Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Fei–Ranis model of economic growth wikipedia , lookup

Global financial system wikipedia , lookup

Fear of floating wikipedia , lookup

Production for use wikipedia , lookup

Steady-state economy wikipedia , lookup

Ragnar Nurkse's balanced growth theory wikipedia , lookup

Long Depression wikipedia , lookup

Uneven and combined development wikipedia , lookup

Okishio's theorem wikipedia , lookup

Chapter 17

Macroeconomic Policies

and Long-Term Growth

© Pierre-Richard Agénor and Peter J. Montiel

1

Wide dispersion of output growth rates across countries.

Table 17.1: growth performance of developing

countries.

Traditional neoclassical approaches: incapable of

explaining the wide disparities in the pace of economic

growth across countries.

“New growth” literature: existence of “endogenous”

mechanisms that foster economic growth, and new

roles for public policy.

2

The Neoclassical Growth Model.

Externalities and Increasing Returns.

Human Capital, Knowledge, and Growth.

Effects on Financial Intermediation.

Inflation Stabilization and Growth.

Government size and Growth.

Commercial Openness and Growth.

Exchange-Rate Unification and Growth.

3

The Neoclassical Growth

Model

Solow (1956) and Swan (1956): neoclassical growth

model.

Assumptions:

Production function: aggregate, constant-returns-toscale, and combines labor and capital in the

production of composite good.

Savings: fixed fraction of output.

Technology improves at exogenous rate.

Cobb-Douglas production function:

Y = AKL1-,

0 < < 1,

(1)

Y: total output; K: capital stock; A: level of technology;

L: workers employed in the production process.

5

Output per worker, y = Y/L, is given by

y = Ak,

k: capital-labor ratio.

Capital accumulation is given by

.

k = sy - (n + )k,

0 < s, < 1,

(2)

s: propensity to save;

n > 0: exogenous rate of population growth;

: rate of depreciation of physical capital.

(2) incorporates equilibrium condition of goods market

or, equivalently, equality between investment I and

6

saving, I = sy.

Suppose that A is constant over time.

Substituting (1) in (2) and dividing both sides of the

resulting expression by k yields growth rate of capitallabor stock:

.

gk k/k = sAk-1 - (n + ),

(3)

from which the rate of growth of output per worker can

be derived as

.

.

gy y/y = kAk-1/Ak = gk.

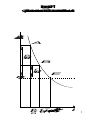

Figure 17.1: behavior of capital stock per worker.

Horizontal line at n + : depreciation line.

7

F

i

g

u

r

e

1

7

.

1

C

a

p

i

t

a

l

A

c

c

u

m

u

l

a

t

i

o

n

i

n

T

h

e

S

o

l

o

w

S

w

a

n

G

r

o

w

t

h

M

o

d

e

l

s

A

k

A

p

g

k

B

r

g

k

E

n

+

~

1

/

(

1

r

p

k

k

k

=

(

s

A

/

n

+

0

0

k

8

Curve sAk-1: savings curve.

Savings curve is downward-sloping due to assumption

of decreasing marginal returns to capital.

As implied by (3), gk is the difference between the two

curves.

Point of intersection of the two curves: steady-state

value of k.

If technology grows at a constant rate, steady-state

values of output per effective worker and

capital/effective labor ratio are

constant;

proportional to the rate of technological change.

Although s has no effect on growth rate per capita in the

long run, it affects level of per capita income in steady

9

state.

Model implies that countries with similar production

technologies, and comparable saving and population

growth rates should converge to similar steady-state

levels of per capita income.

Figure 17.1: “poor” country starts with capital stock of k0p

has higher initial growth rate than “rich” country starting

with k0r .

Poor country grows faster during the transition.

But, if both countries possess the same level of A, s, ,

n, they will both converge to the same steady-state level

~

of the capital stock, k.

Convergence occurs because each increment to capital

stock generates large additions to output when capital

stock is initially small with diminishing marginal returns

to capital.

10

“Sources-of-growth” approach: empirical methodology

to analyze determinants of changes in output.

It uses aggregate production function to decompose

growth into “contributions” from different sources plus

residual.

Residual: “technical progress,” or more adequately

growth in total factor productivity.

Assume: production function is y = Af(k, n).

11

In terms of percentage changes:

.

.

.

.

g y/y = (A/A) + Afk(k/y) + Afn(n/y)

. A + kgk + ngn,

=g

h = fhh/y (for h = k, n): elasticity of output with respect

to input h;

gA: rate of growth of total factor productivity and is

derived as a residual.

