Survey

* Your assessment is very important for improving the workof artificial intelligence, which forms the content of this project

Competition (companies) wikipedia , lookup

Currency War of 2009–11 wikipedia , lookup

Foreign exchange market wikipedia , lookup

Bretton Woods system wikipedia , lookup

Purchasing power parity wikipedia , lookup

Foreign-exchange reserves wikipedia , lookup

Currency war wikipedia , lookup

International monetary systems wikipedia , lookup

Fixed exchange-rate system wikipedia , lookup

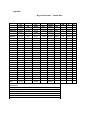

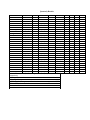

St. Michael’s College Center for Social Science Research Working Paper Summer / Fall 2008 “The Impact of Exchange Rate Changes on the Trade Balance of ex-Soviet Transitioning Economies” Dmitri Repnikov Introduction: Today’s global markets have grown to be sophisticated and especially interconnected. At times globalization proves to be painful (job losses, off-shoring), however, in the long-run everybody benefits from gains in productivity and lower prices of goods and services. Trade policy, such as protectionism and exchange rates, play crucial roles in enhancing a country’s standard of living. This paper will analyze the impact of exchange rate changes on the trade balance of ex-Soviet states after the fall of communism by using the Ordinary Least Squares (OLS) method. The J-curve hypothesis is also under examination. Central and Eastern European countries (CEEC) are extraordinary in that they have been the poster child for economic reform going from planned to market economies. Most of these nations initially experienced significant declines in output due to the magnitude of reform. Although, the transition was later praised by economists once CEECs stabilized their economies, increased growth and employment and established themselves within the international community. This paper is split into several parts: first, it is important to introduce the background regarding trade, the balance of payments (BOP), exchange rates, and other measures authorities can implement to change the flow of goods and services. I then review related studies that have examined the role of exchange rates on the trade balance. Next I go over the methodology, advantages and limitations of this study. Finally, the conclusion brings about the summary, final remarks, and implications for future research in this field. Tables and graphs are in the appendix. Background: The BOP is one of the most important economic indicators in terms of policy making as it records all economic transactions between residents of a particular country and those of the rest of the world in a given time period. Among other financial data, it reveals how much an economy has been importing and exporting and whether the country has been lending to or borrowing from the rest of the world. By definition, the BOP is the sum of the current account, which mainly measures the flows of goods and services; the capital account, which consists of capital transfers and the acquisition and disposal of non-produced, non-financial assets; and the financial account, which records investment flows (NY FED). The BOP statement plays an important role in influencing other economic variables and policy decisions, such as the exchange rate, foreign and domestic growth and inflation. The BOP accounts are ever more significant as the degree of capital mobility and international trade have drastically evolved since the end of the gold standard in 1971. It is not just corporations, governments and central banks that invest in international assets – private actors have greatly increased their involvement in recent years. For example, there has been a 15% average annual rate of increase in total international bank lending from $442 billion in 1975 to $11,048 in 1998. The value of world exports has sky-rocketed over 2000% in the past few decades, from $582 billion in 1973 to $14472 billion by 2005 (Field, 2001). In other words, the world economy has seen a very rapid growth in international transactions, which have become very efficient, yet quite complex and all at once. The BOP balance can be thought of as the sum of the current and capital accounts. The BOP always balances out since each credit in the account corresponds with a debit somewhere else, also known as double-entry bookkeeping. However, this is not necessarily the case for individual economies, such that of the United States today. A BOP deficit usually makes the news and newspaper headlines, but it is important to note that it refers to only some part of the BOP statement – the term lacks precision in indicating which item in the account is being talked about (Field). Therefore, the focus of this paper will shift to the current account and more specifically study the balance of trade, or exports minus imports, for the period of changes in exchange rates. The current account reflects sources and uses of national income since exports produce domestic income which is then used to purchase imports of goods and services from abroad. A current account deficit means that a country spends more than it earns, ergo a very low savings rate relative to its investment, which suggests that a country must import supplementary foreign capital in order to sustain its spending. For example, the US has had a current account deficit (CAD) since the early 80s (with the exception of President Bush’s last term in the ’92) and stands today around 7 percent of its gross domestic product (GDP) (The Economist). Some economists argue that this position is not sustainable since foreign investors may cutback or stop the inflow of their financial assets if they feel like there is a greater chance in the US defaulting (the fundamentals of the US economy are quite strong and the chances of default are virtually zero, hence there is no incentive for capital outflow like in the case of the Latin American debt crisis). This would lead to less demand for the US dollar and therefore an eventual depreciation of the USD. A weaker dollar pushes up the prices of imports and also makes domestic products more competitive on the world market. Another