Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

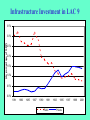

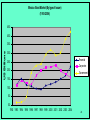

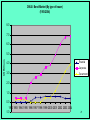

World Economic Forum What is Needed to Advance Infrastructure Needed Steps to Advance Infrastructure Finance in Latin American and the Caribbean (LAC) Diagnosis and Challenges of Economic Infrastructure in Lac Pietro Masci Inter-American Development Bank New York, June 22, 2005 1 Contents • • • • • • • • Infrastructure and Growth Private Sector and Growth Reforms and public discontent Recurrent dissatisfaction, diminished expectations LAC falls behind Investment needs Can reforms be made sustainable? Challenges for governments and IFIs 2 Infrastructure and Economic Growth • Good infrastructure promotes economic growth (as opposed to White Elephants) • Private sector is the engine of growth 3 What Happened? Public retrenchment never fully offset by private entry 5% TOTAL Public Private 4% share of GDP 4% 3% 3% 2% 2% 1% 1% 0% 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 4 Source: Calderon and Serven (2004) Infrastructure Investment in LAC 9 3.5% (As percentage of GDP) 3.0% 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% 1981 1983 1985 1987 1989 1991 Public 1993 1995 Private 1997 1999 2001 5 The State of the Opinion •Infrastructure reforms and privatizations do not go well with the Latin American opinion. •According to Latinobarometro, a high and growing % of L.A. people disagree that privatization was beneficial for their country: As of 2003, in the 17 countries surveyed, negative views of privatizations ranged from 53% in Honduras to 83% in Argentina, for Latin American average above 67% 6 The State of the Opinion: A Privatization Paradox? • Strong public discontent contrasts with rather favourable evaluations of the privatization process in terms of operating efficiency / profitability / output / investment / service coverage / fiscal results / some social indicators (e.g., child mortality) / poverty / income distribution. • Discontent occurs even in countries where unequivocal welfare gains (more access, lower prices, improved quality) have materialized • This parallels a generic discontent with reforms / free markets / democracy, etc. (La Porta & Lopéz-de-Silanes 99, Megginson & Netter 2001, McKenzie & Mookherjee 2003, Chong & Lopéz-de-Silanes 2004, Galiani et al. 2005). 7 Percentage of respondents who (strongly) disagree that privatization has been beneficial for their country Argentina Panama Bolivia El Salvador Peru Uruguay Paraguay Ecuador 2003 Nicaragua 1998 L.A. Guatemala Mexico Venezuela Colombia Chile Brazil Honduras 0 20 40 60 80 100 8 Why is this Happening? • What are some of the causes del rechazo social? Various studies point to different factors: – Unequal income distribution, Graham (2005) – Perception that benefits accrue always to the same people, Boix (2005) – Perception of Corruption, Martimort y Straub (2005) – Political and economic shocks, property rights, beliefs, Di Tella (2005) – Lack of deepening of reforms, Kucinsky and Williamson (2003) – Privatization, deregulation and capital market development 9 Recurrent dissatisfaction, diminished expectations • Distrust in governments makes privatization look as “the same recipe once again” if things go wrong • Distrust leads to expect that current gains will be expropriated or will reinforce the status quo • Recalcitrant expectations form when property rights can only be defended by those who have the means and skills • Advance in economic progress, property rights enforcement and inequality reduction needed to develop trust 10 LAC is falling behind Various measures of gaps between LAC and other areas (e.g., Asia) Caveat: geography and GDP composition (Singapore figures cannot be compared with Brazil’s) 11 LAC has fallen behind China and Middle Income Countries 2500 LAC 2000 MIC China 1500 1000 500 0 Access to electricity (%) Source: World Development Indicators Roads (km/km2) Mainline per 1000 pers 12 Latin American firms see infrastructure as a bottleneck Businesses that see infrastructure as a serious problem for the growth of their business: LAC Middle East & North Africa Sub-Saharan Africa South Asia Europe & Central Asia East Asia & Pacific 0 10 20 30 40 50 60 Percent of firms Source: World Bank Investment Climate Surveys 13 Investments Needs • Various estimations of investment needs for infrastructure in the years ahead 14 How much is needed depends on the goal • Universal coverage of water and sanitation? • ~ 0.25% over 10 years • To maintain and rehabilitate existing assets? • ~1% of GDP for adequate maintenance • Impossible to estimate rehabilitation needs • For business as usual? • ~ 2% of GDP to satisfy consumer and firm demand based on modest growth assumptions • To grow and take off? • ~4 to 6% of GDP to catch up with Korea and keep up with China 15 Brasil: Expected Investments by Sector Investimentos Totais (2000-2007) US$ 164,9 bilhões Meio Ambiente Informação & Conhecimento US$ 12,4 bilhões Transportes US$ 29,3 bilhões US$ 1,6 bilhão Energia US$ 28,5 bilhões Desenvolvimento Social US$ 52,5 bilhões Telecomunicações US$ 40,6 bilhões 16 Where is the Funding Coming from? • Foreign Borrowing • Domestic Markets 17 Investments • A growing attention to Project Finance occurs when international financial markets become unavailable. Role of Domestic markets and Public sector banks/Funds • Legal and regulatory environment are not enough to mitigate risks 18 Example of Project Finance Sponsors and Investors Government Regulation Constructors Financial Institutions Trustee $$$ Special Purpose Company Suppliers Operators Cash Flow / Services 19 Example of PPP Government Regulation Sponsors and Investors Constructors Loans DB, BID, and other SPE Suppliers Operators Fiduciary Agent Cash Flow Liquidity Fund Treasury/ Fiscal Fund Achievement of Contractual Goals 20 Domestic Capital Market Development Trade off: Capital market – Public sector financing 21 Latin America: BOND MARKET (By type of issuer) 250 150 Financial Government 100 Corporate 50 0 19 93 19 94 19 95 19 96 19 97 19 98 19 99 20 00 20 01 20 02 20 03 20 