trudie Murray ©