potential problem with consistent deficits is the rapid growth of payments as return to foreign investors, which not only worsens the CAD but may lead to a “debt trap” (Field, 2001). Although a continuous CAD can not be ignored by policy makers, there are times when a CAD can be viewed in a positive manner – some argue that large deficits should not be worried about in today’s financially-advanced world. For example, Greenspan argues that the recent drastic change in countries’ surplus and deficits is an inevitable results of globalization and deregulation (Korporaal). For example, the US and Australia have carried large deficits for the past couple of decades mainly driven by a sharp gap between savings and investment. However, nations’ measures of wealth no longer consists of BOP surplus and the amount of gold in reserves. A CAD could also reflect the natural cycle of an economy rapidly pulling out of a recession where higher incomes lead to an increase of imports or the country may seem like an attractive source of foreign investment because of stable business / political conditions or higher rates of return (Field, 2001). It is also natural to see developing countries in deficit as they industrialize since it requires a large inflow of investments. High debt and large deficits do imply a degree of vulnerability and external shocks, especially for small open economies. However, it may also be a sign of economic resilience where foreign investors nonetheless are confident in keeping their assets in an indebted country. It is worth looking for the source of the deficit – raising taxes or cutting on government spending may be the remedy if the economy is in large budget deficit (when the government spends more than it collects in taxes). Although, there is no single agreed upon definition of a BOP disequilibrium, it is not what the statistics show in the short run, but what they reveal over a period of time about the direction of the economy (Pilbeam, 2001). Economists’ views on BOP deficits have changed dramatically since the break down of the fixed exchange rate and the Breton Woods system in 1971. The current account balance was seen as a very important economic variable and therefore, CADs were signals for immediate macro policy action, such as tight monetary or restrictive trade policies. However, as exchange rates were left to freely float and capital mobility increased, contradictions quickly surfaced against the arguments for the old view of CADs. The current account is not seen as such a vital variable anymore. Deficits are not necessarily bad just as surpluses are not necessarily good. It is also believed that it is best to keep the optimal level of the CA variables consistent. For example, the right rate of investment, taxation, or government expenditure. From a policy perspective there are multiple ways to improve a trade deficit. Quotas, tariffs, subsidies and other import restrictions all interfere with the free flow of goods and services. These beggar-thy-neighbor policies are believed to improve the trade balance by reducing imports and protecting infant industries against established international firms. A tariff is an import duty or a fixed monetary tax per physical unit of the good imported (Field, 2001). The export side can be manipulated by export taxes, which usually induces domestic producers to lower the price and sell in the relatively tax-free domestic market rather than export their goods (Field, 2001). It can be beneficial in developing countries by means of raising government revenue and lower inflationary pressures. An export subsidy is a payment to a firm by the government when a unit of a good is exported, attempting to increase the flow of trade (Field, 2001). This pushes the domestic price up leading to a reduction in consumption and a price decline in the world market. Lately, however, policymakers have shifted away from distorting free trade and began to adapt less visible forms of trade barriers – non-tariff barriers. An import quota differs from a tariff in that the interference with prices that can be charged on the domestic market for an imported good is indirect – quotas operate directly on the quantity of the import instead of the price / percentage tax (Field, 2001). There are other domestic policies that affect trade and competitiveness, such as government subsidies to firms and spillovers from government expenditure. In open economies with floating exchange rates protectionist policies actually diminish gains from trade and despite popular belief they do not successfully alter the trade balance due to the appreciation of the ER (Mankiw, 2007). These policies can also lead to unintended consequences as other countries may retaliate with barriers of their own further reducing the amount of trade. Since the trade balance is determined by the difference between savings and investment at the world interest rate, it is more useful to evaluate the fiscal and monetary policies rather than focusing on protectionism (Mankiw, 2007). In short, when the ER is left to float, expansionary domestic fiscal policy leads to a trade deficit because it reduces national savings, while expansionary fiscal policies in a foreign economy (large enough to influence in i*) tend to improve the domestic trade balance since the increased cost of borrowing depress investment. Therefore, it is important to assess domestic saving and investment when evaluating trade policy in flexible ER environments. In contrast, trade restrictions paint a very different picture under fixed ER, which is more relevant in this study as the majority of former Soviet countries have their ER tightly pegged. Rather than seeing the ER appreciate in regards to a protectionist policy, in this case there is an increase net exports because the authorities buy domestic currency with reserves in order to keep the ER fixed. In other words, this accommodating expansionary monetary policy increases the aggregate income and boosts employment. Choosing an Exchange Rate Regime After all, one of the most important economic variables is the exchange rate. It specifies how much one currency is worth in terms of another and its