Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

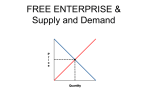

FREE ENTERPRISE & Supply and Demand At the end of class today, for a grade: 1. Draw the supply and demand graph, with these parts labeled: supply line, price, quantity, demand line, equilibrium price 2. When does a surplus occur? 3. When does a shortage occur? Review Types of Economies • Fill in the blank using command economy, traditional economy, market economy, laissez faire, Karl Marx, Adam Smith, Profit motive, central planners 1. In a _______________ custom and habit determine the answers to the 3 economic questions. IF YOU CAN ANSWER THESE QUESTIONS, YOU UNDERSTAND SUPPLY AND DEMAND!!!!! 1. If you were a candy store owner, would you be more willing to sell candy at $1 a piece or $2 a piece? Why? 2. If you were buying candy, would you be more willing to BUY candy at $1 a piece or at $2 a piece? Why? Types of Economies Review 1. Which type of economy combines the market economy and the command economy? 2. Which type of economy are economic decisions based on customs and habits of the past? 3. Which type of economy does the government control all aspects of production? 4. Which type of economy do individuals and firms have the freedom to produce what they want? • Free Market (Capitalism) – Because we have a generally free market people have the freedom to make money in any way they choose. This can be called having “free enterprise.” – Invisible Hand: society benefits when individuals can pursue their own interests without interference from the government. – Instead of the gov’t, supply and demand determines prices, which determines who can buy certain goods/services. – ANSWER: Who determines price in the command economy? – ANSWER: If you were opening a business in the free market how would you decide what to make? 4 Characteristics of Free Enterprise 1. Individuals can choose how much they want to work and what skills they want to have. What do individuals think about when choosing a job? 2. Voluntary Exchange: people determine what and how much they want to buy and sell. If something is “voluntary” it means you are not forced. 3. Businesses are motivated by making as much profit as possible. What is this called? ___________ _______________ 4. Prices are determined by the supply and demand for a good. • a. b. c. d. Which economic system will most likely promote individual initiative by involving free enterprise? socialism Capitalism Feudalism communism Which system has the most unregulated flow of economic activity? a. market b. Mixed c. Command d. traditional Law of Supply • Businesses will produce more products when they know they can sell them at a higher price. – Ex: If you know you can sell your sneakers for $100 a pair you will want to make more sneakers than if you could only sell them for $10. Law of Demand • Consumers will demand (want) more of a good when the price for the good is low. – Ex: As a consumer you will want to buy more sneakers if they cost $10 rather than if they cost $100. • So what will be the price of the sneakers? $100, $10 or somewhere in between? The Supply and Demand Graph • Where the 2 lines intersect is the price the good will be sold at. At $45 a consumer is willing to buy (demands) 2 pairs, and the producer is willing to supply 2 pairs of sneakers. Supply Price $100 $45 Why wouldn’t a producer sell the sneaker for $100? Demand 2. Why wouldn’t a producer sell the sneaker for $10? 1. $10 1 2 Quantity 3 • Equilibrium price: the price where supply and demand are equalthe highest price a good can be sold at and not have a shortage (not enough) or surplus (too much). – The Equilibrium Price prevents producers from charging too much for a good, because they will never sell it at a high price if there is no demand. Price $100 Supply $45 Equilibrium Price = ???? $10 Demand 1 2 Quantity 3 Shortage and Surplus • What does it mean to have a shortage? • What does it mean to have a surplus? Shortage vs. Surplus • What happens to the price if we have too much supply and no demand for a good? – SURPLUS: Supply is greater than demand = lower price • SALES at stores are usually the result of a surplus. Shortage vs. Surplus • What happens to the price if we have a lot of demand but not enough supply of a good? – SHORTAGE: Demand is greater than supply = higher price • GAS PRICES go up during gas shortages. SUPPLY AND DEMAND PRACTICE 1. Draw a Supply and Demand Graph. Label (supply “S”, demand “D”, equilibrium price “E,” Price axis, and Quantity axis. Price Units Demanded Units Supplied $5 10 60 $4 18 51 $3 28 41 $2 38 29 $1 52 10 Gum Supply and Demand 2. What happens if demand is high Graph and supply is low? a) When gum costs $1 what quantity is demanded? b) When gum cost $1 what quantity is supplied? c) What is the shortage of gum (demanded - supplied) ? 3. What happens is demand is low but supply is high? a) Gum costs $3 what quantity is demanded? b) Gum costs $3 what quantity is supplied? c) What is the surplus of gum (supplied - demanded)? Gum Supply and Demand on the graph at what price Graph4.theCircle quantity supplied and demanded are the same (equal)?_____________ What is this point called? _________________________ 5. What would happen if the government set the price of gum at $4? 6. What would happen if the government set the price of gum at $2? 7. How does having price set by supply and demand benefit consumers? Assignment: 1. Draw the supply and demand graph, with these parts labeled: supply line, price, quantity, demand line, equilibrium price Each Person must have their own 2. When does a surplus occur? 3. When does a shortage occur? PREVIEW FOR TOMORROW What might cause demand in a product to increase? Price Quantity PREVIEW FOR TOMORROW What might cause demand in a product to decrease? Price Quantity PREVIEW FOR TOMORROW What might cause SUPPLY in a product to increase? Price Quantity PREVIEW FOR TOMORROW What might cause SUPPLY in a product to decrease? Price Quantity