Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

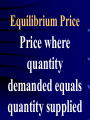

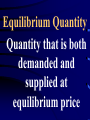

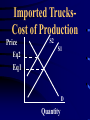

Prices (Supply + Demand) Market System • People’s self-interest drives the economy • Consumers want to minimize their costs (Law of Demand) • Producers want to maximize their profits (Law of Supply) Equilibrium • Demand and supply are in balance • Quantity supplied = Quantity demanded • Point at which demand curve crosses supply curve • Equilibrium Price • Equilibrium Quantity Equilibrium Price Price where quantity demanded equals quantity supplied Equilibrium Quantity Quantity that is both demanded and supplied at equilibrium price Equilibrium Price S Peq D Quantity Shortage • Quantity demanded greater than quantity supplied at a certain price • Shortage causes price to increase - less is demanded - more is supplied - shortage reduced prices go back down Surplus • Quantity supplied is greater than the quantity demanded at a certain price • Surplus causes price to decrease more is demanded - producers make less - supply is decreased prices go back up Shortage and Surplus Price Surplus S Eq. Shortage D Quantity Prices Questions • If a product is all of a sudden in high demand, what do you think will happen to its price? • If a product’s popularity drops significantly, what do you think will happen to its price? • If a product is much more available than it used to be, what do you think will happen to its price? • If a product is less available to purchase, what do you think will happen to its price? Equilibrium and Demand Changes • New equilibrium is achieved when supply curve moves to meet new demand • Demand Increase= if supply does not adjust prices rise, quantity exchanged rises • Demand Decrease=if supply does not adjust prices fall, quantity exchanged falls Equilibrium and Demand Changes: Demand Increase • Copy the Graph on the Dry-Erase Board • Find & label the Peq1 and the Qeq1 • Label the Demand Line D1 • Show an increase in demand (shift in demand) • Find the new Peq2 and Qeq2 Equilibrium and Demand Changes:Demand Decrease • Copy the Graph on the Dry-Erase Board • Find & label the Peq1 and the Qeq1 • Label the Demand Line D1 • Show a decrease in demand (shift in demand) • Find the new Peq2 and Qeq2 Equilibrium and Supply Changes:Supply Increase • Copy the Graph on the Dry-Erase Board • Find & label the Peq1 and the Qeq1 • Label the Demand Line D1 • Show an increase in supply (shift in supply) • Find the new Peq2 and Qeq2 Equilibrium and Demand Changes:Supply Decrease • Copy the Graph on the Dry-Erase Board • Find & label the Peq1 and the Qeq1 • Label the Demand Line D1 • Show a decrease in supply (shift in supply) • Find the new Peq2 and Qeq2 Equilibrium and Supply Changes • New equilibrium is achieved when demand curve moves to meet new supply • Supply Increase=if demand does not adjust prices fall, quantity exchanged rises • Supply Decrease=if demand does not adjust prices rise, quantity exchanged falls • • • • • • • • Draw graphs for each of the following 8 situations and explicitly write what happened to Peq (Increase, Decrease or Indeterminate?). Name each of the graphs the scenario provided 1) Supply: No Change Demand: Increase 2) Supply: Decrease Demand: No Change 3) Demand: No Change Supply: Increase 4) Demand: Decrease Supply: No Change • • • • • • • • 5) Supply: Increase Demand: Increase 6) Supply: Increase Demand: Decrease 7) Supply: Decrease Demand: Decrease 8) Supply: Decrease Demand: Increase Graph the effects of an increase in the price of gas on UPS Imported TrucksCost of Production Price Eq2 S2 S1 Eq1 D Quantity Graph the effects of increased purchasing power for teenagers after an increase in the minimum wage Effects of Added Income Price S Eq2 Eq1 D2 D1 Quantity Graph the effects of advancements in computers on the architecture industry Computers on Architecture Technology Price S1 Eq1 Eq2 D Quantity S2 Laissez Faire • What is Laissez Faire? •Does the United States Government leave the economy alone? •In what ways does the government get involved with the economy? Government Intervention • Limit imports- keep prices high • Govt. buying agricultural products to increase demand and keep prices high • Rent controls • Minimum wage Forms of Gov’t Intervention • Price Floor • Price Ceiling Imagine the following scenario: You are an unemployed single parent of two young children living in Los Angeles. You interview at the Los Angeles Times for a position for an assistant in the mail room. I, the interviewer, say that the hourly wage is negotiable and asks you what the lowest hourly wage you would be willing to work for is. What do you say? How did you come up with that number? Price Floor •Gov’t Regulation that establishes a minimum level for prices. It is illegal to charge less than that price Price Floor Example – Minimum Wage • Minimum Wage – Wage that the lowest amount an employer legally can pay a worker for a job Agriculture Products - Price Floor Example • Agriculture Products Unusually good weather leads to corn farmers being able to produce an unusually large corn crop. What happens to the Price Equilibrium? Suppose that if Farmers sell at this price, they will not be able to cover their costs, many will lose their land. What can be done? Agriculture Products - Price Floor Example Cont’d • Gov’t sets a base price for corn that will guarantee farmers a minimum level of income. What will result from this government decision? Government buys the surplus Rent • What do you guess is the average monthly rent for a 2 bedroom 1 bathroom apartment in • Yorba Linda? • Manhattan? Price Ceiling • Gov’t regulation that establishes a maximum price for a particular good. Producers cannot charge prices above this set level. Price Ceiling Example – Rent Control • Suppose a city gets so popular that many people want to move there. What happens to the price equilibrium? Price Ceiling Example – Rent Control Cont’d • Supply and Demand would force a large portion of people living there to move. To prevent this from happening, some cities set a price ceiling on rent Price Ceiling - Consequences •Takes away incentive to enter the market and improve the product •Creates Shortages

![[A, 8-9]](http://s1.studyres.com/store/data/006655537_1-7e8069f13791f08c2f696cc5adb95462-150x150.png)