fluctuations determine countries’ term of trade. The link between the exchange rate and the BOP can be readily shown using supply and demand for a given currency. The foreign exchange market is one of the largest markets in the world, which encompasses a daily trade average of US $4 million (Wikipedia). The US supply of foreign currency is essentially the foreign demand for US dollars (USD) – Americans do not demand euros for its intrinsic value, but rather for what they can buy with it. As the dollar appreciates (when it takes less USD to buy a Euro) the cost of US exports becomes cheaper for Europeans, which increases the demand for dollars and boosts the quantity of euros in the foreign exchange market. The equilibrium exchange rate is determined by the intersection of the supply and demand curves where a surplus in one account of the BOP exactly offsets a deficit in another account. However, an increased demand for dollars under a fixed-exchange rate regime puts pressure on dollar to appreciate. Since the authorities try to keep the dollar at a fixed rate, it is necessary for the central bank to intervene by purchasing foreign currency with the dollars (the dumping of dollars into the FX market increases supply and eliminates excess demand). During the Bretton Woods system the exchange rate regime was a fixed peg to the gold-backed (USD). Each country had a reserve of gold and agreed to exchange its currency for a predetermined amount of gold. BOP-deficit countries were expected to borrow and finance their debt via the International Monetary Fund (IMF). Borrowing was limited to 125% of a country’s quota, which depended on the size of their economy among other factors. However, the greater a country borrowed the more interest it had to pay off along with increased supervision of tight IMF policy implications and suggestions. Deflationary policies were not desired at the time since many WWII-battered nations were in their rebuilding stages with mainly growth and expansion in sight. Interest rate hikes were not popular at the time because capital flows were still seen as immobile and destabilizing. It was only after persistent deficits or a “fundamental disequilibrium” that the IMF allowed countries to use their last option and devalue. Devaluation is a political decision in which there is a deliberate decrease in the official value of domestic currency in regards to foreign currency – under a floating exchange rate regime, however, supply and demand determine the range of the deprecation or appreciation. By devaluating its currency, a country makes its exports cheaper relative to the goods and services abroad. It also discourages imports as the price of foreign goods increases. The European transition countries had to decide on numerous fundamental political decisions in the beginning of their reforms. Along with decentralizing the economy, privatizing and liberating prices authorities needed to decide on the optimal choice of monetary policy. According to Alogoskuofis (1989), the choice between fixed and flexible exchange rates depends on two sets of factors: domestic incentives to create unanticipated inflation and the variability of idiosyncratic shocks that call for different monetary policy across countries. The choice involves balancing these two sets out, which will depend on how convincing the central bank is about low inflation, as well as the extent to which the option of joining a credibly antiinflationary international ER regime. A fixed ER regime is said to provide discipline that is needed to prevent continuing inflation (Field, 2001). Foreign direct investment is also believed to be greater under fixed ER in the long-run due to reduced uncertainty and less ER risk. Bofinger (1991) further argues that a floating ER needs to be accompanied by an independent monetary policy which is not realistic in the case of these emerging economies because economic variables are bound to change unpredictably. He also notes that a floating ER is expected to function efficiently only in the presence of a well-developed capital market which these countries lack as well. Lastly, extreme ER misalignments (speculative bubbles) may produce large trade imbalances, which is especially undesirable for economic recovery. Advocates of floating ER regimes claim that governments lack the knowledge to pick the right ER. There is also the vicious circle hypothesis which states that inflation in a country with fixed ER becomes self perpetuating. Those in favor of the floating ER also argue that fixing the ER interferes with efficient resource allocation causing price distortions that do not reflect true scarcity values (Field, 2001). Thus, a flexible ER regime would not only free up resources that can be used elsewhere in the economy, but it would also insulate an economy from external shocks better than fixed ER. Hutchinson and Walsh (1992) found that the GNP decline under fixed ER was much greater than that of floating ER economies following the oil shocks of the 1970s. Therefore, it is believed that transitioning economies should fix their ER for a while after liberalizing prices, which provides an anchor for the new price structure in the short run (Williamson, 1990). A fixed ER regime is less compelling in the long run due to asymmetric shocks and the fact that a country without reserves can not defend a pegged exchange rate. Monetary / Fiscal Policies under Fixed Exchange Rate Regimes: When authorities conduct an expansionary monetary policy, they purchase bonds from the public market, which drives up bond prices and thus leads to a fall in the domestic interest rate. The cut in the interest rate stimulates investment and a rise in output. Similarly to increase output, the government finances fiscal expansion by selling bonds to the public. This drives bond prices down and raises interest rates, thus offsetting the expansionary effect to a certain extent. However, it is crucial to distinguish the important implications of macroeconomic policies under a fixed ER regime. When a country fixes its exchange rate to the USD for example, its Central Bank stands ready to buy and sell domestic for foreign currencies