Under conditions of competitive equilibrium, factors are

paid their marginal products: k (n) is equal to share of

capital (labor) income in total output.

In the presence of constant returns to scale, sum of all

12

share coefficients must be equal to unity.

With Cobb-Douglas production technology as in (1),

assuming that factors of production are paid their

marginal products implies that

k = 1-n, and

labor's share corresponds to the parameter .

Even though hypotheses of constant-returns-to-scale

production function and competitive factor markets are

restrictive, there are studies based on the model.

Chenery (1986):

Studies based on sources-of-growth methodology in

the 1960s and 1970s.

Average capital share is about 40%, which indicates

that production function exhibits diminishing marginal

returns to capital.

13

Growth in capital stock had limited effect on output

growth.

Average contribution of the residual was less than in

developed countries.

Most countries had high growth rate of labor input.

Estimates of capital share vary across countries,

ranging from 26% for Honduras to more than 60% for

Singapore.

Effect of capital accumulation on growth varies across

countries.

Contribution of total factor productivity to growth also

varied across countries.

Elías (1992):

Growth process of Argentina, Brazil, Chile, Colombia,

14

Mexico, Peru, and Venezuela during 1940-85.

He considers different kinds of labor and capital inputs,

and defines gross and quality component for each of

them.

For labor: gross component is arithmetic sum of

employment across characteristics.

For capital: it is arithmetic sum of different categories of

capital.

Quality component captures changes in composition of

factors of production.

Output growth averaged 5.3% for the group as a whole.

Quality of labor rose on average by 1.4%, and quantity

of labor by 2%.

Quality of capital fell by 0.4%, its quantity grew at 4%.

Given average labor share of 40%, labor contributed

15

1.3% to average growth rate.

Capital's contribution was 2.5%.

Technological progress was therefore 1.5% of rate of

growth.

Thus, capital made the highest contribution to output

growth (47%) because of its quantity and its share.

Quality of labor played more important role in growth of

labor input.

Table 17.2:

Decomposition of trend or potential output growth for

developing countries during the 1970s and 1980s.

Contribution of capital to potential output growth was the

most important.

Total factor productivity accounted for about the same

share as labor in its contribution to growth.

16

Differences across regions: total factor productivity

accounts for negligible share of growth in Africa and

the Middle East,

provides substantial contribution to growth in Asia.

Limitations of neoclassical growth model:

Capital assumed to exhibit diminishing marginal returns.

This prevents it from providing an explanation

for the wide variations across countries in either per

capita income or growth rates, and

for the fact that poor countries do not grow faster

than rich ones (Figure 17.2).

It is assumed that output growth is independent of

saving rate and is determined only by demographic

factors and technological progress rate.

17

F

i

g

u

r

e

1

7

.

2

A

v

e

r

a

g

e

R

a

t

e

o

f

G

r

o

w

t

h

P

e

r

C

a

p

i

t

a

a

n

d

P

r

o

p

o

r

t

i

o

n

o

f

G

N

P

P

e

r

C

a

p

i

t

a

t

o

U

S

G

N

P

P

e

r

C

a

p

i

t

a

0

.

1

0

.

0

5

0

AveragtofGNPgrwthpecai(197-5)

0

.

0

5

0

.

1

0

0

.

0

5

0

.

1

0

.

1

5

0

.

2

0

.

2

5

0

.

3

G

N

P

p

e

r

c

a

p

i

t

a

r

e

l

a

t

i

v

e

t

o

U

S

G

N

P

p

e

r

c

a

p

i

t

a

I

n

1

9

7

0

(

i

n

U

.

S

.

d

o

l

l

a

r

s

)

S

o

u

r

c

e

:

W

o

r

l

d

B

a

n

k

.

18

Since population growth and technological change are

assumed exogenous, the model does

not explain the mechanisms that generate steadystate growth,

not allow evaluation of mechanisms through which

government policies can influence growth process.

Assumption that rate of growth of output is independent

of saving rate is at variance with the evidence; highgrowth developing countries have higher saving rates.

New growth literature addresses these limitations by

proposing variety of channels through which steadystate growth arises endogenously.

19

Externalities and Increasing

Returns

Two approaches were followed to relax assumption of

diminishing returns to capital:

First approach views all production inputs as some

form of reproducible capital, including

physical capital,

human capital (Lucas, 1988) or

“state of knowledge” (Romer, 1986).

Simple growth model along these lines: AK model

proposed by Rebelo (1991).

It results from setting = 0 in (1):

y = Ak,

where k = K/L as before, but K includes both physical

21

and human capital.

