Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

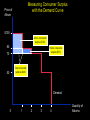

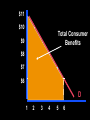

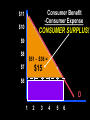

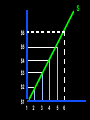

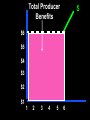

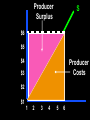

Chapter 7 Consumers, Producers and the Efficiency of Markets Objectives 1. Understanding how consumer’s willingness and ability to pay for a good determines the demand curve. 2. Learn the concept of consumer surplus and how to measure it. 3. Understand how sellers cost of production determine the supply curve. Objectives 4. Learn the concept of producer surplus and how to measure it, and ... 5. ... recognize that market equilibrium maximizes total surplus in a market. Market Equilibrium Revisited Does the equilibrium price and quantity result in the maximum total welfare of buyer and seller? S PE D QE Market Equilibrium Revisited Does the equilibrium price and quantity result in the maximum total welfare of buyer and seller? Market equilibrium illustrates the way markets allocate scarce resources. But does it answer whether that market allocation is desirable? Turn to Welfare Economics to answer the question. Welfare Economics Is the study of how the allocation of resources affects economic well being. – Buyers and sellers receive benefits from taking part in the market. – The equilibrium in a market makes the sum of these benefits as large as possible. Welfare Economics Equilibrium in the market results in maximum benefits, and therefore total welfare for both the buyer and the seller. Welfare Economics from the Buyer Side and the Seller Side: – Consumer Surplus – Producer Surplus Welfare Economics: Consumer Surplus Market Demand Curve: depicts the various quantities that buyers would want to purchase at different prices. What determines how much a consumer would be willing to pay (the maximum price) for a good or service? – Answer: The expected benefits received or Utility. Utility is... … the satisfaction (benefit) that a consumer expects to receive from consuming a good or service. …the power to satisfy a want. Marginal Utility (MU) is... …the amount of utility (satisfaction) that one more or one less unit of consumption adds to or subtracts from total utility. – Consumers try to obtain the largest possible total satisfaction (utility) from the mix of goods and services they buy with their incomes. Consumer Surplus is... …the maximum amount a consumer will be willing to pay for a good depends upon the expected utility (benefits) of that good. – Willingness to Pay: The maximum price that a buyer is willing and able to pay for a good. Measures how much the buyer values the good or service. Measuring Consumer Surplus with the Demand Curve Price of Album $100 John’s consumer surplus ($10) 80 Paul’s consumer surplus ($10) 70 Total consumer surplus ($40) 50 Demand 0 1 2 3 4 Quantity of Albums Four Possible Buyers’ Willingness to Pay... Price Buyer Quantity Demanded More than $100 None 0 $80 to $100 John 1 $70 to $80 John, Paul 2 $50 to $70 John, Paul, George 3 $50 or less Ringo 4 Consumer Surplus: Verbal Definition The amount a buyer is willing to pay for a good minus the amount the buyer actually pays for it. D How the Price Affects Consumer Surplus Figure 7-3 (a) -- Consumer Surplus at Price P1 Price A Consumer Surplus P1 B C Demand 0 Q1 Quantity How the Price Affects Consumer Surplus Figure 7-3 (b) -- Consumer Surplus at Price P2 Price A Initial Consumer Surplus Additional consumer surplus to initial consumers P1 P 2 C B Consumer Surplus to New Consumers F D E Demand 0 Q1 Q 2 Quantity Consumer Surplus: Graphical S Pmax Consumer Surplus PE D QE Consumer Surplus and Market Price The area below the demand curve and above the market price measures the consumer surplus in a market. Hence, – A lower market price will increase consumer surplus – A higher market price will reduce consumer surplus Consumer Surplus and Economic Well-Being Consumer surplus, the amount that buyers are willing to pay for a good minus the amount they actually pay for it, measures the benefit that buyers receive from a good as the buyers themselves perceive it. Consumer Surplus: Mathematically Maximum Market Price = $11 Price = $6 Quantity Purchased = 6 Assume: Price drops $1 for every additional unit sold. Consumer Surplus = $15 $51 - $36 = $15 ($11+$10+$9+$8+$7+$6) - ($6 x 6) = $15 $11 $10 $9 $8 $7 Market Price $6 D 1 2 3 4 5 6 Quantity Purchased $11 $10 Total Consumer Benefits $9 $8 $7 $6 D 1 2 3 4 5 6 $11 $10 $9 $8 Consumers Expense $7 $6 D 1 2 3 4 5 6 $11 Consumer Benefit -Consumer Expense $10 CONSUMER SURPLUS! $9 $8 $51 - $36 = $7 $15 $6 D 1 2 3 4 5 6 Quick Quiz Illustrate, with a demand curve, the consumer surplus for turkey. Explain in words what consumer surplus measures. Discuss changes in consumer surplus as price changes. Producer Surplus Market Supply Revisited: – Depicts the various quantities that suppliers would be willing to sell at different prices. – May be viewed as a measure of supplier costs, i.e.. the opportunity cost to the seller of supplying various quantities of the good. Producer Surplus Market Supply: The marginal opportunity cost of