at a predetermined rate. This country gives up its monetary autonomy (gives up control over its money supply) – assuming it still prefers to have open capital markets. Economists refer to this as the “tying of the hands” because effectively the US is be running the other country’s monetary policy. An increase in the money supply boosts the initial real balances which leads to an increase in output and the demand for labor. Yet, the fall in interest rates creates a BOP deficit due to the excess supply of domestic currency on the FX market and in order to keep the ER fixed authorities buy back their currency with reserves. This indeed reduces the money supply and output while raising interest rates. Conversely, authorities can practice sterilization by ensuring that reserve changes due to intervention do not affect the domestic money base. In this case, the central bank would keep the money base (domestic bonds + reserves) constant by a further expansion of the money supply which is precisely offset by the loss of reserves. This can only be carried out in the short run as the country will eventually run out of reserves and be forced to devalue (Pilbeam, 1998). Therefore, monetary expansion is ineffective under a fixed-ER regime. On the other hand, fiscal expansion (tax cuts or money financed increase in government spending) under a fixed ER regime causes capital inflow due to the upward shift in the interest rate. To avoid appreciation of the ER the central bank buys foreign currency with domestic currency. This increase in the money supply raises the national output. Thus, fiscal expansion is useful in raising a country’s national income. Under a flexible ER regime, fiscal expansion tends to raise interest rates above world interest rates causing a massive capital inflow and ultimately an appreciation of the ER. The foreign capital inflow not only tends to push the interest rates back to the world level, but it also reduces net exports due domestic goods being more expensive relative to foreign goods. Consequently, the fall in exports exactly offsets the effects of the fiscal expansion on national income (Mankiw, 2007). Before analyzing the literature and the effects of devaluation, it is important to chip away at a couple of different schools of thought in regards to the BOP. The monetary approach, pioneered by Whitman (1975), Frenkel and Johnson (1976), focuses on a country’s supply and demand for money. According to this view, disequilibrium in the money market leads to BOP imbalances or appreciations and depreciations in the exchange rate. The money market is in equilibrium when the amount of money in existence – supply, which consists of domestic bond holdings and the reserves of foreign currencies help by the monetary authorities, is equal to the amount of cash balances that the public desires to hold – demand, which is a function of real income, price level and interest rate. However, when money supply is greater than demand, the cash people have on hand and in their bank accounts exceed their desired amount. This results in a BOP deficit or a depreciation of the home currency since individuals will now spend more money on goods and services. On the other hand, BOP surpluses or the appreciation of the exchange rate occur when the demand for money is greater than the supply. In this case the boost of exports eventually strengthens the domestic currency, which then lowers domestic prices and finally decreases the demand for money to be in equilibrium with supply. In terms of the effects of devaluation, the monetarists argue that there will be positive transitory effects as long as the authorities do not simultaneously conduct expansionary open market operations where the central bank purchases treasury bonds held by the public, and thus increasing the money base (Pilbeam, 2001). This model suggests that changes in the exchange rate are viewed as ineffective in terms of bringing about a permanent change in the BOP – it is all short lasting, until equilibrium is stored in the money market via reserve changes (Pilbeam, 2001). Even though the monetarist camp agrees on no policy concern with regard to the BOP (since it is a transitory effect), its advocates differ on views and assumptions which causes disagreement over this approach. However, if a country chooses to fix its exchange rate, it will lose its monetary autonomy – also known as the impossible trinity (a country can not have all of the following: an independent monetary policy, a fixed exchange rates and open capital markets – authorities must choose two out of the three accordingly). In contrast to the monetarist model of money imbalances, the Keynesian side focuses on a nation’s competitiveness. By imposing several assumptions (perfect capital mobility, full employment level and that purchasing power parity holds) of the monetarist model, the Keynesian approach predicts much of the same outcomes in regards to the behavior of the BOP when putting an economy through various shocks, such as a CPI or an interest rate hike. The methodology of this school of thought begins with the elasticity approach, pioneered by Alfred Marshall and Abba Lerner. It refers to the responsiveness of imports and exports to the change in value of nation’s currency. For example, if import demand is highly inelastic (not responsive to changes in the exchange rate – like goods without substitutes, such as gasoline), a deprecation of the domestic currency is not likely to slow import all that much. On the other hand, devaluation is bound to have positive effects when a country’s price elasticity of demand is elastic, or is responsive to changes in the prices. While estimating actual elasticities in international trade is complicated, the Marshall-Lerner condition says that devaluation will improve the current account only if the sum of foreign elasticity of demand for exports and the home country elasticity for imports are greater than unity. In contrast to the monetary approach, it suggests that there are two direct effects of a devaluation on the current account – the price and the volume effects, one of which improves the CAD, while the other actually worsens