Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

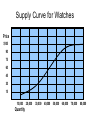

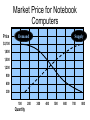

Introduction to Business Chapter 1 Economic Decisions and Systems Warm-Up • Answer the following in complete sentences. – Is there a difference between needs and wants? Explain your answer. Needs and Wants • Need: things you cannot live without – Examples • Water, food, shelter, clothing Wants: things you would like to have but can live without They add comfort and Pleasure to life Goods and Services • Goods – Things you can see and touch • Examples: computers, food, clothes • Services – When someone does something for someone • Examples: hair care, dental care, doctor visits Economic Resources • The means through which goods and services are produced Warm-Up • When Campbell’s Soup makes it’s Chicken Noodle Soup, what resources to they use to make the soup? Be specific and list all the resources you can think of. Natural Resources • Raw materials supplied by nature – Examples: lumber, coal, oil, water, animals, crops Human Resources • People producing the goods and services – Examples: farmers, factory workers, managers, accountants, entrepreneurs Capital Resources • The products and money used in the production of goods and services – Examples: money, tools, equipment • NOTE: Economic Resources are Limited The Basic Economic Problem • Scarcity – Not having enough resources to satisfy every need Decision Making • Tradeoff – When you give up something to have something else Opportunity Cost Definition: the value of your next best alternative that you did not choose What did you give up or not have when making a decision to buy something or obtain a goal? Decision Making Process • Specify – Determine your goal. What is your need/want • Search – Gather information • Sift – Look at all options and opportunity costs • Select – Make a choice and act on it • Study – Evaluate the result Warm-up • Identify the possible opportunity cost for each of the following. – Trying out for an athletic team – Accepting a part-time job – Studying for an important exam – Saving money to buy a used car – Obtaining a loan to start a business Economic Systems The Three Economic Questions 1. What to produce? • Depends on resources, climate, and education 2. How to produce? • Skilled/unskilled labor; technology available 3. What needs and wants to satisfy? • What is most critical Types of Economies • Command Economy – Government owns most of the resources and make most of the economic decisions. Types of Economies • Market Economy: People rather than the government own the resources and run the business. Types of Economies • Traditional Economy – Goods and services are produced the same way for generations – Countries with traditional economies do not participate in the global economy Does our society have any elements of a traditional economy? Mixed Economy • A combination of a market economy and a command economy. – U.S. has a mixed economy (the dominate economy is a market economy) The U.S. Economic System • Capitalism – Private ownership of resources by individuals not government • Free to decide what to produce and buy Warm-Up • What are some disadvantages of living in a market economy? Four Principles of the U.S. Economy • Private Property – Individuals can own, use, or dispose of things of value • Freedom of Choice – Make decisions independently and must accept consequences of those decisions Four Principles of the U.S. Economy • Profit – Formula: Price – Cost = Profit • Price you sell the product – amount producer spends to make product = left over profit – Making money (Profit) is the heart of the private enterprise system Competition • Contest among sellers to win customers. How does competition affect consumers? – Better customer service – Good quality products – Fair prices Warm-Up • What are the 5 steps in the decisionmaking process? • List the three components of economic resources and give an example of each. Supply and Demand • Consumers – anyone who buys or uses products. • Producers – Individuals/organizations that determine what products/services will be available for sale Demand • Quantity of goods that consumers are willing and able to buy – Law of Demand • As prices go up, demand goes down – Example: of a cheeseburger cost $1 each we might buy more than if they are $10 each Demand Curve for Movies Price $10.50 9.00 7.50 6.00 4.50 3.00 1.50 1,000 Quantity 2,000 3,000 4,000 5,000 6,000 7,000 Supply • Quantity of products that Producers are willing and able to make available for sale – Law of Supply • As prices go up, supply goes up • Example: if you are a supplier of computers you might make more available at $800 than at $200 Supply Curve for Watches Price $105 90 75 60 45 30 15 10,000 Quantity 20,000 30,000 40,000 50,000 60,000 70,000 80,000 Market Price • Point at which supply and demand are equal. Market Price for Notebook Computers Price Demand Supply $2,100 1,800 1,500 1,200 900 600 300 100 Quantity 200 300 400 500 600 700 800 Warm-up • List the three economic resources and give an example of each. • List the 5 decision making steps and give an example of each. Warm-Up • Explain the following terms: – Freedom of choice – Capitalism – Right to private property