Thus, production function is linear and exhibits constant

returns to scale, but does not yield diminishing returns

to capital.

Using the capital accumulation (2), steady-state growth

rate of capital stock per worker:

gk = sA - (n + ).

Steady-state growth rate per capita:

gy = sA - (n + ).

Growth rate is, for sA > n+, positive (and constant over

time) and level of income per capita rises without

bound.

22

Implication of AK model:

Increase in saving rate raises growth rate per capita.

Poor nations whose production process has the

same technological sophistication as other nations

grow at the same rate as rich countries, regardless of

initial level of income.

Thus it does not predict convergence even if

countries

share the same technology;

are characterized by the same pattern of saving.

Rebelo (1991):

Implications of considering separately the production

of consumption goods, physical capital, and human

capital goods.

23

Endogenous steady-state growth obtains if “core” of

capital goods is produced

according to a constant-returns-to-scale

technology;

without nonreproducible factors.

Second approach: introducing spillover effects or

externalities in growth process.

Externalities: if one firm doubles its inputs, productivity

of inputs of other firms will also increase.

Introducing spillover effects relaxes assumption of

diminishing returns to capital.

Mostly externalities take the form of general

technological knowledge that is available to all firms,

which use it to develop new methods of production.

24

Exceptions.

Lucas (1988): externalities take the form of public

learning, which increases the stock of human capital

and affects productivity of all factors.

Barro (1990): externalities associated with public

investment.

Externalities is associated with increasing returns to

scale in production function.

But, important implication of models exhibiting spillover

effects and externalities is that sustained growth

does not result from the existence of external effects,

rather result from assumption of constant returns to

scale in all production inputs.

Rebelo (1991): increasing returns are neither necessary

25

nor sufficient to generate endogenous growth.

Human Capital, Knowledge,

and Growth

The Production of Human Capital.

The Production of Knowledge.

27

The Production of Human Capital

One of the sources of externalities: accumulation of

human capital and its effect on productivity of the

economy.

Lucas (1988):

Spillover effects of human capital accumulation.

Individual workers are more productive, if other

workers have more human capital.

Simplified version of Lucas' model is examined here.

Human capital is accumulated through explicit

“production”: part of individuals' working time devoted to

accumulation of skills.

Let k denote physical capital per worker and h human

28

capital per worker (“knowledge” capital).

Production process:

y = Ak[uh]1-, 0 < u < 1,

u: fraction of time that individuals devote to producing

goods.

Growth of physical capital depends on saving rate.

Growth rate of human capital depends on time devoted

to its production:

.

h/h = (1-u),

> 0.

Long-run growth rate of both capital and output per

worker is (1-u).

29

Rate of human capital growth, and ratio of physical to

human capital converges to a constant.

In the long run, income is proportional to the economy's

initial stock of human capital.

Saving rate has no effect on growth rate.

Implication of the model:

Under purely competitive equilibrium there will be

underinvestment in human capital since private agents

do not take into account external benefits of human

capital accumulation.

Equilibrium growth rate is thus smaller than optimal

growth rate.

Growth would be higher with more investment in human

capital.

30

Thus government policies are necessary to increase the

equilibrium growth rate.

31

The Production of Knowledge

Romer (1986): source of externality is stock of

knowledge.

Knowledge is produced by individuals.

But since newly produced knowledge can be partially

and temporarily kept secret, production of goods and

services depends on both

private knowledge, and

aggregate stock of knowledge.

Since individuals only partially reap rewards to

production of knowledge, market equilibrium results in

underinvestment in knowledge accumulation.

32

Romer (1990):

Explains endogenously decision to invest in

technological change;

uses a model based on distinction between research

sector and rest of the economy;

firms cannot appropriate all the benefits of knowledge

production;

tax and subsidy can be used to raise rate of growth.

Simplified version of Romer's (1990) model is presented

here.

Two production sectors:

goods-producing sector uses physical capital,

knowledge and labor in the production process;

knowledge-producing sector (same inputs are used).

33

cL (cK): fraction of labor force (capital) is used in the

knowledge-producing sector.

1–cL (1-cK): fraction of labor (capital) in the goodsproducing sector.

A: total stock of knowledge that can be used in both

production activities.

Assuming Cobb-Douglas technology, output in goodsproducing sector:

Y = [(1-cK)K][A(1-cL)L]1-

0 < <1. (9)

Constant returns to both capital and labor.

34

Production of new knowledge (changes in A) is

determined by generalized Cobb-Douglas form:

.

A = B(cKK)(cLL)A,

B > 0, 0, , 0,

(10)

B: shift parameter.