it. The price effect deteriorates the current account because imports are now relatively more expensive for residents. Conversely, the volume effect recognizes that exports become cheaper and should contribute to improving current account. There are two opposing forces in response to devaluation and the net outcome depends on which effect dominates. Even though conventional wisdom says that a nominal devaluation is supposed to improve the trade balance and help correct external imbalances, the literature is somewhat divided on its impact. Despite all the empirical research, the effects of exchange rate changes relating to the trade balance are still not well understood due to undesired growth and inflation patterns. It is widely agreed, however, that in the short-run devaluation may cause a negative shock to the trade balance followed by an improvement in the long-run. This phenomenon is known as the J-curve. The slow responsiveness of export to import volumes is said to hold for several reasons post-devaluation. For one, it takes time for consumers in devaluing countries and the rest of the world to adjust to changes in competitiveness. There is also a time lag in producer responses not only because it takes to expand production, but because orders for imports are usually made well in advance and these contracts can not be easily canceled in the short-run. In addition, payments for many imports may have been hedged against exchange rate risk and therefore will be left unaffected by the devaluation (Pilbeam, 2001). Lastly, in response to a loss of competitiveness, foreign import competing industries may reduce their prices in their home markets, thus limiting the amount of additional exports by the devaluing country (Pilbeam, 2001). Firms would not be able change prices in a perfectly competitive environment as they make normal profits and would rather be looking at reasonably tight margins. In other words, short-run elasticities of supply and demand tend to be smaller than the long-run elasticities, which implies that the Marshall-Lerner condition may not hold in the short-run. In fact, Kahn (1985) concluded that long-run elasticities (>2 years) are approximately twice as much a short-run elasticities (0-6 months). Hence, the longer consumers and producers remain unresponsive to changes in prices, the greater the J-curve effect. Although there is no clear answer as to whether devaluation leads to an improvement in the current account, along with high elasticities, it is more likely to succeed when authorities adapt appropriate fiscal and monetary policies. Due to an increase in the price of imports becoming and stimulating demand for domestic goods, devaluation can cause inflationary pressures. Therefore, authorities have to implement tight monetary policies, such as raising interest rate at the cost of growth. As mentioned previously, adopting a fixed ER regime can help restrain inflationary pressures. For example, in 1991 the doomed country of Argentina established a currency board which maintained a one-to-one peg to the USD. By the end of the decade the six-digit inflation rate had fallen to 1% and real output per person grew at an annual rate of 4.6 from 1992 to 1998 (Field, 2001). In fact, after analyzing 19 independent devaluations, Bhagwat and Onitsuka (1974) conclude that the major element in the postdevaluation export performance was the effectiveness of the supporting financial policies in the controlling domestic demand and in the accompanying development. DECLINE IN OUTPUT IN TRANSITION ECONOMIES Review of Literature: Literature dating back to the 1940s attempted to find a relation between changes in exchange rates countries’ trade balances. Alexander (1952) was one of the first pioneers to examine the effects of devaluation on the trade balance. Alexander claims that the elasticities approach depends on the behavior of the economy as a whole rather than a few variables. Therefore, he goes straight into the absorption method, which is based around several effects on income. Alexander argues there will be an increase in production due to devaluation, however, also deterioration in the terms of trade. Following the suspension of gold convertibility and the devaluation by the United States, Magee (1973) examines the implications on the U.S. trade balance. Magee starts with the currency contract analysis which deals with the brief period immediately following a devaluation in which contracts negotiated prior to the change fall due. He also puts forward the pass-through problem which refers to the behavior of global prices on contracts agreed upon first the devaluation has taken place but before it has effected significant changes in quantities (Magee, 1973). According to his analysis, after the behavior of the trade balance largely depends on which currency the contracts are denominated in. For example, if a contract is denominated in foreign currency, then the U.S. exporter obtains capital gains since the foreign currency would be more expensive compared to the dollar. In other words, if U.S. export contracts are denominated in foreign currencies, a large increase in U.S. export prices in dollars would occur immediately, while if they are denominated in dollars, there would be no significant change in export prices immediately after devaluation (Magee, 1973). The passthrough is also important because there are incentives to alter purchases of foreign goods only to the extent that the prices of these goods change in terms of their domestic currency following depreciation (Magee, 1973). However, Magee further points out that immediately after devaluation, supply and demand may be inelastic due to lags. Thus, we see an initial decline in the trade balance post-devaluation. A pass through refers to for example, the inelastic demand for U.S. import – where the prices imports rise by the full amount of devaluation. Magee sees the deterioration in the U.S. trade balance as a result of a rapid U.S. expansion relative to foreign expansion as well as the presence of considerable lags following the devaluation. Trade balance behavior and the path of adjustment depends on what happens in the pass-through