Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

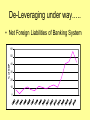

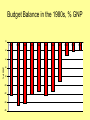

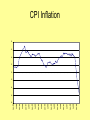

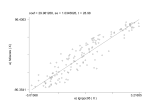

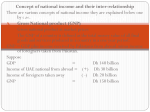

Stabilising the Public Finances Colm McCarthy (School of Economics UCD) McGill Summer School, July 21st. 2009. Fiscal Consolidation in Context….. • There are four priorities in macro policy. • Restore fiscal balance….. • Resolve the banking crisis…. • Restore competitiveness…. • De-leverage the national balance sheet Managing the Balance Sheet • The private sector now owes c. €400 bn to the banking system, one of the highest ratios to GNP in the world. • De-leveraging seems to have commenced • It requires not just an increase in private saving but asset disposal nationally to reduce debt • The State is also funding a book of assets and it may need to de-leverage too De-Leveraging under way….. • Net Foreign Liabilities of Banking System 60 % of GDP 50 40 30 20 10 0 Personal Sector Debt Repayments to Income 25% 10% more disposable income eaten up in debt repayments than seven years ago 20% 15% 10% 5% 0% 2000 2001 2002 2003 2004 2005 2006 2007 2008F Bank Lending to Property 120000 100000 30% Lending to construction development and investment up €100bn in seven years 25% 80000 20% 60000 15% 40000 10% 20000 0 5% Q1 1997 Q1 1998 Q1 1999 Q1 2000 Q1 2001 Q1 2002 Q1 2003 Q1 2004 Q1 2005 Q1 2006 Q1 2007 Q1 2008 Lending to construction and real estate activities (lhs, €m) % of total private sector credit (rhs) Tiger Checked out around 2002 1995 to 2002 • Real GDP • Real GNP • Real GNDI (Adjusted for terms-of-trade) 8.6 7.2 7.0 2002 to 2008e 5.3 5.1 3.5 Property-Related Taxes led the Collapse…. 9000 20% 8000 18% 16% 7000 14% 6000 12% 5000 10% 4000 8% 3000 €6bn drop in direct property-related revenue in three years 2000 6% 4% 1000 2% 0 0% 1997 1998 1999 2000 2001 2002 Property revenue (€m, lhs) 2003 2004 2005 2006 Property revenue % of total tax revenue (rhs) 2007F 2008F 2009F The Budget Gap….. Government spending and revenues 80,000 € million 70,000 60,000 Revenues 50,000 Spending 40,000 30,000 2000 2001 2002 2003 2004 2005 Year 2006 2007 2008 2009(f) The Fiscal Deterioration….. GGB Deficit = 10.75% in 2009 after four sets of policy changes since July 2008 Would exceed 10% for some years thereafter without further measures. GGB Gross debt 41% of GDP at end 2008, will exceed 50% at end 2009. Without bank rescue costs, annual borrowing at 10%+ is dangerous. Bank rescue costs could add two years’ borrowing at this rate, or even more. Raise Taxes or Cut Spending? • Real Total Exchequer spending rose c. 5.7% in 2008 • Will rise even faster in 2009 with negative inflation. • Significant tax increases have already been imposed • The Govt is anxious to avoid heavt further tax increases. Total Exchequer Spend % GNP trends in government spending 60.0 Gross Voted Current Expenditure Central Fund Services (Current) Total Expenditure Exchequer Capital Expenditure (excl. NPRF) NPRF Contribution 50.0 30.0 20.0 10.0 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 1986 1985 1984 0.0 1983 per cent of GNP 40.0 Exchequer Spend excl Debt Service, % GNP trends in government spending 50.0 Gross Voted Current Expenditure Exchequer Capital Expenditure (excl. NPRF) 45.0 40.0 30.0 25.0 20.0 15.0 10.0 5.0 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 1986 1985 1984 0.0 1983 per cent of GNP 35.0 Real Growth, Total Exchequer Spending Year 2000 2001 2002 2003 2004 2005 2006 2007 2008e 2009f Spend % Chg CPI % % Real Growth 10.4 16.1 11.0 7.7 6.2 11.1 10.6 11.8 9.8 6.9 5.6 4.9 4.6 3.6 2.1 2.5 3.9 4.9 4.1 -3.8 4.8 11.2 6.4 4.1 4.1 8.6 6.7 6.9 5.7 10.8 Budget Balance in the 1980s, % GNP 0 1980 -2 % of GNP -4 -6 -8 -10 -12 -14 -16 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 Bord Snip’s Proposals…. • A set of options for Government • Must be seen against background of - borrowing almost €400m. per week - already paying penalty interest rate - difficult borrowing markets - inflation has turned negative Jan-09 Jul-08 Jan-08 Jul-07 Jan-07 Jul-06 Jan-06 Jul-05 Jan-05 Jul-04 Jan-04 Jul-03 Jan-03 Jul-02 Jan-02 Jul-01 Jan-01 Jul-00 Jan-00 Jul-99 Jan-99 CPI Inflation 8 6 4 2 0 -2 -4 -6 -8 Fiscal Consolidation is Unavoidable • Borrowing at 10% of GDP for any length of time is risky, even in benign credit markets • The credit markets are less borrower-friendly than at any time since WWII • Borrowing needs to be contained in 2009 and reduced decisively in 2010. • Cuts in current and capital spending are required, and further tax measures cannot be ruled out.