There is either diminishing returns in production of new

ideas or increasing returns, depending on , , and .

can be equal to unity, or strictly greater or smaller than

unity.

Assuming s is constant and there is no depreciation of

capital stock, then

.

K = sY,

0 < s < 1.

(11)

35

Population growth is exogenous:

.

L = nL,

Begin analyzing te model by substituting (9) in (11):

.

K = KKA1-L1-,

n 0.

K s(1-cK)(1-cL)1-.

Dividing both sides of this expression by K:

.

gK (K/K) = K{AL/K}1-.

Its rate of change:

.

gK = (1-)(gA + n - gK).

(14)

36

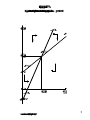

gK is rising (falling) if gA+n-gK is positive (negative), and

remains constant if gA+n = gK.

Curve KK in Figure 17.3: combinations of gA and gK for

which gK is constant over time.

Slope of KK is unity; above (below) KK, gK is falling

(rising).

Dividing both sides of (10) by A:

.

gA A/A = AKLA-1,

A BcKcL.

This implies that

.

gA = gK + n + (-1)gA.

(15)

37

F

i

g

u

r

e

1

7

.

3

D

y

n

a

m

i

c

s

o

f

C

a

p

i

t

a

l

a

n

d

K

n

o

w

l

e

d

g

e

:

C

a

s

e

I

-

+

<

1

g

K

A

K

~

E

g

K

K

n

0

A

~

g

A

g

A

n

/

S

o

u

r

c

e

:

R

o

m

e

r

(

1

9

9

4

,

p

.

1

0

7

)

.

38

gA is increasing (falling) if right-hand side of (15) is

positive (negative), and constant if it is zero.

Curve AA in Figure 17.3: combinations of gA and gK for

which gA is constant over time.

Slope of AA is (1-)/, which is ambiguous in sign.

Figure assumes that < 1, so that the slope is positive.

Above (below) AA, gA is rising (falling).

(9) exhibits constant returns to scale in K and A.

Thus whether there are on net increasing, decreasing,

or constant returns to scale to A and K depends on

whether (10) exhibits constant returns to scale.

This equation can be rewritten as

.

A = KA(qL),

q BcKcL.

39

Degree of returns to scale to A and K in production of

new knowledge is + .

Consider the three separate cases, depending on

whether + is less, equal, or greater than unity.

If + < 1:

(1-)/ is greater than unity and AA is steeper than KK.

This case is illustrated in Figure 17.3.

Regardless of initial values of gA and gK, they converge

to equilibrium point E.

.

~

~

Equilibrium values gA and gK are obtained by setting gA

.

= gK = 0 in (14) and (15), and are given by

+

gA =

n,

1 – (+)

~

~

~

gK = n + gA.

40

From (9), aggregate output and output per worker are

growing at rates given by

gY = gK + (1-)(n + gA) = gK,

~

~

~

~

~

~

gY/L = gK – n = g~ A.

Thus, economy's growth rate is endogenous: increasing

function of n and is zero if n is zero.

cL,cK and s have no effect on growth rate.

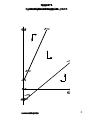

If + > 1:

AA and KK diverge (Figure 17.4).

Regardless of economy's initial position, it enters the

region between two curves.

41

F

i

g

u

r

e

1

7

.

4

D

y

n

a

m

i

c

s

o

f

C

a

p

i

t

a

l

a

n

d

K

n

o

w

l

e

d

g

e

:

C

a

s

e

I

I

+

>

1

g

K

K

A

K

n

0

A

g

A

n

/

S

o

u

r

c

e

:

R

o

m

e

r

(

1

9

9

4

,

p

.

1

0

8

)

.

42

Once this occurs, growth rates of A and K increase

without bound.

There cannot be steady-state growth.

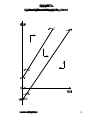

If + = 1:

(1-)/ is equal to unity and AA and KK have the same

slope.

If n is positive, KK lies above AA:

upper panel of Figure 17.5;

there is no steady-state level of growth.

If n = 0, AA and KK are identical:

lower panel of Figure 17.5;

regardless of initial position of the economy,

balanced growth path is reached;

this path is unique;

43

F

i

g

u

r

e

1

7

.

5

a

D

y

n

a

m

i

c

s

o

f

C

a

p

i

t

a

l

a

n

d

K

n

o

w

l

e

d

g

e

:

C

a

s

e

I

I

+

=

1

g

K

K

A

K

n

0

A

g

A

n

/

S

o

u

r

c

e

:

R

o

m

e

r

(

1

9

9

4

,

p

.