period. Magee concludes that even though there may or may not be a clear J-curve effect, the long-run impact of a devaluation on the trade balance is favorable. Miles (1979) uses a pooled cross-section time-series regression technique on 14 countries to examine the effects of a devaluation on trade balance and the BOP in the 1960s. The variables included in his model are the trade balance, exchange rate, level of output, growth rates of income, ratio of government consumption to output and the ratio of the average level of high-powered money. Rather than checking for the Marshall-Lerner condition, Miles puts the country equations through a regression using Aitken’s generalized least squares to estimate the coefficients. He then conducts residual tests, in which he excludes the exchange rate from the equation to see the effectiveness of devaluation. The average residuals were small but positive in the two years prior to devaluation; however in the year after, there is a very large negative residual. In other words, devaluation had a negative impact on the trade balance. Even after doing a pooled cross-section time series regression and testing for leads and lags, Miles finds additional evidence of that devaluation does not improve the trade balance. Results for the BOP case were strikingly the opposite, which is consistent with the prediction of the monetary approach – improvement in the capital account, otherwise known as a temporary portfolio adjustment. This model was criticized on the grounds that the dependent variable in the model should be the trade balance itself and not the ratio of the TB to income (Oskooee). Furthermore, Miles’ data were stationary, whereas later econometric literature points out that in non-stationary methods, standard critical values used in determining the significance of estimated coefficients are not valid (Oskooee). Oskooee and Alse (1994) negate the flaws of Miles’ analysis to reexamine the long-run and short run relationships between the trade balance and the exchange rate by using the cointegration and error-correction modeling techniques, which is believed to produce more accurate short-run forecasts and therefore obtain the long-run equilibrium. The non-stationary time series method was then performed on 19 developed countries and 22 less developed ones using a lag operator and the error correction term. The variables in this study included the real effective exchange rate and the real trade balance defined as the ratio of a country’s imports to its exports. This ratio is not sensitive to units of measurement and is not deflated by the domestic price index (Oskooee). After conducting the ADF test, which determines the degree of integration of each time series, the study goes on to compare the ADF statistics to its critical values in order to integrate the countries into four groups. Oskooee and Alse conclude with mixed results. Out of 20 countries for which the method could be applied, only six countries proved to have the real effective exchange rate and the trade balance co-integrated. However, out of the six countries, four were in support of the J-curve. A more recent study by Hacker and Hatemi (2003) investigates the validity of the jcurve in Sweden, Norway, Denmark, Belgium, and the Netherlands. An impulse reaction function generated from a vector error-correction model is used to relate the real exchange rate, export / import ratio, real exchange rate, and domestic and foreign outputs. Hacker and Hatemi consider not only quarterly, but also monthly data since it may detect the price effect to be stronger than the volume effect. They also aggregate the data and log the variables to better explain the coefficients and see how exchange rate movements impact trade. After testing for co-integration, they examine the generalized impulse response function of the logged export / import ration with respect to one standard deviation change in the logged real exchange rate – this method is beneficial because it is not sensitive to the order in which the variables are entered in the model (Hacket and Hatemi, 2003). With careful consideration of optimal lag lengths and other time series properties, the study is found to be supportive of the j-curve effect. Gomez and Paz (2004) did a short examination of the behavior of the Brazilian trade balance post devaluation. In contrast to past studies which found no evidence of the j-curve, this one uses the VEC model which can lead to a better understanding of the nature of any nonstationary among the different component series and can also improve longer term forecasting over an unconstrained model (SAS Institute, 2002). METHODOLOGY Countries of interest in this study are the transitioning ex-Soviet economies mainly in Europe. It includes Estonia, Latvia, Lithuania, Poland, Armenia, Moldova, Georgia, Russia and Ukraine. All the data was collected from the International Monetary Fund online database of “International Financial Statistics” as well as World Bank’s “World Development Indicators.” Though, the data availability varied from country to country. In order to investigate the relationship between changes in the exchange rate and the trade balance, I used the Ordinary Least Squares (OLS) technique. This is the most common regression procedure which is based around the line of best fit. It minimizes the summed, squared residuals (error terms) making the regression estimates as close to the true values as possible. Consider different values of the trade balance plotted on a graph. The OLS attempts to find the line of best fit by minimizing the sum of squared elements from the deviation vector. Thus, the linear regression investigates how much of the relationship a country’s GDP, world GDP, and the exchange rate can explain in the variance of the trace balance – the better the line fits around the actual plotted points, the greater the confidence in the independent variables explaining the discrepancy. Before analyzing the model, log specification was applied to both sides of the equation. This technique makes analyzing the results much easier as the coefficients convert to percentage terms, rather than regular units