Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

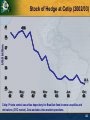

Reducing Public Sector’s FX Exposure: The Brazilian Experience Afonso Bevilaqua December 2003 1 Reducing Public Sector’s FX Exposure: The Brazilian Experience I. Background II. Recent Strategy for Reducing Public Sector’s FX Exposure 2 Reducing Public Sector’s FX Exposure: The Brazilian Experience I. Background 3 Reducing Public Sector’s FX Exposure: The Brazilian Experience From the 80s to 1994: Despite chronic inflation, Brazilian economy has never dollarized. Broad and credible indexation substituted the dollar as an instrument to mitigate inflationary losses. Demand for domestic debt was preserved through indexation mechanisms. 4 Reducing Public Sector’s FX Exposure: The Brazilian Experience From 1994 to 1998: Monetary reform and exchange-rate anchor succeeded in stopping high inflation; Public sector provided dollar-indexed securities, safeguarding the administered FX regime; External crises in mid-90s (Mexico, Southeast Asia, Russia) gradually increased vulnerability of the Brazilian economy, with significant losses of international reserves to sustain FX regime. 5 Reducing Public Sector’s FX Exposure: The Brazilian Experience From 1999 to present: Provision of dollar-indexed securities helped to smooth the transition from administered to floating FX regime, without generalized financial distress or credit crunch; No significant balance sheet mismatches in the private sector; 3 major waves of devaluation after the move to floating regime (1999, 2001 and 2nd half of 2002); Main impact of the 3 waves of devaluation on the public sector’s debt. 6 Debt/GDP Ratio (1994/03) Sep 02 62.5% 65 60 57.7% 50 45 1999-02: FX realignment 40 35 30 Sep 03 Nov 02 Jan 02 Mar 01 May 00 Sep 98 Nov 97 Jan 97 Mar 96 May 95 25 Jul 99 1994-98: lax fiscal policy + high real interest rates Jul 94 % of GDP 55 7 Dollar-Indexed Debt / Total Domestic Debt Ratio (91/03) 40 35 30 % 25 20 15 10 5 0 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003* * October/2003 8 Exchange Rate R$/US$ (1994/03) 4.0 3.5 R$/US$ 3.0 Nov 27 2.94 2.5 2.0 1.5 1.0 0.5 Jul 94 Jul 95 Jul 96 Jul 97 Jul 98 Jul 99 Jul 00 Jul 01 Jul 02 Jul 03 9 Real Effective Exchange Rate (1994/03) 4.00 3.80 3.60 3.40 3.20 R$/US$ 3.00 2.80 2.60 2.40 2.20 2.00 1.80 1.60 1.40 Jul 94 Jul 95 Jul 96 Jul 97 Jul 98 Jul 99 Jul 00 Jul 01 Jul 02 Jul 03 10 Net Public Sector Debt vs Real Exchange Rate (1994/03) 63 4.0 45 Net Debt/GDP 2.5 36 Real Effective Exchange Rate 2.0 Sep 03 Nov 02 Jan 02 Mar 01 May 00 Jul 99 Sep 98 Nov 97 Jan 97 Mar 96 1.5 May 95 27 Jul 94 % of GDP 3.0 R$/US$ 3.5 54 11 Net Public Sector Debt Increase Decomposition - % of GDP (1995/98) 1995 1996 1997 1998 95-98 Net debt increase 1.4% 1.9% 1.1% 7.4% 11.7% 1. Primary surplus -0.3% 0.1% 0.8% 0.0% 0.7% 2. Pure interest on the debt 6.1% 5.4% 4.8% 7.4% 21.2% 3. Depreciation on domestic debt 0.1% 0.1% 0.2% 0.5% 0.8% 4. Depreciation on foreign debt 0.9% 0.1% 0.3% 0.3% 1.2% 5. Skeletons 1.5% 2.0% 0.1% 1.6% 4.5% 6. Privatization proceeds 0.0% -0.2% -1.8% -1.4% -3.3% 7. Effect of GDP growth -7.0% -5.6% -3.3% -1.0% -13.5% Debt dynamics (1+2+7) -1.2% -0.1% 2.4% 6.4% 8.4% Currency (3+4) 1.0% 0.2% 0.5% 0.7% 2.1% Net "skeletons" (5+6) 1.5% 1.8% -1.8% 0.3% 1.2% 12 Net Public Sector Debt Increase Decomposition - % of GDP (1999/03) 1999 2000 2001 2002 2003* 99-03* Net debt increase 7.0% 0.1% 3.8% 4.0% 1.2% 16.0% 1. Primary surplus -2.9% -3.3% -3.5% -3.4% -3.7% -14.4% 2. Pure interest on the debt 8.2% 6.8% 6.9% 7.3% 7.4% 31.1% 3. Depreciation on domestic debt 3.8% 0.8% 1.5% 4.9% -1.4% 8.0% 4. Depreciation on foreign debt 2.8% 0.8% 1.5% 4.5% -2.6% 5.7% 5. Skeletons 1.3% 0.8% 1.5% 0.9% 0.1% 3.7% 6. Privatization proceeds -0.9% -1.8% -0.1% -0.2% 0.0% -2.2% 7. Effect of GDP growth -5.4% -3.9% -4.0% -10.2% 0.6% -16.7% Debt dynamics (1+2+7) 0.0% -0.5% -0.6% -6.2% 4.2% 0.0% Currency (3+4) 6.5% 1.6% 3.0% 9.4% -4.0% 13.7% Net "skeletons" (5+6) 0.5% -1.0% 1.4% 0.7% 0.1% 1.5% * Data for September/2003 13 Reducing Public Sector’s FX Exposure: The Brazilian Experience II. Recent Strategy for Reducing Public Sector’s FX Exposure 14 Reducing Public Sector’s FX Exposure: The Brazilian Experience Different features of the 2001 and 2002 depreciation episodes: 2001: “pure external shocks” increase in demand for hedge. 2002: confidence crises reduction in demand for hedge (and reduction in FX liabilities of private sector). 15 Reducing Public Sector’s FX Exposure: The Brazilian Experience Different responses in the depreciation episodes: In 2001: Net placement of dollar-indexed securities to mitigate impact of increased demand for hedge on the exchange market; Dollar-indexed domestic debt rollover rate reached 137.0%. In 2002, before the crisis: Central Bank introduced FX swaps to replace dollar-indexed Treasury notes (NTN-D); swaps perceived as having lower credit risk (daily margin adjustment) than NTN-D. 2nd Half of 2002: Increased risk perception reduced the rollover rate to 45.2% during August/October, averaging 66.4% for the year. 16 Reducing Public Sector’s FX Exposure: The Brazilian Experience 2003: rapid improvement in fundamentals enabled the Central Bank to actively reduce public sector’s FX exposure; Since the end of May, Central Bank announced that it would not rollover a fixed rate of FX securities or swaps maturing; In July, Central Bank disciplined auction procedures, establishing a maximum of two auctions to be carried out for each rollover; In September, Central Bank reduced number of auctions to one. 17 FX Instruments Rollover Rate* (2001/03) 140 137.0% 120 100 80 % 66.4% 65.8% 60 40 20 0 2001 2002 * Includes rollover of intermediary and final interests Jan/Nov 2003 18 FX Instruments Rollover Rate* (2003) Average Jan/May: 87.1% 100 90 80 85.3 88.1 Average Jun/Nov: 41.5% 91.4 85.0 84.5 81.7 70 % 60 56.2 50 42.3 40 33.9 30 20 7.3 10 2.1 0 Jan 03 Feb 03 Mar 03 Apr 03 May 03 Jun 03 Jul 03 Aug 03 Sep 03 Oct 03 Nov 03 * Includes rollover of intermediary and final interests 19 FX Domestic Debt: Total Outstanding in US$ (1999/03) (Includes Swaps) 2001: Increase of US$ 18.8 billion 80 2002: Reduction of US$ 8.4 billion 2003 to November: Reduction of US$ 6.0 billion US$ billion 75 70 65 60 55 Dec 99 Apr 00 Set 00 Feb 01 Jul 01 Dec 01 May 02 Oct 02 Mar 03 Nov 03 OBS: This behavior is partly explained by the rise and later fall of the FX coupon, which affected outstanding marked to market (see next slide). 20 FX Coupon (2002/03) 90 Pre-elections period 80 70 60 % 50 40 30 20 10 0 -10 Jan 02 May 02 Sep 02 90 days Jan 03 May 03 Sep 03 360 days 21 FX-Indexed Debt/Total Domestic Debt (2000/03) (Includes Swaps) 42 peak in Sep/02 (40.7%), especially due to price-effect (FX depreciation) 40 38 36 % 34 32 30 28 26 Trough in Oct/03 (24.4%) due to price-effect (FX appreciation) and quantity-effect 24 22 20 Dec 99 Jun 00 Dec 00 Jun 01 Dec 01 Jun 02 Dec 02 Jun Oct 03 03 22 FX-Indexed Debt/Total Domestic Debt vs. Exchange Rate (1999/03) 42 4.0 40 38 FX-Indexed Debt/Total Domestic Debt % 34 3.0 32 30 R$/US$ 36 3.5 2.5 28 26 24 Exchange Rate 2.0 22 20 1.5 Dec 99 May 00 Oct 00 Mar 01 Aug 01 Jan 02 Jun 02 Nov 02 Apr 03 Oct 03 23 Stock of Hedge at Cetip (2002/03) 41 40,6 40.6 US$ billion 39 37 35 33 31 30.0 29 Jan 02 May 02 Aug 02 Nov 02 Mar 03 Jun 03 Oct 03 Cetip: Private central securities depository for Brazilian fixed-income securities and derivatives (OTC market). Data excludes intra-market operations. 24 Exchange Rate Volatility (2002/03) Reduction in demand for hedge partly explained by fall in FX volatility 60% 55% Pre-elections period 50% 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% Jan 02 May 02 Sep 02 Jan 03 May 03 Nov 03 25 Reducing Public Sector’s FX Exposure: The Brazilian Experience Main Outcomes: In 2003, Government actively pursued a strategy aimed at reducing dollar-indexed debt; Rollover rate of FX instruments reduced to 41.5% in the June/November 2003 period, without any major effect on the FX market; Share of FX debt to total domestic debt fell to 24.4% in October 2003 from peak of 40.7% in September 2002; Reduction in FX hedge provision by the public sector in 2003 (including early December rollover) reached US$ 17.6 billion. 26 Reducing Public Sector’s FX Exposure: The Brazilian Experience Afonso Bevilaqua December 2003 27