1

0

9

)

.

44

F

i

g

u

r

e

1

7

.

5

b

D

y

n

a

m

i

c

s

o

f

C

a

p

i

t

a

l

a

n

d

K

n

o

w

l

e

d

g

e

:

C

a

s

e

I

I

+

=

1

g

K

A

A

a

n

d

K

K

g

A

S

o

u

r

c

e

:

R

o

m

e

r

(

1

9

9

4

,

p

.

1

0

9

)

.

45

economy's growth rate on that path depends on all

the parameters of the model including s.

Existence of knowledge-producing sector may explain

positive correlation between s and rate of economic

growth (Figure 17.6).

46

F

i

g

u

r

e

1

7

.

6

S

a

v

i

n

g

R

a

t

i

o

a

n

d

O

u

t

p

u

t

G

r

o

w

t

h

P

e

r

C

a

p

i

t

a

(

1

9

7

1

9

5

)

0

.

1

0

.

0

8

0

.

0

6

0

.

0

4

0

.

0

2

AveragtofGNPgrwthpecai

0

0

.

0

2

0

.

0

4

0

.

0

6

1

0

0

1

0

2

0

3

0

4

0

5

0

6

0

G

r

o

s

s

D

o

m

e

s

t

i

c

S

a

v

i

n

g

a

s

a

p

r

o

p

o

r

t

i

o

n

o

f

G

D

P

S

o

u

r

c

e

:

W

o

r

l

d

B

a

n

k

.

47

Effects of Financial

Intermediation

Introduce financial factor, following Pagano (1993), to

assume that 1- of saving is “lost” as a result of financial

disintermediation activities:

sy = I,

0 < < 1.

Assuming that production technology is constant returns

to scale to capital, steady-state growth rate per capita:

g = sA - .

How financial development affects economic growth:

raise s;

raise A (marginal productivity of the capital stock);

49

increase in (“conduit” effect).

Effects on the Saving Rate.

Effects on the Accumulation of Capital.

The “Conduit” Effect, Financial Repression, and Growth.

Financial Development and Growth: Empirical

Evidence.

50

Effects on the Saving Rate

Early development literature: existence of positive effect

of financial development on s.

New growth literature: direction of this effect is not

consistent.

Jappelli and Pagano (1994):

development of financial markets offers households

possibility of diversifying their portfolios and

increases their borrowing options;

this affects proportion of agents subject to liquidity

constraints, which may affect s.

Financial development also

reduces overall level of interest rates;

51

modifies structure of interest rates by reducing

spread between rate paid by borrowers and that paid

to lenders.

In each case effect on s is ambiguous.

Ambiguous effect of financial intermediation on s may

be compounded when all partial effects associated with

financial development are taken into account.

Bencivenga and Smith (1991): direct effect of banking

activities may be reduction in s.

But, if positive effect of financial development on

productivity of capital and efficiency of investment is

taken into account, net effect on growth may be

positive.

52

Effects on the Allocation of

Capital

Figure 17.7: investment and output growth are

positively correlated in developing countries.

Role of financial intermediaries: facilitate efficient

allocation of resources to investment projects that

provide the highest marginal return to capital.

Financial intermediation increases average productivity

of capital A in two ways:

by collecting, processing, and evaluating relevant

information on alternative investment projects;

by inducing entrepreneurs, through their risk-sharing

function, to invest in riskier but more productive

53

technologies.

F

i

g

u

r

e

1

7

.

7

I

n

v

e

s

t

m

e

n

t

a

n

d

O

u

t

p

u

t

G

r

o

w

t

h

P

e

r

C

a

p

i

t

a

(

1

9

7

1

9

5

)

0

.

1

0

.

0

8

0

.

0

6

0

.

0

4

0

.

0

2

AveragtofGNPgrwthpecait

0

0

0

.

0

2

0

.

0

4

0

.

0

6

5

1

0

1

5

2

0

2

5

3

0

3

5

4

0

G

r

o

s

s

D

o

m

e

s

t

i

c

I

n

v

e

s

t

m

e

n

t

a

s

a

p

r

o

p

o

r

t

i

o

n

o

f

G

D

P

S

o

u

r

c

e

:

W

o

r

l

d

B

a

n

k

.

54

Greenwood and Jovanovich (1990):

Link between informational role of financial

intermediation and productivity growth.

Capital may be invested in safe, low-yield technology or

risky, high-yield one.

Return to risky technology is affected by

aggregate shock;

project-specific shock.