production increases as market output expands. Because the producer’s cost is the lowest price he/she would accept it may be considered a measure of his/her willingness to sell. Measuring Consumer Surplus with the Supply Curve Price of House Painting Supply Total producer surplus ($500) $900 800 Georgia’s producer surplus ($200) 600 500 Grandma’s producer surplus 0 1 2 3 4 Quantity of Houses Painted Figure 7-5a The Costs of Four Possible Sellers... Seller Cost Mary $900 Frida 800 Georgia 600 Grandma 500 Producer Surplus: Verbal Definition The amount a seller is paid minus the cost of production. Producer surplus measures the benefit to sellers of participating in a market. S How the Price Affects Producer Surplus Figure 7-6 (a) -- Producer Surplus at Price P1 Price Supply P1 B C A 0 Producer Surplus Q1 Quantity How the Price Affects Producer Surplus Figure 7-6 (b) -- Producer Surplus at Price P2 Additional producer surplus to initial producers Price Supply D P E F 2 P1 C A 0 Producer surplus to new producers B Producer Surplus Q1 Q 2 Quantity Producer Surplus: Mathematically Minimum Market Price = $1 Price = $6 Quantity Sold = 5 Assume: Price increases $1 for every additional unit sold. Producer Surplus = $15 $30 - $15 = $15 ($6 x 5) - ($1 +$2 + $3 + $4 + $5) = $15 S $6 $5 $4 $3 $2 $1 1 2 3 4 5 6 Total Producer Benefits S $6 $5 $4 $3 $2 $1 1 2 3 4 5 6 Producer Surplus S $6 $5 $4 Producer Costs $3 $2 $1 1 2 3 4 5 6 Market Efficiency Under the assumptions of perfect competition and no externalities, the economic well-being of a society is measured as the sum of consumer surplus and producer surplus. Market Efficiency is attained when total surplus is maximized, a point where resource allocation is efficient. Economic Well-Being and Total Surplus Consumer Surplus = Value to _ Amount paid buyers by buyers and Producer Surplus = Amount received _ Cost to by sellers sellers Economic Well-Being and Total Surplus Total Surplus = Consumer Surplus + Producer Surplus or Total Surplus = Value to _ Cost to buyers sellers Market Efficiency S PE D Market Efficiency Consumer Surplus S PE Producer Surplus D Market Efficiency In addition to market efficiency, a social planner might also care about equity – the fairness of the distribution of well-being among the various buyers and sellers. Market Efficiency: Three observations Free markets allocate the supply of goods to the buyers who value them most highly. Free markets allocate the demand for goods to the sellers who can produce them at least cost. Free markets produce the quantity of goods that maximizes the sum of consumer and producer surplus. Market Efficiency: Invisible Hand In a free market system the many buyers and sellers are interested in their own well-being, self-interest. As market participants are motivated by self-interest a process of coordination and communication takes place so that buyers and sellers are directed to the most efficient outcome. As if by an Invisible Hand, the free market system reaches efficiency. The Efficiency of the Equalibrium Price S Value to Buyers Cost to sellers Cost to sellers 0 Equilibrium Value to buyers is greater than cost to sellers. Value to Buyers quantity Value to buyers is less than cost to sellers. D Quantity Quick Quiz Draw the supply and demand for turkey. In the equilibrium, show the producer and consumer surplus. Explain why producing more turkey will lower total surplus. Market Failure If a market system is not one of perfect competition, control over prices leads to Market Power. – The ability by one buyer or seller to control market price. Market Power causes markets to be inefficient, and thus fail. Market Failure If a market system affects individuals other than buyers and sellers of that market, side-effects are created and called Externalities. – Benefits or costs imposed on a third party who is not the consumer or the producer. Externalities cause markets to be inefficient, and thus fail. Externalities Externalities are created when a market outcome affects individuals other than buyers and sellers in that market. Externalities cause welfare in a market to depend on more than just the value to the buyers and cost to the sellers. When buyers and sellers do not take externalities into account when deciding how much to consume and produce, the equilibrium in the market can be Summary Consumer surplus measures the benefit buyers get from participating in a market. Consumer surplus can be computed by finding the area below the demand curve and above the price. Summary Producer surplus measures the benefit sellers get from participating in a market. Producer surplus can be computed by finding the area below the price and above the supply curve. Summary The equilibrium of demand and supply maximizes the sum of consumer and producer surplus. This is as if the invisible hand of the marketplace leads buyers and sellers to allocate resources efficiently. Markets do not allocate resources efficiently in the presence of market failures. Summary An allocation of resources that maximizes the sum of consumer and producer surplus is said to be efficient. Policymakers are often concerned with the efficiency, as well as the equity, of economic outcomes.