which often have to be interpreted in the scientific notation. Thus, the new multivariate regression model takes the form of: Log TBt α β Log Yd,t γ LogYW,t λ Log REX t ε t (1) Where TB is the trade balance, Y is the domestic GDP, Yw is the world GDP, REX is the exchange rate, and e is the error term. REX is measured as domestic currency per unit of SDR (special drawing rights). SDR is a basket of currencies currently consisting of the USD, euro, pound and the Japanese Yen. Each currency’s share in the SDR is determined by its magnitude in regard to international trade and finance. Along with gold and foreign reserves, the SDR is another form of an international reserve asset in a central bank’s balance sheet. SDRs were created after the break down of the gold standard and have served as an important tool in international economics. The trade balance is defined as exports over imports. It is essential to obtain a ratio since it is not possible to take logs of negative numbers if a country were in a trade deficit. The domestic GDP is measured in national currency. World industrial production is a proxy for foreign quarterly GDP in this study – it should be a fairly accurate approximation of the world’s real GDP. However, in the annual analysis foreign GDP is measured in real 2000 USD provided by the World Bank indicators. A devaluation should lead to the improvement of the trade balance. Therefore, I expect REX coefficient to be positive – an increase in the value of the ER coefficient suggests that the ER has been devalued / is depreciating against the SDR index of currencies, which should induce more exports / less imports. The Y and Y* coefficients could be positive or negative. Economic theory suggests that a rise in domestic income leads to an increase in imports; however, if this growth is export-led which is evident in emerging economies, the trade balance should improve. The Y and Y* estimates depend on the countries’ and their trading partners elasticities of demand for import and exports, therefore the coefficients may be positive or negative. LIMITATIONS As previously noted, data availability remains a large constraint in regards to conducting research for the CEECs. For example, Ukraine does not have sufficient data prior to 1998. Also the ER based on the domestic currency’s value versus the SDR is not the most favorable. The USD, which is a major component of the SDR at times can be volatile and experience large movements in its ER, thus it does not reflect true ER movements in the countries of interest. Apart from data, a major setback of this study can be attributed to the inability to empirically test for the J-curve effect. Again, this involves implementing sophisticated econometric models which are beyond the scope of this paper. Furthermore, it is difficult to interpret the quarterly results in an unbiased manner due to possible multicollinearity and a several of cases of serial correlation. Again, fixing these violations of the classical assumptions involves techniques beyond the scope of this paper, but will surely be implemented in future research. RESULTS AND CONCLUDING REMARKS This study has attempted to shed more light on the post-socialist economic transition, specifically on devaluations and its implications on the trade balance of the countries of interest. In short, there was no gain without pain for the transitioning CEECs. High inflation and an output collapse characterize the subsequent few years after the collapse of the USSR. Although the effects of devaluation varied from country to country, it is essential for countries to have fiscal and monetary discipline to hold inflation in check, since high inflation can quickly offset the positive effects of a devaluation and bring economic growth to a halt. The effects of devaluation are still vague in this research partially because the countries studied are each other’s major trading partners. Therefore, it may have been more favorable to disaggregate the data and study ER sensitivity in regards to bilateral trade, etc. Anyhow, the exchange rate coefficient was positive (see appendix for all results) suggesting that depreciations in the ER eventually improve the TB in the long-run. The long-run is thought of when the ER is passed through and is in its equilibrium. The effects of domestic and foreign outputs on the trade balance also differ and depend on countries’ demand and supply elasticities. It can also be observed that the CEECs that kept their ER from large fluctuations enjoyed better macroeconomic performance along with greater improvements in their balance of trade in the long-run. Lastly, it is important to emphasize the negative effect of repeated devaluations (Ukraine, Moldova, Georgia), which progressively hurt the economy and prolonged their exchange rate realignment. Transition is the simultaneous change of economic structures and institutions and the final outcome largely depends upon the economic reform in terms of liberalization of goods and factor markets, macroeconomic policies and institutional development. The results indicate that policymakers in CEECs can not use exchange rate policies alone to promote large balance of trade surpluses and hence economic growth. Other policy channels, such as monetary and fiscal policy, become more important than ever. Therefore, policymakers may need to pay closer attention to the importance of fiscal discipline and the close coordination of monetary and fiscal policy in these economies to achieve economic growth. Reducing exchange rate fluctuations, controlling inflation and adopting the euro as early as possible may also be beneficial to the countries of interest. An early rush to the euro, however, is not advisable for countries with significant lack of monetary and fiscal convergence. IMPLICATIONS FOR FUTURE RESEARCH It will be most favorable to include the real effective exchange rates (REER) in partially explaining the variance in countries’ trade balance. In order to be consistent, I used the SDR definition throughout the whole study due to lack of data availability for other measures of ER. REER are useful because it is an average of the bilateral real ER