Financial intermediaries with their large portfolios can

identify the aggregate productivity shock; and

induce their customers to select technology that is

most appropriate for current shock.

55

Efficient allocation of resources channeled through

financial intermediaries raises productivity of capital and

thus growth rate of the economy.

Pagano (1993):

Another function of financial intermediation: it enables

entrepreneurs to pool risks.

“Insurance” function: financial intermediaries allow

investors to share uninsurable and diversifiable risk

from rates of return differences on alternative assets.

Risk sharing affects saving and investment decisions.

Liquidity:

In the absence of banks, households can guard against

idiosyncratic liquidity shocks by investing in productive

assets that can be liquidated.

56

Bencivenga and Smith (1991): banks increase

productivity of investment by

directing funds to illiquid, high-yield technology;

reducing investment waste due to premature

liquidation.

57

The “Conduit” Effect, Financial

Repression, and Growth

Financial intermediation operates as a tax in

transformation of saving into investment.

Financial intermediation thus has growth-deterring effect

because intermediaries appropriate share of private

saving.

Costs associated with financial intermediation represent

payments that are received by intermediaries in return

for their services.

In developing countries:

Such absorption of resources results from explicit

and implicit taxation and by excessive regulations.

58

This leads to higher costs and thus inefficient

intermediation activities.

If financial system reforms reduce cost and

inefficiencies associated with intermediation process,

growth rate will increase.

Role of financial repression in growth models:

In countries where collecting conventional taxes is

costly, governments choose to repress their financial

systems to increase revenue.

Roubini and Sala-i-Martin (1995): inflation is viewed as

proxy for financial repression.

Courakis (1984): constraints on bank portfolio choices

may reduce volume and productivity of investment by

reducing funds channeled to deposit-taking financial

59

intermediaries;

causing less efficient distribution of any given volume

of such funds.

60

Financial Development

and Growth: Empirical Evidence.

Recent research has explored empirical relationship

between financial “deepening” and economic growth.

King and Levine (1993a, 1993b):

Four alternative measures of financial depth:

ratio of liquid liabilities of financial system to GDP;

share of total credit allocated by banks;

share of total domestic credit received by private

sector;

ratio of credit to private enterprises to GDP.

Contributions of such indicators in explaining

61

long-term real GDP growth;

share of investment in GDP;

rate of growth of total factor productivity.

All of financial depth indicators are statistically

significant with large positive effects on variable being

explained.

This association did not reflect reverse causation from

growth to financial indicators.

Evidence linking financial depth to long-term economic

growth, both through

incrementation of resource accumulation, and

enhancement of productivity growth,

is strong in cross-country record.

62

Inflation Stabilization and

Growth

High rates of inflation can be expected to reduce

economic growth through variety of mechanisms which

can influence both

rate of capital accumulation;

rate of growth of total factor productivity.

Fischer (1993): government which tolerates high

inflation is one which has lost macroeconomic control,

and this deters domestic investment in physical capital.

Other arguments: high inflation

means unstable inflation and volatile relative prices;

reduce information content of price signals;

distort efficiency of resource allocation, affecting

growth of total factor productivity.

64

Simplified version of De Gregorio’s model (1993) is

presented here.

Assumptions:

Closed economy consists of households, firms, and

government.

Households hold no money but hold indexed bond

issued by government.

Capital is only input in production process, which

takes place under constant returns to scale.

Firms hold money because it reduces transactions

costs associated with purchases of new equipment.

Capital mobility is precluded, so that domestic

investment must equal domestic saving.

Inflation is exogenous.

65

Representative household maximizes present value of

utility stream

0

c1- -t

e dt,

1-

0 < <1,

(18)

subject to flow budget constraint

.

b = (1 - )(y + rb) – c - ,

(19)

1/: elasticity of intertemporal substitution;

b: real stock of government indexed bonds;

0 < < 1: income tax rate;

r: real rate of return on bonds; y: total factor income;

66

: net lump-sum taxes paid by households.

Maximization of (18) subject to (19) yields

.

c/c = [(1-)r - ].

Production exhibits constant returns to scale:

y = Ak.

Firms require money to purchase new capital goods.

Cost of investing I units is thus equal to I[1+(m/I)],

where m is firms' real money holdings.

< 0 and > 0: holding money reduces transactions

costs but entails diminishing returns.

67

Representative firm maximizes present discounted

value of its cash flow, net of opportunity cost of its

holdings of money balances.

This opportunity cost is equal to (r + )m, where is

inflation rate.

Thus firm maximizes:

0

m

.

Ak - 1 + ( ) I – (r+)m – m e-rtdt,

I

.

subject to k = I.

68

Solution yields

(23)

m

-(

) = r + m = (r + )I, = 1/ < 0,

I

.

(24)

q/q = r – (A/q),

m

m

m

q = 1 + (

)( ),

I

I

I

(25)

q: shadow price of capital.

(23): firm's demand for money.

Since cash flows are not subject to direct taxation,

opportunity cost of holding money is sum of before-tax

real interest rate plus inflation rate.

69

(24): shadow price of capital is equal to present

discounted value of marginal product of capital.

(25): q exceeds unity due to existence of transactions

costs incurred in buying new unit of capital.

Substituting (23) in (25) yields

q = 1 + [()] + (r + )() = q(r + ),

~ if is constant.

(26): q is constant (at q)

From (24, real interest rate is:

~

q > 0.

(26)

~

r = A/q.

70

Government budget constraint:

.

.

m + b = g - y - - m,

g: public expenditure, which is taken to be a constant

fraction of output.

.

Assume b = 0, and government adjusts lump-sum taxes

to maintain fiscal equilibrium.

Aggregate resource constraint of the economy:

y = c + 1 + ( m ) I + g.

I

71

Consumption, output, capital, and real money balances

grow at constant rate in the steady state:

g = [(1-)r - ].

~

(30)

Model has no transitional dynamics; that is, economy

grows continuously at rate given by (30).

This model generates an inverse relationship between

output growth and due to negative effect of inflation on

profitability of investment.

Higher raises “effective” price of capital goods,

which incorporates opportunity cost of holding money

to facilitate purchases of capital goods.

72

Increase in transactions costs raises shadow value of

installed capital, dampens investment, and reduces

growth rate.

Barro (1997):

Cross-country evidence on relationship between

inflation and growth.

Data set consists of 100 countries, with annual

observations on macroeconomic data during 1960-90.

Three periods: 1965-75, 1976-85, and 1986-90.

Other things equal, 10% increase in reduces long-run

growth by about 0.025% per year.

It is level of , rather than its variability, that affects

growth adversely.

Results are robust with respect to exclusion of few high73

inflation outliers.

Interesting aspect of Barro's work: introduction of some

novel instruments for inflation.

Barro uses prior colonial history: these are uncorrelated

with innovations in recent growth experience, but

correlated with long-term inflation performance.

Using these as instruments for leaves previous results

in place.

Transition from high to low may not be associated

with contemporaneous acceleration in economic

growth.

Favorable growth effects from disinflation materialize

with a lag, so that growth may slow during transition,

and perhaps for some time thereafter.

74

Bruno and Easterly (1998):

Evidence about growth effects of transition from high to

low .

Methodology:

compiling a sample of countries that had experienced

successful stabilization over 1961-92; and

comparing their growth rates relative to world

average before, during, and after, their inflationary

episodes.

Growth fell by an average of 2.8% during high-inflation

episode, but rose by an average of 3.8% during

successful stabilization.

This pattern was repeated for growth of total factor

productivity.

75

But investment ratio did not rise above world average.

Conclusion: growth accelerates during and just after

stabilization when initial level of inflation is high.

Inflation stabilization component of market-oriented

reform policies should be growth-enhancing.

76

Government Size

and Growth

Inflation stabilization implies the need for reduction of

fiscal deficits that can be reduced by decreasing

expenditures or increasing revenues.

Difference between two approaches: resulting size of

government sector.

Both level and composition of government expenditures

may matter for long-term growth:

Holding fiscal deficit constant, larger government

expenditures imply need for additional revenues.

But such revenues would be raised through

distortionary taxation.

This would reduce rate of growth through adverse

effects on efficiency of resource allocation.

Some government expenditure may be productive.

78

Expenditures on health and education may be

interpreted as investments in human capital.

Other expenditures may represent investment in

“social capital” in form of institutions that

safeguard property rights.

Barro (1991):

Examines coefficients of government spending

variables when other long-term growth determinants are

controlled for in the regression.

Government expenditures are disaggregated into

government investment;

government consumption excluding spending on

defense and education;

79

spending on defense and education separately;

spending on transfer payments.

Government consumption net of defense and education

and transfers may affect growth adversely through

distortionary effects of taxation.

Government investment and defense and education

spending add to productive resources and thus would

have ambiguous effects on growth.

Empirical results are mixed:

Government investment has positive and statistically

significant partial correlation with growth.

Government consumption net of defense and

education is negative and significant.

80

Neither education nor defense spending is related to

long-run growth.

Spending on transfers is positively related to growth,

but Barro interprets this as reverse causation.

