Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

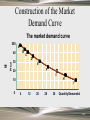

Supply and Demand Chapter 3 McGraw-Hill/Irwin Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved. The Market • How do market mechanisms decide WHAT, HOW, and FOR WHOM to produce? – What determines the price of a good or service? – How does the price of a product affect its production or consumption? – Why do prices and production levels often change? 3-2 Market Participants • A good way to start learning how markets work is to see who participates in them – Over 310 million consumers, 25 million firms, and tens of thousands of government agencies participate directly in the U.S. economy – Millions of international buyers and sellers also participate in U.S. markets 3-3 Maximizing Behavior • All participants have limited resources and strive to maximize outcomes – Consumers seek to maximize utility – Businesses try to maximize profits through efficient production – Government seeks to maximize general welfare 3-4 Specialization and Exchange • We interact in markets because: – Individuals are not capable of producing everything they need or want – We face limits on time, energy, and other resources, so it makes sense to specialize in production and trade for other goods and services 3-5 The Circular Flow • Four different groups participate in our economy: – – – – Consumers Business firms Government International participants 3-6 The Two Markets • Factor markets: Any place factors of production (e.g., land, labor, capital) are bought and sold • Product Markets: Any place finished goods and services are bought and sold 3-7 The Circular Flow Goods and services demanded Consumers Product markets Governments International participants Goods and services supplied Business Firms Factors of production supplied International participants Factor markets Factors of production demanded 3-8 Dollars and Exchange • A market exists wherever and whenever an exchange takes place • Every market transaction involves an exchange of dollars for goods or resources • Money is critical in facilitating market exchanges and the specialization it permits 3-9 Supply and Demand • There must be a buyer and a seller in every market transaction – The seller is on the supply side of the market – The buyer is on the demand side 3-10 Supply and Demand • Supply: The ability and willingness to sell specific quantities of a good at alternative prices in a given time period, ceteris paribus • Demand: The ability and willingness to buy specific quantities of a good at alternative prices in a given time period, ceteris paribus 3-11 Individual Demand • Demand exists only if someone is willing and able to pay for a good or service • An individual must consider the opportunity cost associated with a purchase, since it involves a tradeoff due to limited resources 3-12 Individual Demand • Demand schedule: A table showing quantities of a good a consumer is willing and able to buy at alternative prices in a given time period, ceteris paribus – “Demand” is an expression of consumer buying intentions – of a willingness to buy – not a statement of actual purchases 3-13 The Demand Curve • Demand curve: A curve describing quantities of a good a consumer is willing and able to buy at alternative prices in a given time period, ceteris paribus – A graphical illustration of a demand schedule • Demand curves are downward sloping 3-14 The Law of Demand • Law of Demand: The quantity of a good demanded in a given time period increases as its price falls, ceteris paribus 3-15 Demand Schedule and Curve Demand Schedule Quantity Price Demanded $50 1 45 2 40 3 35 5 30 7 25 9 20 12 15 15 10 20 PRICE $50 45 40 35 30 25 20 15 10 5 0 A B C D E F G H I 2 4 6 8 10 12 14 16 18 20 Quantity 3-16 Determinants of Demand • Determinants of market demand include: – – – – – Consumer tastes Consumer income Availability and prices of other goods Consumer expectations Number of buyers in the market 3-17 Types of Other Goods • Substitute goods substitute for each other – When the price of good x rises, the demand for good y increases, ceteris paribus • Complementary goods are frequently consumed together – When the price of good x rises, the demand for good y falls, ceteris paribus 3-18 Ceteris Paribus • Recall that to simplify their models economists focus on only one or two forces at a time and assume nothing else changes • Ceteris paribus: The assumption of nothing else changing 3-19 Shifts in Demand • A demand curve (schedule) is valid only if its underlying determinants remain constant • Determinants of demand can and do change • Shift in demand: A change in the quantity demanded at any given price 3-20 Movements vs. Shifts • Changes in quantity demanded: Movements along a demand curve in response to changes in price for the good • Changes in demand: Shifts of the demand curve due to changes in the determinants of demand, which change the relationship between price and quantity demanded 3-21 Movements vs. Shifts PRICE Shift in demand $45 d2 40 d1 35 30 25 g1 Movement along curve 20 D2 15 Increased demand D1 Initial demand 10 5 0 2 4 6 8 10 12 14 16 18 20 22 Quantity 3-22 Market Demand • Market demand: Total quantities of a good or service people are willing and able to buy at alternative prices in a given time period – The sum of individual demands, as determined by the number of potential buyers, their respective tastes and incomes, other goods, and expectations 3-23 Construction of the Market Demand Curve Quantity Demanded Price Tom + George + Lisa + Me = Market Demand A 50 1 4 0 0 5 B 45 2 6 0 0 8 C 40 3 8 0 0 11 D 35 5 11 0 0 16 E 30 7 14 1 0 22 F 25 9 18 3 0 30 G 20 12 22 5 0 39 H 15 15 26 6 0 47 I 10 20 30 7 0 57 3-24 Construction of the Market Demand Curve Tom’s demand curve George’s demand curve Lisa’s demand curve $50 My demand curve Price 40 30 + 20 + + = 10 0 4 8 12 16 0 4 8 12 16 20 24 28 0 4 8 12 0 4 8 12 Quantity Demanded 3-25 Construction of the Market Demand Curve The market demand curve $50 A B = Price 40 C D 30 E F 20 G H 10 0 4 12 20 28 36 I Quantity Demanded 3-26 Supply • Market supply: The total quantities of a good that sellers are willing and able to sell at alternative prices in a given time period, ceteris paribus 3-27 Determinants of Supply • The determinants of market supply include: – Technology – Factor costs – Other goods – Taxes and subsidies – Expectations – Number of sellers 3-28 Law of Supply • Law of Supply: The quantity of a good supplied in a given time period increases as its price increases, ceteris paribus • Supply curves are upward-sloping to the right 3-29 Market Supply • The market supply curve is just a summary of the supply intentions of all producers. • Market supply is an expression of sellers’ intentions – an offer to sell – not a statement of actual sales. 3-30 Market Supply Quantity Supplied By: Price Ann + Bob + Cory = Market j $50 94 35 19 148 i 45 93 33 14 140 h 40 90 30 10 130 g 35 86 28 0 114 f 30 78 12 0 90 e 25 53 9 0 62 d 20 32 7 0 39 c 15 20 0 0 20 b 10 10 0 0 10 3-31 Market Supply Price Ann’s supply curve Bob’s supply curve + Cory’s supply curve + = Quantity Supplied 3-32 Market Supply = Price Quantity supplied increases as price rises Quantity Supplied 3-33 Shifts of Supply • A supply curve is valid only if its underlying determinants remain constant • Determinants of supply can and do change • Shift in supply: A change in the quantity supplied at any given price 3-34 Movements vs. Shifts • Changes in quantity supplied: Movements along the supply curve due to changes in price • Changes in supply: Shifts in the supply curve due to changes in the determinants of supply – An increase in supply is a rightward shift – A decrease in supply is a leftward shift 3-35 Equilibrium • Only one price/quantity combination is compatible with buyer’s and seller’s intentions • Equilibrium price: The price at which the quantity of a good demanded equals the quantity supplied in a given time period – Equilibrium occurs at the intersection of the supply and demand curves 3-36 Equilibrium Price Price Quantity Supplied Quantity Demanded $50 148 surplus 5 45 140 surplus 8 40 130 surplus 11 35 114 surplus 16 30 90 surplus 22 25 62 surplus 30 20 39 equilibrium 39 15 20 shortage 47 10 10 shortage 57 3-37 Equilibrium Price Price $50 45 40 35 Market demand Market supply At the equilibrium price: quantity demanded = quantity supplied 30 25 20 15 Equilibrium price 10 5 0 25 39 50 75 100 125 Quantity 3-38 Market Clearing • The equilibrium price reflects a compromise between buyers and sellers – Not everyone is happy, as the price is too high for some buyers and too low for some sellers • The unique outcome at market equilibrium is efficient 3-39 The Invisible Hand • Market mechanism: The use of market prices and sales to signal desired outputs (or resource allocations) • Adam Smith characterized this market mechanism as the invisible hand 3-40 Market Surplus • Market surplus: The amount by which the quantity supplied exceeds the quantity demanded at a given price – excess supply • A market surplus will emerge when the market price is above the equilibrium price 3-41 Market Shortage • Market shortage: The amount by which the quantity demanded exceeds the quantity supplied at a given price – excess demand • A market shortage will emerge when the market price is below the equilibrium price 3-42 Surplus and Shortage Price $50 Market demand 45 40 35 Surplus 30 25 Market supply x y 20 15 10 5 0 Shortage 25 39 50 75 100 125 Quantity 3-43 Self-Adjusting Prices • Buyers and sellers will change their behavior to overcome a surplus or shortage • Only at the equilibrium price will no further adjustments be required 3-44 Surplus and Shortage Price $50 Market demand 45 40 35 30 25 Surplus x y 20 15 10 5 0 Market supply Equilibrium price Shortage 25 39 50 75 100 125 Quantity 3-45 Changes in Equilibrium • No equilibrium price is permanent • Equilibrium price and quantity will change whenever the supply or demand curve shifts – Shifts are due to a change in supply or demand resulting from a change in any of the underlying determinants 3-46 Change in Equilibrium: Demand Shift Price $50 Market supply 40 E2 30 New demand E1 20 10 0 Initial demand 25 50 75 100 Quantity 3-47 Change in Equilibrium: Supply Shift Price $50 Market supply 40 E3 30 E1 20 10 0 Initial demand 25 50 75 100 Quantity 3-48 Market Outcomes • The market mechanism resolves the basic economic questions: – WHAT we produce is determined by equilibriums – HOW we produce is determined by profit seeking behavior and efficient use of resources – FOR WHOM we produce is determined by those willing and able to pay equilibrium prices 3-49 Optimal, Not Perfect • Although outcomes of the marketplace are not perfect, they are often optimal – the best possible given our incomes and scarce resources 3-50 Supply and Demand End of Chapter 3 McGraw-Hill/Irwin Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved.