Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

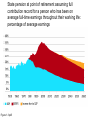

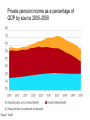

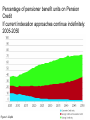

A New Pension Settlement for the Twenty-First Century: Second Report of the Pensions Commission Cass Business School Adair Turner 7 December 2005 • State has been planning a reduced role in pension provision for average earner • Proposition: private pension provision should grow to fill gap • Reality: private pension provision in underlying decline Projected state spending per pensioner indexed in constant 2003/04 price terms: 2004 projections Figure 1.5 p47 Participation in private pension schemes: 2003-04, millions Figure 1.8 p50 • Is there a “crisis”? • Is there a “savings gap”? • If the problem is in the future, can we wait until then to deal with it? State pension at point of retirement assuming full contribution record for a person who has been on average full-time earnings throughout their working life: percentage of average earnings Figure 1.3 p45 Private pension income as a percentage of GDP by source 2005-2050 Figure 1.16 p57 Percentage of 50-65 year olds in danger of having replacement rates below benchmarks of adequacy Figure 1.30 p79 Gross saving by sector as a percentage of gross national disposable income: 1980-2004 Figure 1.33 p83 Residential housing wealth as a percentage of GDP Figure 1.31 p81 Wealth holdings in a closed economy in equilibrium Figure 1.36 p85 Household non-pension financial assets and non-mortgage debt as a percentage of GDP Figure 1.35 p85 Barriers to a purely free market solution • Behavioural barriers to rationality e.g. inertia • High selling costs • Declining employer interest • Complexity • Expectations of spread of means-testing 3 Sources of costs for the median earner aged 40 in the present Stakeholder Pension system Figure 1.52 p111 Typical Annual Management Charge in alternative forms of pension provision Figure 1.27 p71 Percentage of pensioner benefit units on Pension Credit If current indexation approaches continue indefinitely: 2005-2050 Figure 1.22 p64 IFA assessments of attractiveness of different earnings segments: survey results The design of the state system means that the returns to saving for people in this group are good. Figure 1.23 p65 Two major elements of policy • National Pension Savings Scheme (NPSS) • More generous less means-tested state pension provision but at an age gradually rising with increased life expectancy Female cohort life expectancy at 65 30 Years 25 20 15 10 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 Historical Principal 2003-based Principal 1983-based Principal 1992-based Principal 2004-based 2050 Impact of the 1940s-1960s baby boom: ratio of 65+ year olds to 20-64 year olds Figure 1.45 p 99 State pension provision: the unavoidable trade-off Figure Ex.6 p 17 Public expenditure and pension age increases: Pensions Commission proposed range for debate 9 Figure 3.1 p 131 Percentage of adult male life spent after State Pension Age State Pension Age 2005 65 Life expectancy at SPA (years) Percentage of adult life (18+) after SPA 67 2050 68 69 19.4 21.8 20.9 20.1 29.2% 30.8% 29.5% 28.3% More generous state pension in the long-term at a later age: • Unified Citizen’s Pension? • Evolution of present system: BSP and S2P? Preferred way forward 1. Build on current two-tier system and recent reforms, accelerating the evolution of S2P to a flat-rate pension by freezing the Upper Earnings Limit for S2P accruals in nominal terms. 2. Index the BSP to average earnings growth over the long-term ideally starting in 2010 or 2011 as the public expenditure benefit of the rise in women’s SPA begins to flow through ……making this indexation affordable long-term by raising the SPA gradually, broadly in proportion to the increase in life expectancy, for instance to 66 by 2030, 67 by 2040 and 68 by 2050. 3. Maintain the reductions in pensioner poverty achieved by Pension Credit, but limit the spread of means-testing by freezing the maximum level of Savings Credit payments in real terms (which implies that the lower Savings Credit threshold increases faster than in line with average earnings). 4. Base future accruals to the BSP on an individual and universal (i.e. residency) basis, and improve carer credits within S2P. 5. Accept the consequence that the public expenditure on state pensions and pensioner benefits must rise from 6.2% of GDP today to between 7.5% and 8% by 2045 (depending where SPA reaches in 2050). 6. Ideally introduce a universal BSP for pensioners aged over 75. Figure Ex.8 p 21 Percentage of pensioner benefit units on Pension Credit With proposed state system reforms and introduction of the NPSS Figure 6.42 p294 Key features of NPSS • Automatic enrolment, but with right to opt-out • Minimum default employee contributions of 5%, of which 1% paid by tax relief • Modest compulsory matching employer contribution (3%) if employee stays enrolled ………impact on total labour cost 0.6% • Payroll deduction, national account maintenance, bulk-buying: 0.3% annual cost target • Individual accounts invested at individual’s instructions: default fund The role of the state • Ensures that all people are out of poverty in retirement, and creates a sound base on which private savings can build • Encourages and enables low cost saving, but leaves ultimate decisions to individual choice Pension income as a percentage of earnings for the median earner: retiring in 2053 Figure Ex.7 p19 Typical Annual Management Charge in alternative forms of pension provision Figure 1.27 p71 Variability of real returns on equities over historical periods: 1899-2004 Figure 5.24 p197 Variability of real returns on equities over historical periods: 1899-2004 Figure 5.24 p197 Longevity risk in UK pension provision, £billion of total liabilities- broad estimates: end 2003 Figure 5.17 p181 Inflows and outflows from NPSS Figure 6.36 p288 Aggregate NPSS funds at different rates of return Figure 6.37 p288 Stock of annuities arising from the NPSS Figure 6.38 p289 Long-run effect of NPSS on private pension savings as a percentage of GDP Figure 6.39 p289 A New Pension Settlement for the Twenty-First Century: Second Report of the Pensions Commission Cass Business School Adair Turner 7 December 2005