Barro (1997) confirms negative effect of government

consumption on long-term growth.

However, interpretation of these results remains open to

question, due to potential for reverse causation.

To identify separate effect of government size on

economic growth appropriate instrument is required.

Such instruments have not been easy to find.

Thus, interpretation of negative partial correlation

between government consumption and growth remains

ambiguous.

81

Commercial Openness

and Growth

Under conditions of financial openness, increased

commercial openness may reduce risk premium that

external creditors require.

Under neoclassical assumptions, this may result in

larger steady-state capital stock and thus more rapid

accumulation-driven growth during transition.

Endogenous growth models: exporting and importing,

by increasing economy's exposure to new technologies,

facilitate their adoption;

thus increase rate of growth of productivity.

Implication: trade liberalization, which promotes

commercial openness, should induce

increase in the level of income;

increase in its rate of growth.

83

Dollar (1992):

Relevant definition of openness: one that combines

liberal trade regime with stable real exchange rate.

To measure outward orientation of trade regime, he

uses deviations of Summers-Heston price levels from

values predicted from regression of price levels on

per capita GDP, and

measure of population density.

Distorted trade regime would result in appreciated real

exchange rate, and thus high price level.

Results:

Asian developing countries had the most liberal trade

regimes.

African countries are the least liberal.

84

Latin American countries in between.

Increased trade distortions and increased real

exchange rate variability have significant and large

negative effects on economic growth.

Sachs and Warner (1995):

Factors that determine whether countries with low

income per capita will achieve convergence.

Two conditions are critical: preservation of private

property rights and commercial openness.

Their methodology involves classification of countries

into two groups:

those which safeguarded property rights and

maintained commercial openness (“qualifiers”),

those which did not (“nonqualifiers”).

85

Trade openness was defining characteristic of two

groups, since almost all countries that failed to qualify

on openness criterion also did so on political criterion.

Qualifiers grew more rapidly, and both political and

trade variables had significant partial effects on growth.

No country which maintained substantially opened trade

failed to grow by at least 2% per year during 1970-89.

Conclusion: safeguarding property rights and

maintaining open trade regime

are conducive to growth, and

constitute sufficient conditions for attainment of

rapid economic growth.

86

Frankel, Romer, and Cyrus (1996):

Both of the previous studies leave open direction of

causality between growth and openness.

They addressed this issue by using gravity model to

instrument for openness in cross-country growth

equation.

They found strong positive correlation between

exogenous component of openness and economic

growth.

87

Exchange-Rate Unification

and Growth

Restrictions on financial trades involves foreign

exchange transactions.

Most common form involved capital account

transactions in balance of payments.

Such restrictions have been intensified when domestic

economic distortions have created incentives for

residents to remove funds from the country.

Private agents have sought to circumvent restrictions by

trading foreign exchange outside official markets.

This gives rise to parallel exchange market at which

foreign exchange trades at substantial premium over its

official value.

Effects of removal of restrictions:

Removal of restrictions on capital inflows can generate

89

resources for investment.

Removing restrictions on outflows may do so as well, by

assuring foreign creditors that they will be able to

repatriate their funds when desired, and

reassuring both domestic and foreign investors that

their capital will be less subject to taxation.

Enhanced liquidity provided to domestic residents may

induce them to undertake less liquid but more

productive investment projects.

Financial integration may affect growth indirectly by

fostering deeper domestic financial markets, thus

reinforcing growth benefits of financial deepening.

Evidence:

Evidence on effects of easing of foreign exchange

restrictions on economic growth is of two types:

90

Use of premium on foreign exchange in parallel

markets as a proxy for capital-account restrictions in

cross-country growth regressions.

Assessing whether international financial integration

affects economic growth through indirect channel of

promoting domestic financial depth.

Levine and Zervos (1996):

Provided evidence of the first type.

Used cross-country sample of 119 countries.

In testing for effects of parallel market premium, they

investigated robustness of its role since large premium

may reflect variety of policy distortions.

Result: premium had robust negative partial correlation

with long-term growth.

91

Implication: foreign exchange restrictions exerted

independent negative effect on growth.

De Gregorio (1992):

Provided evidence of the second type.

Explained cross-country differences in measures of

financial depth on the basis of

set of control variables (initial GDP per capita,

average rate of inflation, and measure of commercial

openness), and

measures of degree of international financial

integration.

92

Results:

Three of his measures of international integration had

statistically significant partial correlation with

measures of financial depth.

This is interpreted as evidence in support of indirect

effect.

No evidence of direct effect of openness on growth is

found.

93