04 US Billions 200 22 BRAZIL: Bond Market (By type of issuer) (1993-2004) 50.0 45.0 40.0 US Billions 35.0 30.0 25.0 20.0 Financial Corporate Government 15.0 10.0 5.0 0.0 -5.01992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 23 Mexico: Bond Market (By type of issuer) (1993-2004) 45.0 40.0 US Billions 35.0 30.0 25.0 Financial Corporate 20.0 Government 15.0 10.0 5.0 0.0 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 24 CHILE: Bond Market (By type of issuer) (1993-2004) 8.0 7.0 6.0 US Billions 5.0 4.0 Financial Corporate 3.0 Government 2.0 1.0 0.0 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 -1.0 25 Putting all together…… 26 LATIN AMERICA: Bond Market, Stock Market Capitalization and Credit to Private Sector 1991-2004 700.0 600.0 Bond Market 400.0 Stock Market 300.0 Credit to Private Sector 200.0 100.0 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 0.0 1991 US Billions 500.0 27 Reasons to Develop Capital Markets • To satisfy -supposedly efficiently- the financial need of Government • To allocate resources efficiently The key to success is to find and maintain the right mix between these two functions that may create opportunistic actions, and conflict of interests 28 Development of Capital Markets As the economy grows -particularly in relatively large countries- and the possibilities of external financing are limited, corporations need long term financing possibly through capital markets. 29 Alternative to Capital Market Development • Creation of Development Banks (DBs) to provide long term financing not otherwise available • Historically, this is the experience in Europe and also in LAC countries • However, economic efficiency was not the objective of these institutions (e.g., political theory of development banks) and mismanagement and corruption were the rule rather than the exception and financing the economy took a back seat 30 Competing or Complementary Courses of Actions? State Model • Long term financing provided by DB and external sources Market Model •Long term financing provided by capital markets 31 Other additions to the toolkit • Infrastructure funds and unbundling of building and financing in project finance • Mezzanine structures and equity kickers • Better use of guarantees 32 Other additions to the toolkit • Financial structures adapted to local context • Governance measures to level the playing field between contractors and governments • Governance measure to proactively manage risk and avoid project collapse 33 Financial structures for economically sound transportation projects Case 1: HIGH fiscal space credibility (+) Private profitability (-) - PPPA: profit-sharing - PPPD: concession with public guarantees - Pure concessions - Civil works - Single-payment outsourcing contracts Low - PPPE: classic PPP with recurrent public payments High Contract enforcement by courts 34 Financial structures for economically sound transportation projects Case 2: LOW fiscal space credibility (+) Private profitability (-) - PPPA: profit-sharing - PPPA: profit-sharing - Single-payment outsourcing contracts - PPPB: public/community procurement (matching); evaluate tax earmarking Low - PPPC: concession revenue supplemented by land use rights High Contract enforcement by courts 35 Can reforms become sustainable? • A long-term, evolutionary, incremental approach to reach infrastructure reform sustainability • Effort inside the sector to increase reform quality and public support must not diminish • However, a purely sector approach does not suffice, given distrust in government and the pervasiveness of inefficient redistribution • Coordinate sector measures with advances in (i) redistributive and fiscal policy; (ii) rule of law; (iii) capital market development 36 Can reforms be made sustainable? Redistributive policy and fiscal space Growth Sector Reform and Investments Rule of Law Capital Market Development 37 Where are We? • The need of infrastructure financing is clear • The commitment of Government bond development is strong • However, will the government find and keep the right mix between the public sector and private sector financing? Or it might be tempted to give preference to the first one? • In LAC we see that in large part Governments are committed to fiscal discipline and are attempting to move towards the optimal mix. However, this is valid for large countries (e.g., Mexico, Brazil). • Small countries? Will we have a two speed LAC? This is a big challenge 38 Looking Forward • Reforms take time and perseverance even if you have “big bangs” • Government: Enabling environment + Leadership + Continuity + Doing the right things and attack the roots – Institutional, Political, Administrative and Judicial stability – Stop the pendulum between public and private sector in financial markets • Growth and competitiveness are complementary and instrumental to reach better standards of living 39 Challenges for Governments and IFIs • How to combine political leadership and empowerment to start change in expectations • How to ensure permanence of results to consolidate expectations • Tactical advice for sector reform meanwhile: press for measures that self-reinforce in the right direction; avoid overwhelming institutions with duties beyond their capabilities 40 IDB in Latin American and Caribbean Markets Five Pillars of the IDB’s approach to infrastructure and capital market development 1. 2. 3. 4. 5. Institutional support through capital market development initiatives and infrastructure financing Government Debt management and bond issues as a building block of capital market development Contributing to the development of local currency financing as issuer (e.g., Finance Department) and as lender for domestic capital markets development (e.g., PRI); Local currency financing to the public sector; Efficiency of State owned banks 41 Key Messages • LAC needs to spend more on infrastructure • LAC needs to spend better • Governments remain at the heart of the infrastructure challenge • The private sector can contribute, but only if the region builds on the lessons of the last decade • Investments in infrastructure have to be regarded in an holistic fashion 42