Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

International monetary systems wikipedia , lookup

Financial crisis of 2007–2008 wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Patriot Act, Title III, Subtitle A wikipedia , lookup

Systemically important financial institution wikipedia , lookup

Financial crisis wikipedia , lookup

Currency intervention wikipedia , lookup

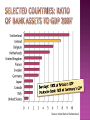

Thorvaldur Gylfason 1929: Compounded by massive public policy failure Monetary contraction (Friedman-Schwartz story) Protectionism (Smoot-Hawley tariff) 1987: Wall Street, again Corrected through monetary expansion (Volcker) 1997: Wall Street collapse Asian crisis Preceded by construction boom in Thailand 2000: Dotcom collapse, limited impact 2008: Subprime loan debacle in US Where will it lead? Repeat from 1929? No. Exposes a fundamental asymmetry of information, leading to grave moral hazard Selling mortgage loans to people with no jobs, no incomes, no money to put down, no means of paying back Bankers convinced subprime customers that they could pay higher interest on their mortgages after a short grace period because house prices would rise, but prices fell Dealers have a vested private interest in making socially destructive deals The most they stand to lose is their jobs The most they can win is astronomical wealth You figure out the average of those two options Need legal protection against predatory lending Like laws against quack doctors, same logic Patients know less about health problems than doctors, so we have legal protection against medical malpractice Same applies to some bank customers vs. bankers, especially in connection with complex financial deals Subprime assets of dubious value were packaged into complex financial instruments of equally dubious value that not even some of the bankers themselves understood … … and were given top ratings by rating agencies paid by the banks that pushed these instruments Do not allow rating agencies to be paid by the banks Fundamental conflict of interest Further, regulation was weak In US, laws from 1930s (Glass-Steagall Act) separating commercial banking from investment banking were deliberately weakened around 1990, permitting banks again to blend the two types of banking Consider merging an electric utility providing a steady stream of electricity to rate-paying customers and a casino, making it possible for the casino, if it goes bust, to bring down the utility But this is controversial because, in good times, the casino can support the utility Need more and better regulation of banks and other financial institutions, but exactly how needs to be worked out Work in progress Read the warning signals Three rules, or stories The Aliber Rule Count the cranes The Giudotti-Greenspan Rule Never allow gross foreign reserves held by the Central Bank to fall below the short-term foreign debts of commercial banks Failure to respect the Giudotti-Greenspan Rule amounts to an open invitation to speculators to stage an attack on the currency The Overvaluation Rule Sooner or later, an overvalued currency will fall Read First story the warning signals Professor Aliber in Iceland 2007: Count the cranes! Bangkok 1996: Many cranes, yes, but no clue Second story Thailand 1996: Ratio of foreign reserves to short-term foreign debt had fallen below the critical number 1 Speculators took notice, and attacked the baht Like others, IMF was caught off guard Iceland took longer: Central Bank foreign reserves dropped from 100% of short-term debt in the 1990s to 6% in 2008 while bank assets rose to 9 times GDP % of short-term debt 140 120 100 80 60 40 20 0 Read the warning Third story signals Overvaluation: Like many African countries, Iceland has a long history of an overvalued currency 2007: Iceland’s per capita GDP had risen to 50% above US per capita GDP Clear sign that correction was due Even so, many households and firms borrowed in cheap foreign currencies at low interest even if their entire earnings were in domestic currency Even senior bankers and ministers did this An indication of wide-spread euphoria Other unmistakable signs Large current account deficits, mounting foreign debts Creeping inflation Pervasive farm support, including fisheries High domestic prices of tradable goods (Big Mac index) Recently, also, carry trade International Investment Position (% of GDP) 0 -20 -40 -60 -80 -100 -120 -140 -160 -180 2004 2005 2007 2007 2008 Do not let banks outgrow Central Bank’s ability to stand behind them as lender – or borrower – of last resort Do not allow banks to operate branches abroad rather than subsidiaries, thus exposing domestic deposit insurance schemes to foreign obligations Without having been informed about it, Iceland (population 300.000) suddenly found itself to be held responsible for the moneys kept in an Icelandic bank by 300.000 British depositors, and more in the Netherlands and Germany Source: Union Bank of Switzerland. 10 9 8 7 6 5 4 3 2 1 0 Switzerland Iceland “A sound banker, alas, is not one who foresees danger and avoids it, but one who, when he is ruined, is ruined in a conventional way along with his fellows, so that no one can really blame him.” J.M. Keynes Icelandic banks copied each other’s business model This can be good when the going is good, but not so good when the sea gets rough Erect Iceland’s privatization of its state banks 1998-2003 was mismanaged in ways that contributed to collapse and to weak restraints on bank growth firewalls between banking and politics Government ought to have constrained the banks through taxes Central Bank ought to have constrained them through reserve requirements Financial Supervision Authority ought to have applied more stringent stress tests, appropriate to local conditions Besides, several earlier episodes of bank problems when banks were state-owned were covered up No accountability When things go wrong, hold those responsible accountable by law, or at least try to uncover the truth: Do not cover up In Iceland, there are now vocal demands for an International Commission of Enquiry, a Truth and Reconciliation Committee of sorts If history is not correctly recorded if only for learning purposes, it is more likely to repeat itself with dire consequences When banks collapse and assets are wiped out, protect the real economy by a massive monetary or fiscal stimulus Think outside the box: put old religion about monetary restraint and fiscal prudence on ice Always remember: a financial crisis, painful though it may be, typically wipes out only a small fraction of national wealth Physical capital (typically 3 or 4 times GDP) and human capital (typically 5 or 6 times physical capital) dwarf financial capital (typically less than GDP) So, financial capital typically constitutes one fifteenth or one twenty-fifth of total national wealth or less Switzerland South Africa Iceland Singapore United Kingdom United States Japan France Russian Federation China India Egypt, Arab Rep. Brazil Mauritius Germany Kenya Botswana Nigeria Ghana Cote d'Ivoire 0 50 100 150 200 250 300 350 Source: World Bank, World Development Indicators 2008. Do not jump to conclusions and do not throw out the baby with the bathwater Since the collapse of communism, a mixed market economy has been the only game in town To many, the current financial crisis has dealt a severe blow to the prestige of free markets and liberalism, with banks having to be propped up temporarily by governments, even nationalized Even so, it remains true that governments are not well suited to own and operate banks, so banks will in due course need to be re-privatized Banking and politics are not a good mix Even so, private banks clearly need proper regulation because of their ability to inflict severe damage on innocent bystanders From the IMF Data Mapper, October 2008 1980 1985 1990 1995 2000 2005 2010 1980 1985 1990 1995 2000 2005 2010