Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

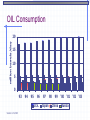

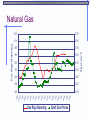

NASPD June 12, 2004 Jim Cowan Maverick EVP/COO Maverick Overview Market capitalization $1.0 billion Sales Revenue $1.3 billion Headquarters St. Louis, MO Company founded 1977 Employees 2,500 Largest oil country tubular goods (OCTG) producer and one of the largest conduit producers in North America 1.7 million tons of tubular products capacity Largest buyer of hot rolled steel in North America Geographically diverse production facilities 24 mills in 10 North American locations Maverick’s operations are segmented into energy and industrial products * Based on closing stock price on April 16, 2004 2 Summary of Products Energy Products 67% of 1Q2004 Revenues 65% of 1Q2004 EBITDA Industrial Products 33% of 1Q2004 Revenues OCTG Used in completions of newly drilled wells Line pipe Used to gather, transmit and disperse oil and natural gas Coiled tubing Used in well servicing, flowline and umbilical applications HSS Structural tubing used in construction and other applications Conduit Sheathing for wiring in non-residential construction 35% of 1Q2004 EBITDA 3 Maverick Locations Calgary Ferndale Conduit Elyria Conduit Hickman 4 facilities First Quarter 2004 Counce Conroe REVENUES Cedar Springs Conduit Industrial Houston 33% Energy 67% 3 facilities Coiled Tubing Coupling Manufacturer 4 CHINA Riding the Dragon’s Tail CHINA is a major player Bright spot of the global economy GDP grew more than 9% in 2003 Averaging 9.7% in past 24 years World’s largest recipient of foreign direct investment $53.7 billion in 2002 World’s 2nd largest economy measured by purchasing power Second largest foreign currency reserves $400 billion by end of 2003 World’s 4th largest trading nation over $700 billion in 2003 Full integration of China into WTO provides further stimulus to internationalize industry and markets. 6 CHINA GDP Growth 15 percent GDP 13 12 10 10 10 9 9 8 7 8 7 9 8 5 0 93 94 95 96 97 98 99 '00 '01 '02 '03 '04 Actual Source: U.S. Commerce Forecast CHINA growth everywhere China’s economy is between 8-10 times the size that it was at the beginning of reform in 1978. Domestic demand as growth engine – exports are less than 30% of overall production. Less than 50% of GDP now state-controlled and only an extremely small number of goods are price controlled. Dramatic expansion in the private sector – aggressive entrepreneurialism has produced 2.5 million firms, providing bulk of employment, tax and overall national growth. China’s growth has been powered by latent demand, the entrepreneurial energy unleashed by the country’s unprecedented reforms, and inherent inefficiencies Emerging large and consuming middle class - growing fast +300 million with significant discretionary spending power by 2010 8 CHINA a hungry dragon China has become the world’s largest consumer of copper, consuming 22,000 tons and importing more than 7,000 tons every day China has become the world’s largest producer of steel, outpacing both Japan and the USA, importing 408,000 tons of iron ore every day China is now importing 1,750,000 barrels of oil every day signing up LNG deals with Australia, Indonesia, and Iran pipelines being built from Kazakhstan and planned from Siberia 9 CHINA capital flow continues China is attracting external capital as the global epicenter for manufacturing, largely because of its’ low labor costs. Investment exceeds $50 billion US annually Investments in processing, assembly, redistribution and value added businesses in China continue to increase relative to Southeast Asia, India and Latin America. Foreign and Chinese manufacturers are building out global supply channels from China. Chinese consumers and raw material users are influencing global pricing in many industries. 10 CHINA Export and Import Growth U.S. Billion $ 500 400 300 200 100 0 93 94 95 96 97 98 Export Source: U.S. Commerce 99 '00 '01 '02 '03 Import OIL Consumption million barrels/day 20 15 10 5 0 93 94 95 96 U.S. Source: U.S. EIA 97 Japan 98 99 China '00 '01 '02 '03 Russia CHINA Oil Consumption million barrels/day 6 4 2 0 93 94 95 96 97 Japan Source: U.S. EIA 98 China 99 '00 Russia '01 '02 '03 China Steel Consumption 400 million tonnes 374 300 200 100 205 135 232 256 276 167 0 '00 '01 '02 Actual Source: Steel Dynamics '03 '04 Forecast '05 '10 China vs USA Steel Consumption million tonnes 400 300 200 100 0 '00 '01 '02 China A Source: Steel Dynamics '03 China F '04 '10 '05 USA A USA F STEEL COSTS Steel costs have risen sharply Rise in the cost of scrap metal, coke, pig iron & other raw materials are pushing steel costs higher Base price has risen $180 to $240 per ton since the first of the year Base prices are set to rise Unprecedented steel surcharges $125 per ton April 2004 Anticipate steel cost to be volatile throughout 2004 16 95 Q3 -9 Q1 5 -9 Q3 6 -9 6 Q1 -9 Q3 7 -9 7 Q1 -9 Q3 8 -9 Q1 8 -9 9 Q3 -9 Q1 9 -0 Q3 0 -0 0 Q1 -0 Q3 1 -0 1 Q1 -0 Q3 2 -0 Q1 2 -0 3 Q3 -0 Q1 3 -0 4 Q1 - Global operating rate 100 95 Source: Steel Dynamics 450 400 90 350 300 85 250 200 80 150 Global operating rate $ / metric tonne $ per metric tonne Steel 550 500 J0 0 A0 0 J0 0 O0 0 J0 1 A0 1 J0 1 O0 1 J0 2 A0 2 J0 2 O0 2 J0 3 A0 3 J0 3 O0 3 J0 4 A0 4 J0 4 O0 4 Oil Rigs Running 300 $40.00 250 $35.00 200 $30.00 150 $25.00 100 $20.00 50 $15.00 Oil Rigs Running Spot Oil Prices $ per barrel Oil $9.50 1100 $8.50 1000 $7.50 900 $6.50 800 $5.50 700 $4.50 600 $3.50 500 $2.50 400 $1.50 Gas Rigs Running Spot Gas Prices $ per mcf 1200 J0 0 A0 0 J0 0 O0 0 J0 1 A0 1 J0 1 O0 1 J0 2 A0 2 J0 2 O0 2 J0 3 A0 3 J0 3 O0 3 J0 4 A0 4 J0 4 O0 4 Gas Rigs Running Natural Gas SUMMARY Tight steel supplies and higher prices will be prevalent for the foreseeable future Anticipate drilling activity to increase 7% for 2004 in U.S., 5% in Canada Energy prices will stabilize but remain elevated The 21st century is the “Chinese” century Figure out how this impacts your business! 20