between the country and each of its trading partners, weighted by the respective trade shares of each partner (IMF). REER reflect true movements in the ER, rather than being dependent on the SDR. Perhaps it would be useful to investigate trade on a bilateral level – Country A vs Country B, rather than Country A vs the rest of the world. Bilateral data may shed more light on the Jcurve hypothesis and more accurate cross country results. Trade at the commodity level reduces aggregation bias and will be able to further elucidate on the behavior of trade flows. Regardless of future research methods, the availability of monthly data should serve a useful purpose and make analysis less restricted. As noted earlier, more complex models will serve a useful purpose. In an effort to test the J-Curve phenomenon which is a short-run concept, one should incorporate the short-run dynamics into the long-run model. The easiest way to do this is to use an error-correction modeling format. Coinegration refers to matching the degree of nonstationarity of the variables in an equation in a way that makes the error term stationary (its mean and variance is constant over time). It would be interesting to introduce money, credit, government and taxes into the model and attempt to evaluate the impact of these variables. Testing ER sensitivity at the commodity level may also reveal greater effects of the J-curve. While I may have only scratched the surface of econometric research, this study has been very beneficial to my learning and hopefully future adjustments of this paper can make it useful to the international community as well. In the near future, I will attempt to examine the reasons for the drastic exchange rate appreciations in CEECs. By using more complex modeling and with greater data availability I hope to find whether these appreciations can be attributed to increases in tradable-goods labor force productivity, also known as the Balassa-Samuelson effect. Bibliography Alogoskuofis, G.S. (1989) “Monetary, nominal income and exchange rate targets in a small open economy,” European Economic Review 33, 687-705. Bahmani-Oskooee, "More Evidence on the J-Curve from LDCs,"JOURNAL OF POLICY MODELING,Vol. 14 (October 1992), pp. 641-653. (with M. Malixi). Bahmani-Oskooee, M. and A. Kutan, "The J-Curve in the Emerging Economies of Eastern Europe”, Applied Economics, forthcoming. Bahmani-Oskooee, “Short-Run vs. Long-Run Effects of Devaluation: Error-Correction Modeling and Cointegration” EASTERN ECONOMIC JOURNAL,Vol. 20 (Fall 1994), pp. 453-464. (with J. Alse). Bahmani-Oskooee, “Devaluation and the J-Curve: Some Evidence from LDCs,"THE REVIEW OF ECONOMICS AND STATISTICS,Vol. 67 (August 1985), pp. 500-504. Bhagwat, A. and Onitsuka, Y., 1974, “Export-Import Responses to Devaluation. Experience of the Nonindustrial Countries in the 1960s”, International Monetary Fund Staff Papers, July. Field, Alfred Jr and Appleyard, Dennis, “International Economics” 4th edition, 2001. Mcgraw-Hill Irwin, Boston. Hutchison, M. and Walsh, C. “Empirical Evidence on the Insulation Properties of Fixed and Flexible Exchange Rates: The Japanese Experience.” Journal of International Economics 32, no. ¾ (May 1992), pp. 241-63. Korporaal, Glenda. “Greenspan gives our deficits his blessing.” The Australian Business. October 06, 2007. < http://www.theaustralian.news.com.au/story/0,25197,225383785013510,00.html> Pilbeam, Keith, “International Finance” 2nd edition, 1998. Macmillan Press LTD, London. Williamson, J. 1990a. “Convertibility, Trade Policy, and the Payments Constraint.” Paper presented at a conference on the Transition to a Market Economy in Central and Easter Europe, sponsored by the OECD, Geneva (28-30 November). Williamson, John, “Currency Convertibility in Eastern Europe” Institute for International Economics, 1991 Appendix: Regression Results – Annual Data lnY Coeff. S.E. lnY* Coeff. S.E. lnREX Coeff. DW R² N S.E. Armenia -0.584 [3.67] 0.159 4.577* [4.80] 0.954 0.665 [2.71] 0.245 1.1 0.698 14 Estonia -0.144 [2.88] 0.05 0.772 [2.99] 0.258 0.363** [5.07] 0.072 2.9 0.652 15 Georgia -1.91 [2.82] 0.679 5.48* [3.91] 1.4 -1.003 [3.57] 0.281 1.84 0.882 12 Latvia 0.745 [2.42] 0.308 -3.38 [2.77] 1.22 0.964 [4.34] 0.222 1.5 0.895 14 Lithuania -0.307 [1.845] 0.166 0.813 [1.225] 0.664 -0.209 [0.934] 0.224 1.31 0.276 13 Poland 0.382 [1.64] 0.233 -1.461 [1.76] 0.828 -0.788 [2.77] 0.285 2.25 0.585 16 Russia -0.155 [2.57] 0.06 1.263 [2.63] 0.48 0.183 [2.69] 0.068 1.59 0.567 16 Ukraine -0.138 [2.28] 0.06 0.694 [2.21] 0.314 0.141 [2.09] 0.068 1.34 0.154 16 1.97 0.884 13 Moldova 1257 551 12856 3316 537 186 (linear / log) [2.28] [3.88] [2.89] Note: Statistics with *, **, or *** are significant at 10%, 5%, or 1% level, respectively. lnY - log of domestic income lnY* - log of foreign income lnREX - log of exchange rate, defined as domestic currency per unit of SDR R² - coefficient of determination N - number of observations t-statistics are in brackets Quarterly Results lnY Coeff. Armenia S.E. lnY* Coeff. S.E. lnREX Coeff. DW R² N S.E. 0.077 [1.19] 0.064 1.94*** [3.17] 0.611 0.524* [2.46] 0.213 0.962 0.397 51 -31.517* [1.8] 17.6 -2248.5*** [20.6] 109.1 1196.1*** [10.6] 113.3 1.07 0.899 61 Georgia 0.245* [2.4] 0.102 -0.769 [.318] 0.18 0.808*** [5.76] 0.14 1.14 0.705 43 Latvia -0.036 [.63] 0.058 -1.401*** [3.49] 0.402 0.104 [.61] 0.171 1.65 0.763 63 Lithuania 0.093 [1.5] 0.06 -1.61*** [4.66] 0.35 -0.522*** [3.97] 0.131 2.02 0.319 56 Poland 0.04 [.46] 0.088 -0.356 [.79] 0.45 -0.568*** [7.7] 0.074 1.15 0.6 52 Russia -0.14** [3.01] 0.046 1.05* [1.77] 0.59 0.232*** [5.6] 0.041 0.655 0.587 57 Ukraine -0.079* [2.2] 0.036 -1.28** [3.1] 0.418 0.694* [2.9] 0.24 1.36 0.577 31 Moldova -156.2*** 40.3 2548.5*** 412.5 176.5 linear / log [3.9] [6.2] [.79] Note: Statistics with *, **, or *** are significant at 10%, 5%, or 1% level, respectively. lnY - log of domestic income lnY* - log of foreign income lnREX - log of exchange rate, defined as domestic currency per unit of SDR R² - coefficient of determination N - number of observations t-statistics are in brackets 224.4 1.92 0.832 32 Estonia linear / log ARMENIA: Estonia: Georgia: Latvia: Lithuania: Moldova: Poland: Russia: Ukraine: